Sums on profits and gains from business or profession

1. Profits and Gains of Business or Profession

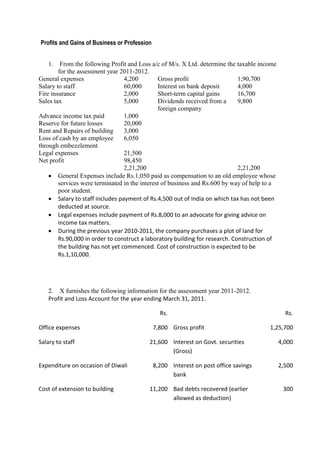

1. From the following Profit and Loss a/c of M/s. X Ltd. determine the taxable income

for the assessment year 2011-2012.

General expenses 4,200 Gross profit 1,90,700

Salary to staff 60,000 Interest on bank deposit 4,000

Fire insurance 2,000 Short-term capital gains 16,700

Sales tax 5,000 Dividends received from a

foreign company

9,800

Advance income tax paid 1,000

Reserve for future losses 20,000

Rent and Repairs of building 3,000

Loss of cash by an employee

6,050

through embezzlement

Legal expenses 21,500

Net profit 98,450

2,21,200 2,21,200

General Expenses include Rs.1,050 paid as compensation to an old employee whose

services were terminated in the interest of business and Rs.600 by way of help to a

poor student.

Salary to staff includes payment of Rs.4,500 out of India on which tax has not been

deducted at source.

Legal expenses include payment of Rs.8,000 to an advocate for giving advice on

income tax matters.

During the previous year 2010-2011, the company purchases a plot of land for

Rs.90,000 in order to construct a laboratory building for research. Construction of

the building has not yet commenced. Cost of construction is expected to be

Rs.1,10,000.

2. X furnishes the following information for the assessment year 2011-2012.

Profit and Loss Account for the year ending March 31, 2011.

Rs. Rs.

Office expenses 7,800 Gross profit 1,25,700

Salary to staff 21,600 Interest on Govt. securities

(Gross)

4,000

Expenditure on occasion of Diwali 8,200 Interest on post office savings

bank

2,500

Cost of extension to building 11,200 Bad debts recovered (earlier

allowed as deduction)

300

2. Depreciation 3,700

Entertainment expenses 12,506

Contribution to:

Unapproved Gratuity Fund 6,000 Sundry receipts 2,000

Unrecognized provident fund 4,500

Reserve for bad debts 700

Net profit 58,294

1,34,500 1,34,500

Office expenses include a sum of Rs.2,500 paid in cash.

Depreciation according to income tax provisions works out to Rs.2,400.

X had gone on a business trip to Bombay. Expenditure incurred on traveling was

Rs.1,900 per day for 6 days. This has not been recorded in the books.

Commission of Rs.4,000 paid for securing a business order has not been recorded in

the books.

Find out the taxable income for the assessment year 2011-2012

3. X furnishes the following particulars for the assessment year 2011-2012.

P & L a/c for the year ending March 31, 2011

Rs. Rs.

Salary to staff 12,750 Gross profit 1,57,000

Advertisement 8,000 Rent of house property received 24,900

Wealth tax 2,500 Short-term capital gains 7,000

Income tax penalty 1,750 Bad debts recovered (disallowed

earlier)

5,600

Travelling expenses 7,100 Gift received 4,000

Bonus to staff 8,400 Winning from lottery 6,000

3. Contribution to Unrecognized

Provident fund

6,200

Car expenses 7,500

Depreciation 12,000

Repairs of house property 6,000

Municipal taxes of house

property

4,500

Interest on capital borrowed

for construction of house

property

8,000

Net Profit 1,19,800

2,04,500 2,04,500

a. Salary includes payment of Rs.1,700 to a relative which is unreasonable.

b. Advertisement includes cost of 5 articles being Rs.1,500 each.

c. Travelling expenses includes an expenditure of Rs.1,750 per day for 4 days. (Being a

business trip to Delhi.)

d. Bonus is outstanding on March 31, 2011. Balance 1/3 is paid on December 1, 2011.

(Due date of furnishing return of income – July 31, 2011.)

e. ¼ of Car expenses relate to personal use.

f. Depreciation as per income tax provisions is Rs.9,500.

Determine the taxable income of X for assessment year 2011-2012.

4. 4. X an advocate who maintains books of account on cash basis furnishes the following

particulars of his income for the previous year ending March 31, 2011.

Receipts and payments a/c for year ending March 31, 2011

Rs. Rs.

Balance b/d 2,500 Purchase of computers 8,000

Fees from clients: Car expenses 4,900

2009-2010 10,000 Office expenses 8,600

2010-2011 38,000 Interest on Loan 1,200

2011-2012 2,500 Income tax penalty 2,500

Presents from clients 6,000 Salary to staff 14,400

Loan from client 7,500 Contribution to public provident

fund

1,500

Balance c/d 25,400

66,500 66,500

1. 35% of car expenses are attributable towards use of car for personal purposes.

Depreciation @ 15%.

2. Written down value of the car on 1/4/2010 is Rs.12,500.

3. Fees due but outstanding – Rs.1,600.

4. Income of X from other sources Rs.20,000.

5. He purchased a typewriter for Rs.20,000 on April 10, 2010. Rate of depreciation 15%.

Determine the taxable income of X for the assessment year 2011-2012.