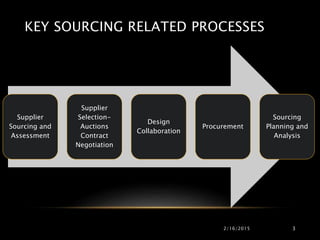

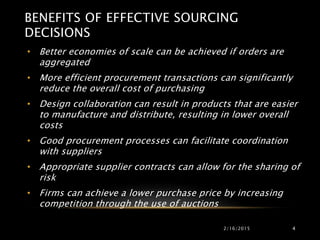

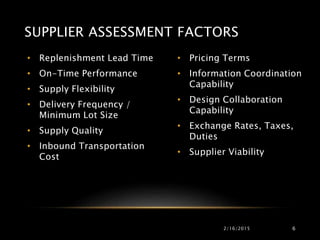

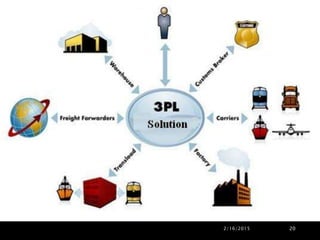

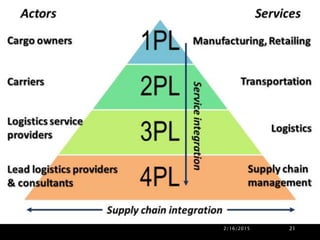

This document discusses key concepts related to sourcing and pricing decisions in a supply chain. It covers the role of sourcing, key sourcing processes like supplier selection and assessment, benefits of effective sourcing like cost reductions. It also discusses supplier scoring and assessment factors, the decision to source in-house vs outsource. Methods for how third parties can increase supply chain surplus are outlined. Risks of using third parties and types of third and fourth party logistics providers are summarized. The document also discusses supplier selection methods like auctions and negotiations, types of contracts to improve supply chain performance, the importance of design collaboration, and an overview of the procurement process.