Downloaded 230 times

The report analyzes the financial statements of S.D. Gupta & Company, highlighting its formation, objectives, and results of financial ratio analysis between 2013-2015. Key findings indicate declining profit margins, liquidity issues, and overall poor performance against industry averages. Recommendations for improvement include enhancing employee efficiency, better control of expenses, and increasing sales and production activities.

Introduction to a financial statement analysis project for S.D. Gupta & Company under CA Shobhit Kumar's supervision.

Introduction of S.D. Gupta & Company, founded in 2015, with details about directors and registration.

Explanation of financial statements as indicators of financial health, aiding in business decision-making.

Objectives include understanding concepts of financial statements and using tools for evaluation.

Data sources for financial analysis, accounting and statistical tools employed for analysis.

Various financial ratios represented in graphs including Gross Profit Ratio, Quick Ratio, and more.

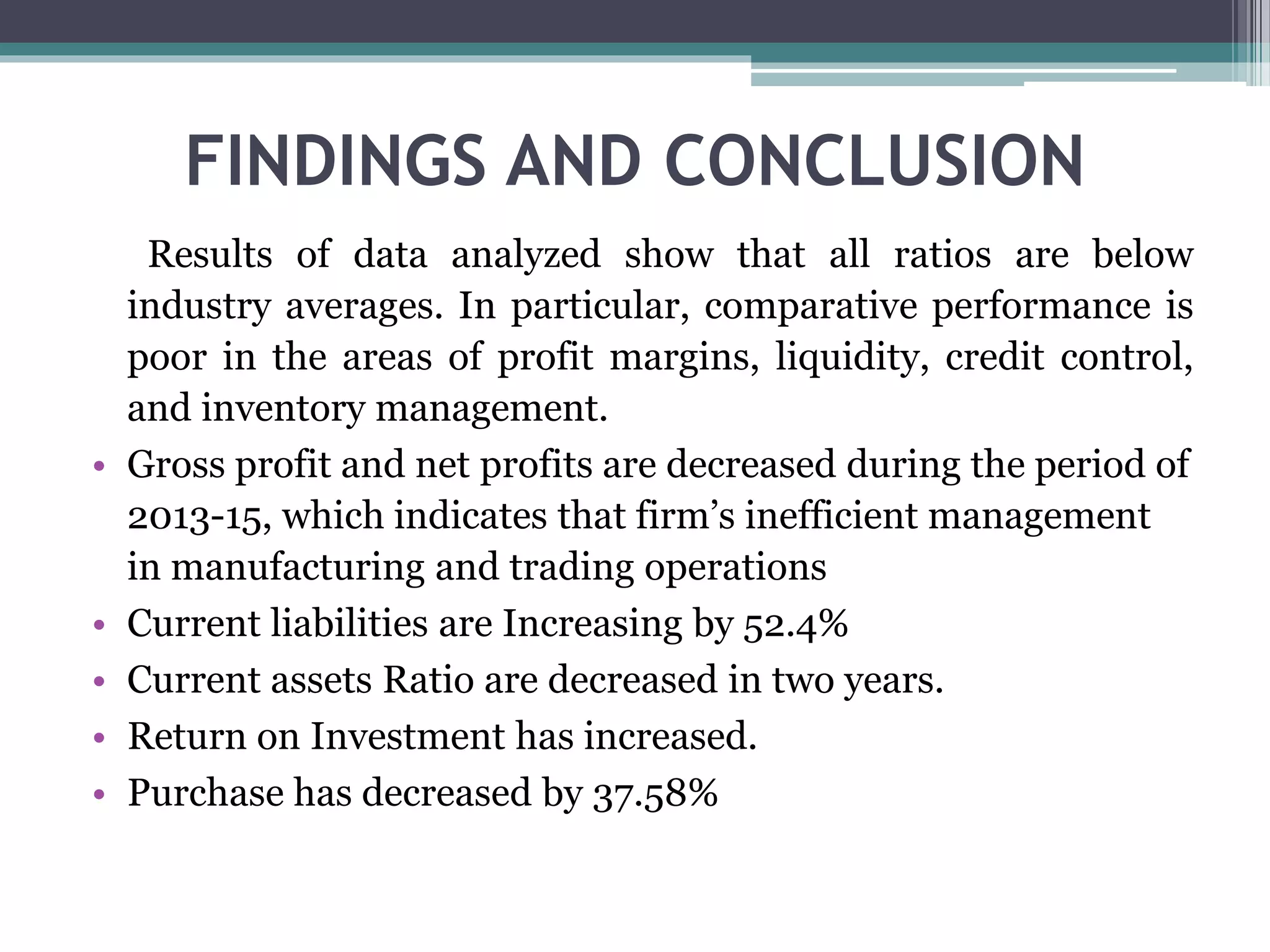

Findings indicate low ratios compared to industry averages and declining profit margins, suggesting mismanagement.

Negative financial trends including decreased sales and profits, pointing to poor prospects for the company.

Suggestions for enhancing employee efficiency and controlling expenses to improve company performance.

Further recommendations on inventory management, process checks, and improving production activities.

Limitations of analysis due to varying accounting principles and industry definitions.

Closing thanks for the presentation.