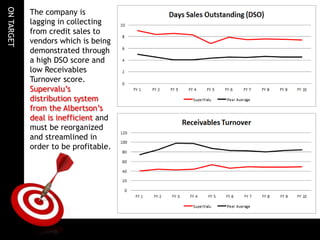

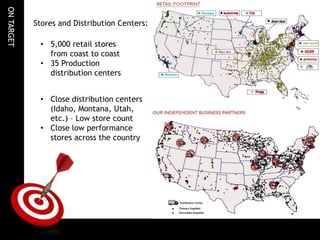

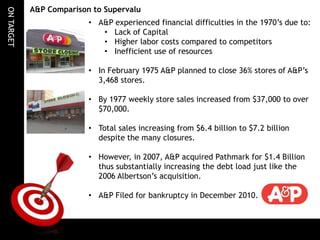

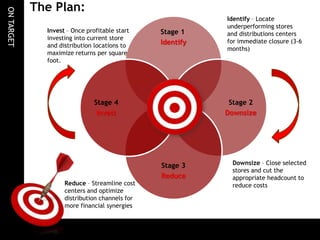

This document discusses strategies for the turnaround of struggling grocery chain Supervalu, including recommendations to close underperforming stores and distribution centers, reduce headcount and benefits, tighten credit, and convert owned Save-A-Lot stores to franchises. It compares Supervalu's management and financial struggles to other chains like Safeway and A&P. Forward strategies involve identifying and closing unprofitable locations while investing in others, followed by downsizing headcount and streamlining costs. Projections estimate financial improvement from cost cuts and debt refinancing.