Download as PDF, PPTX

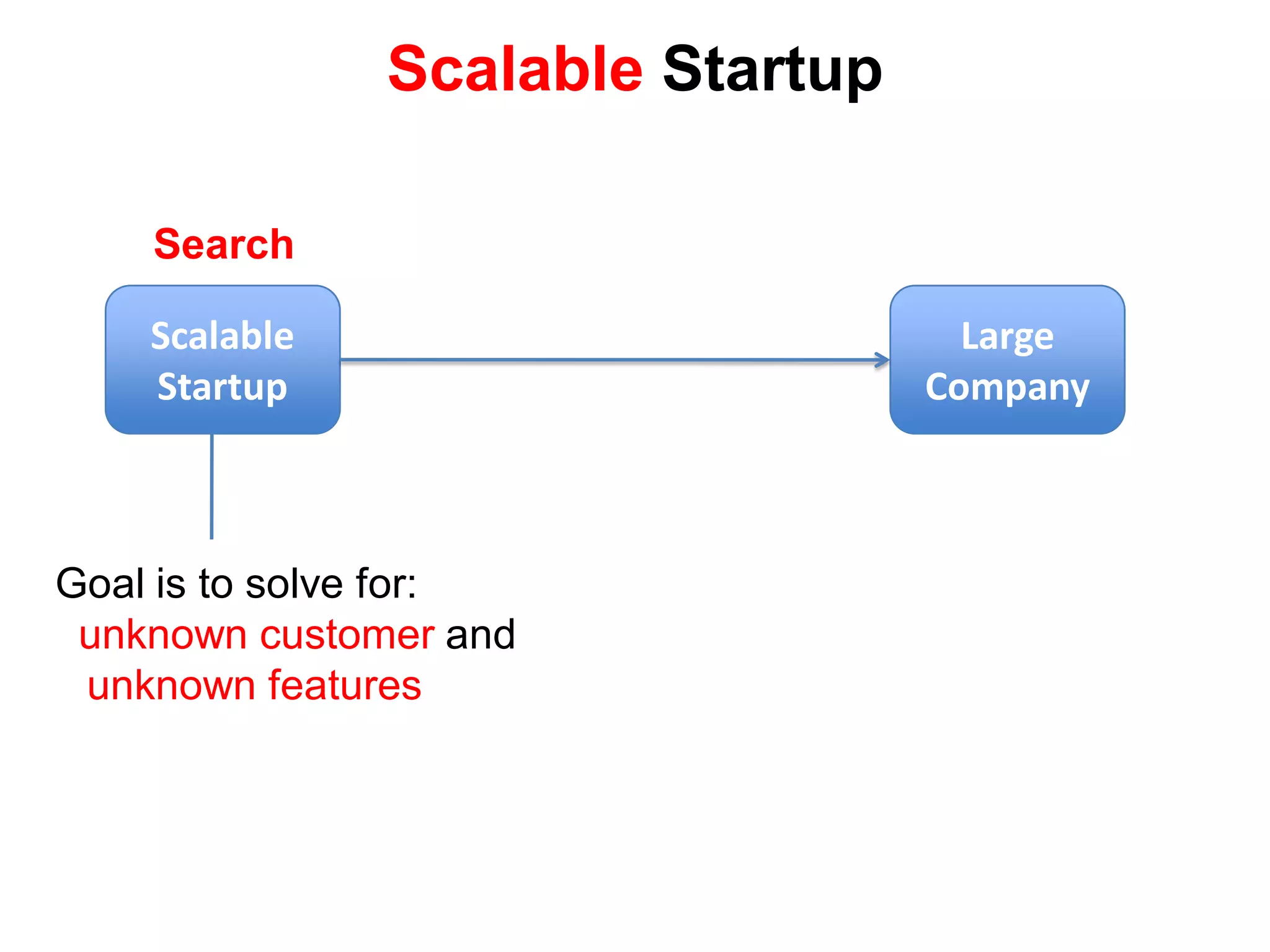

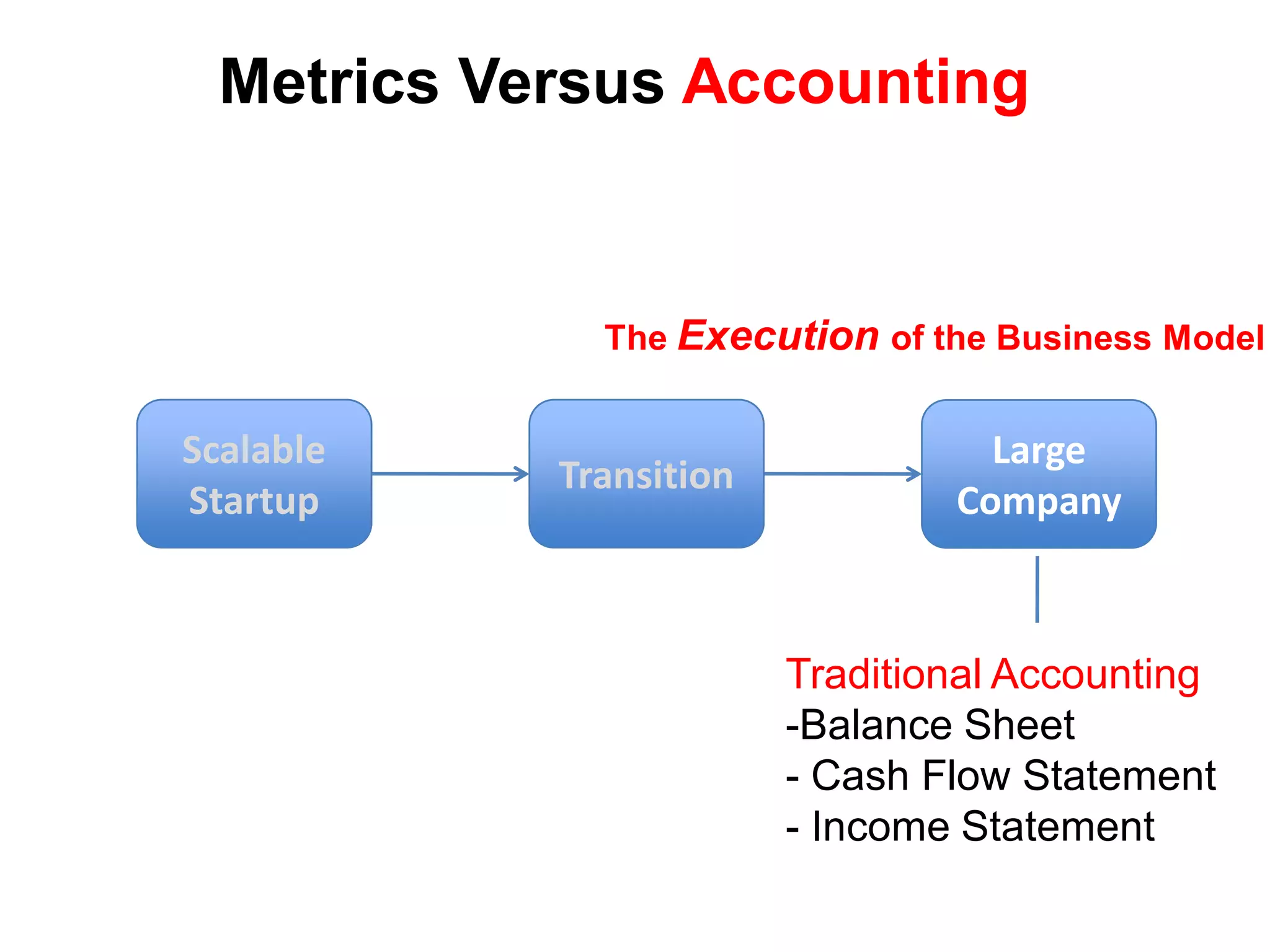

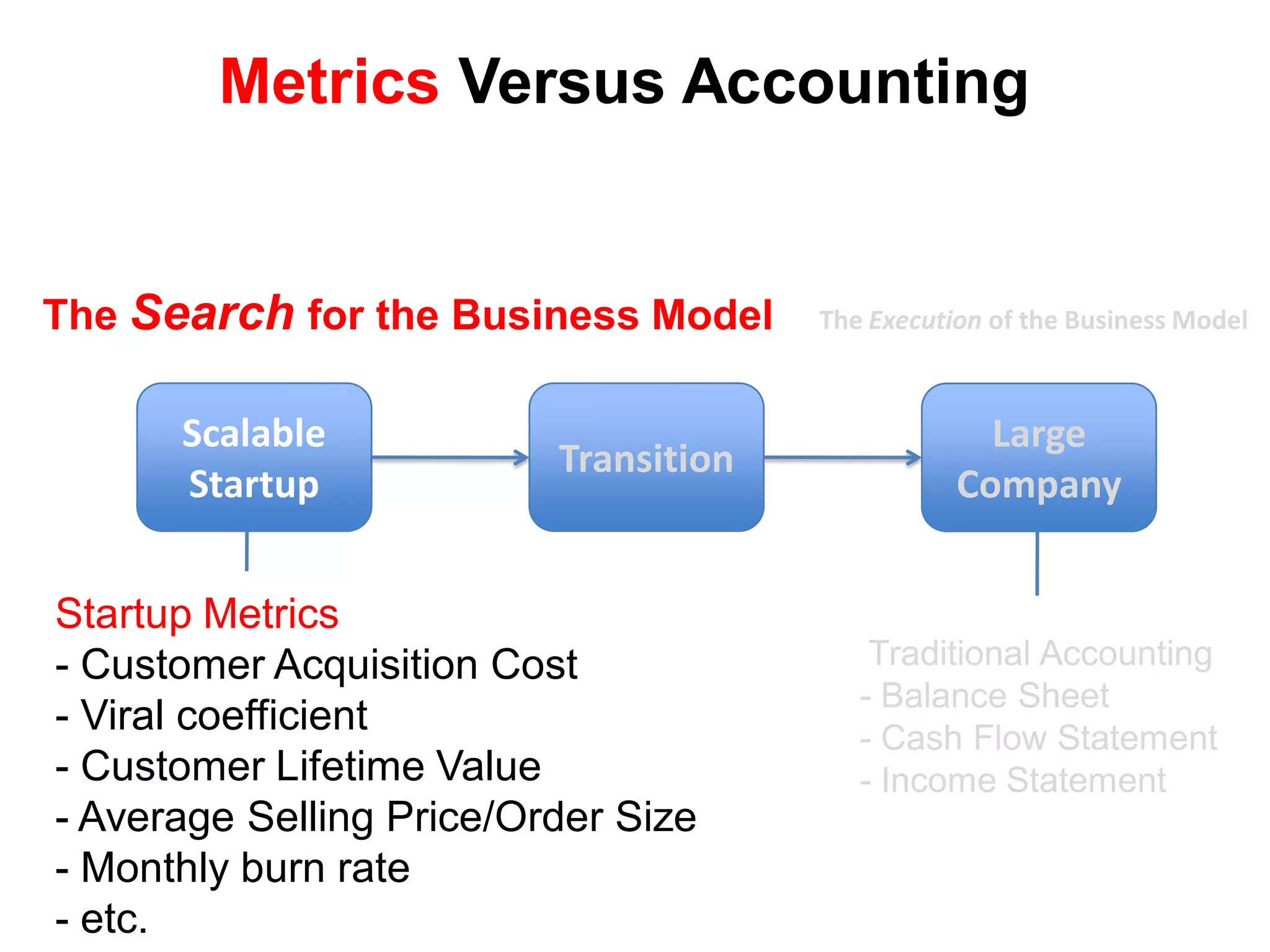

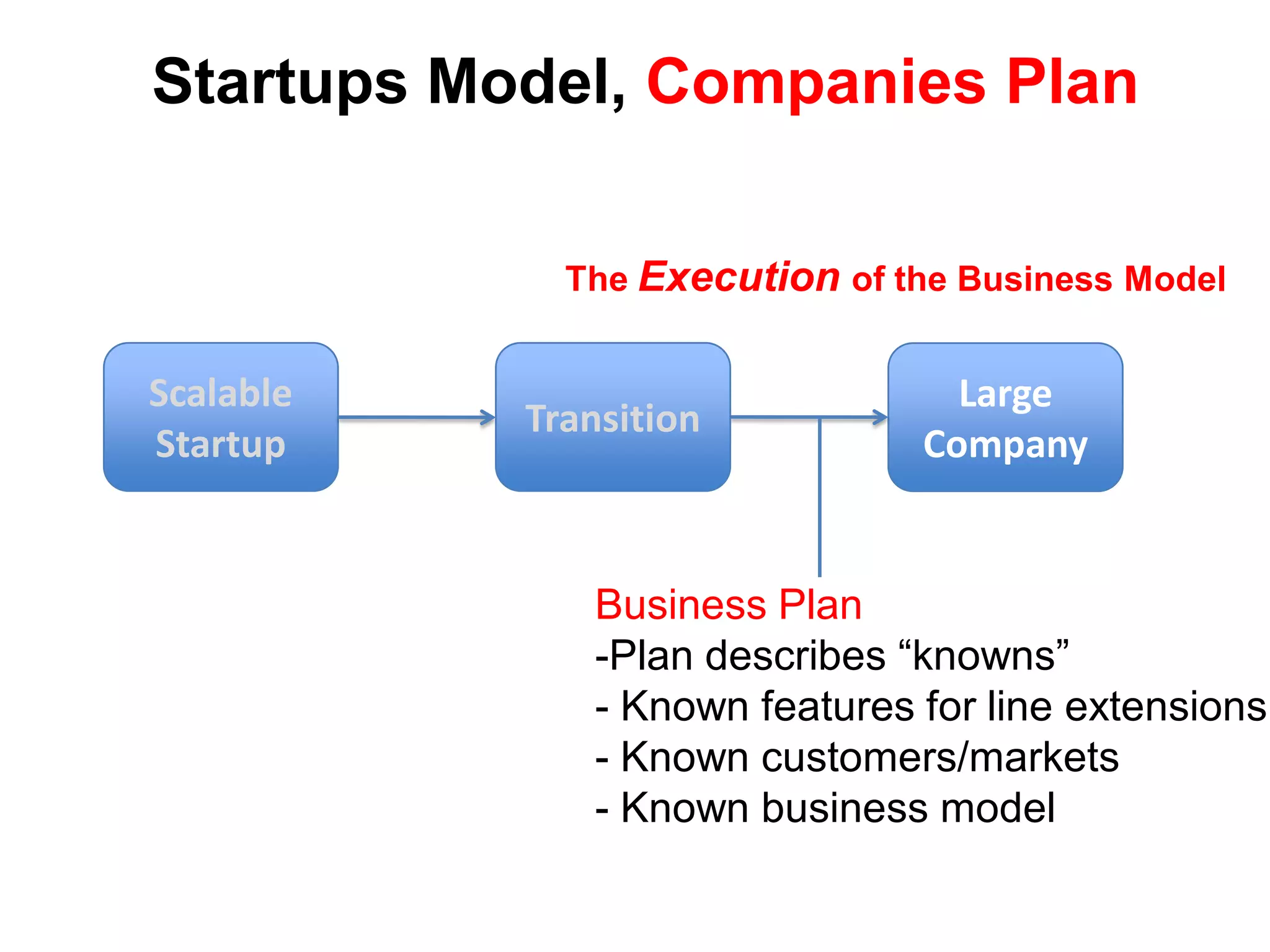

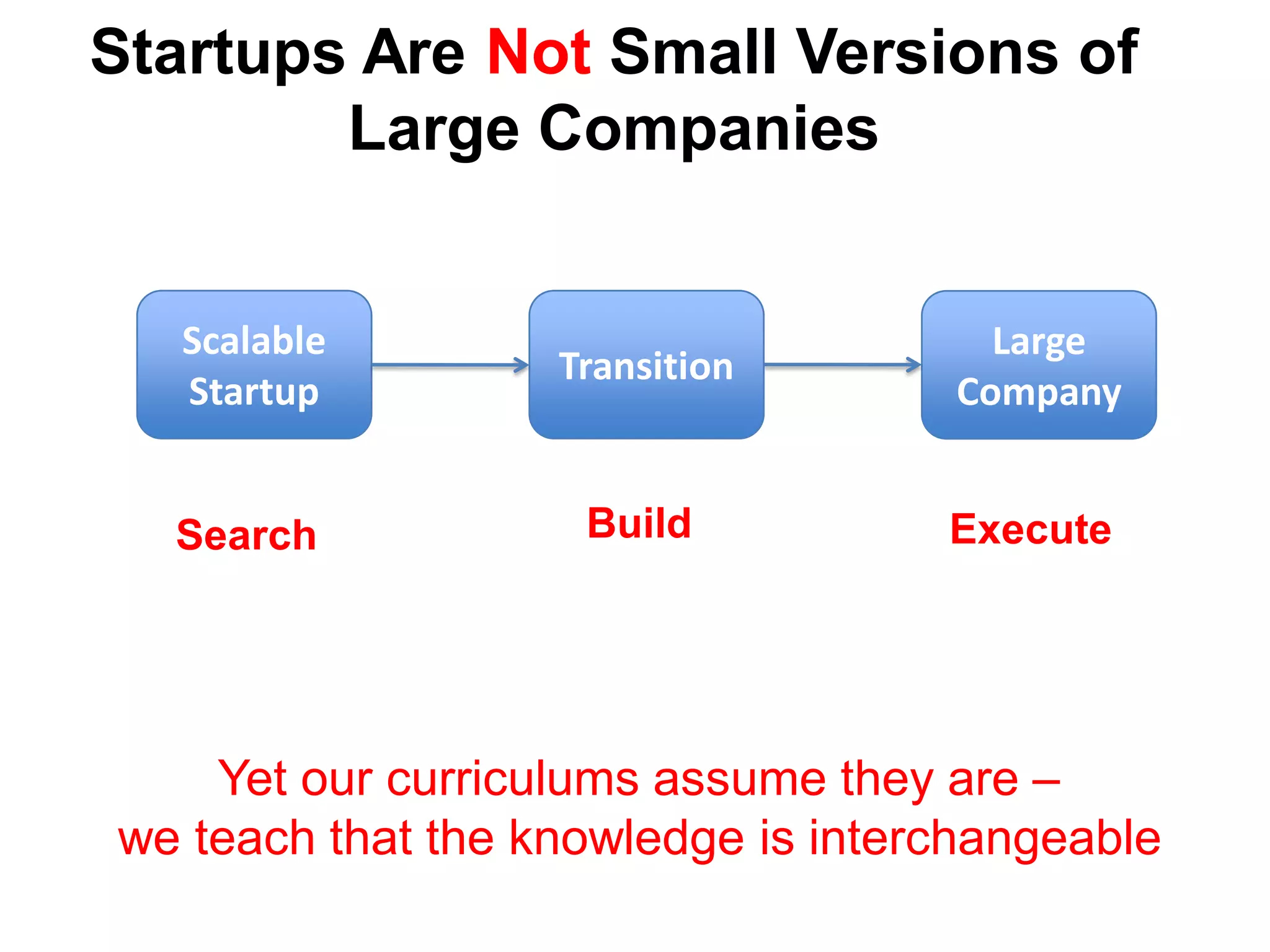

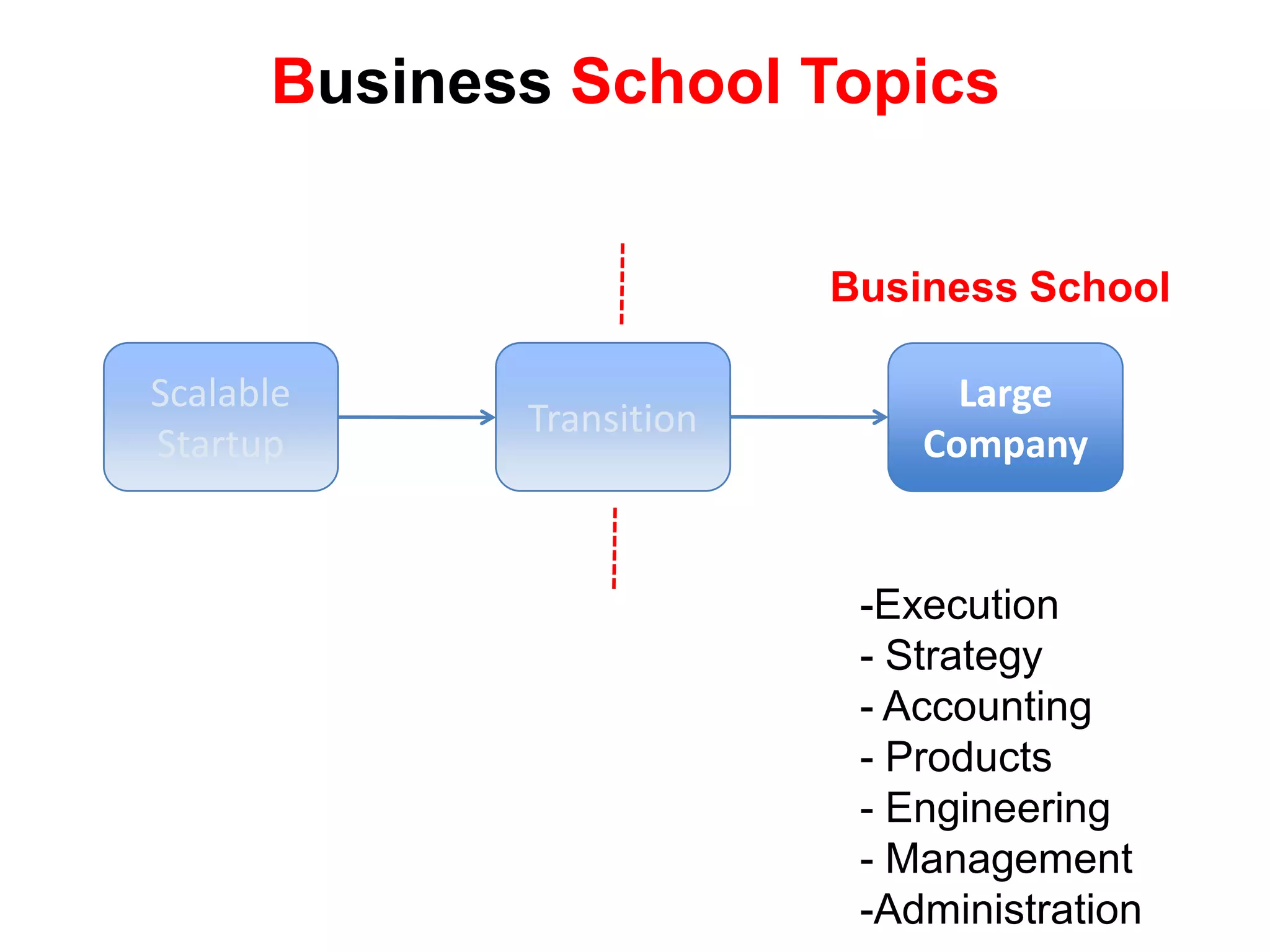

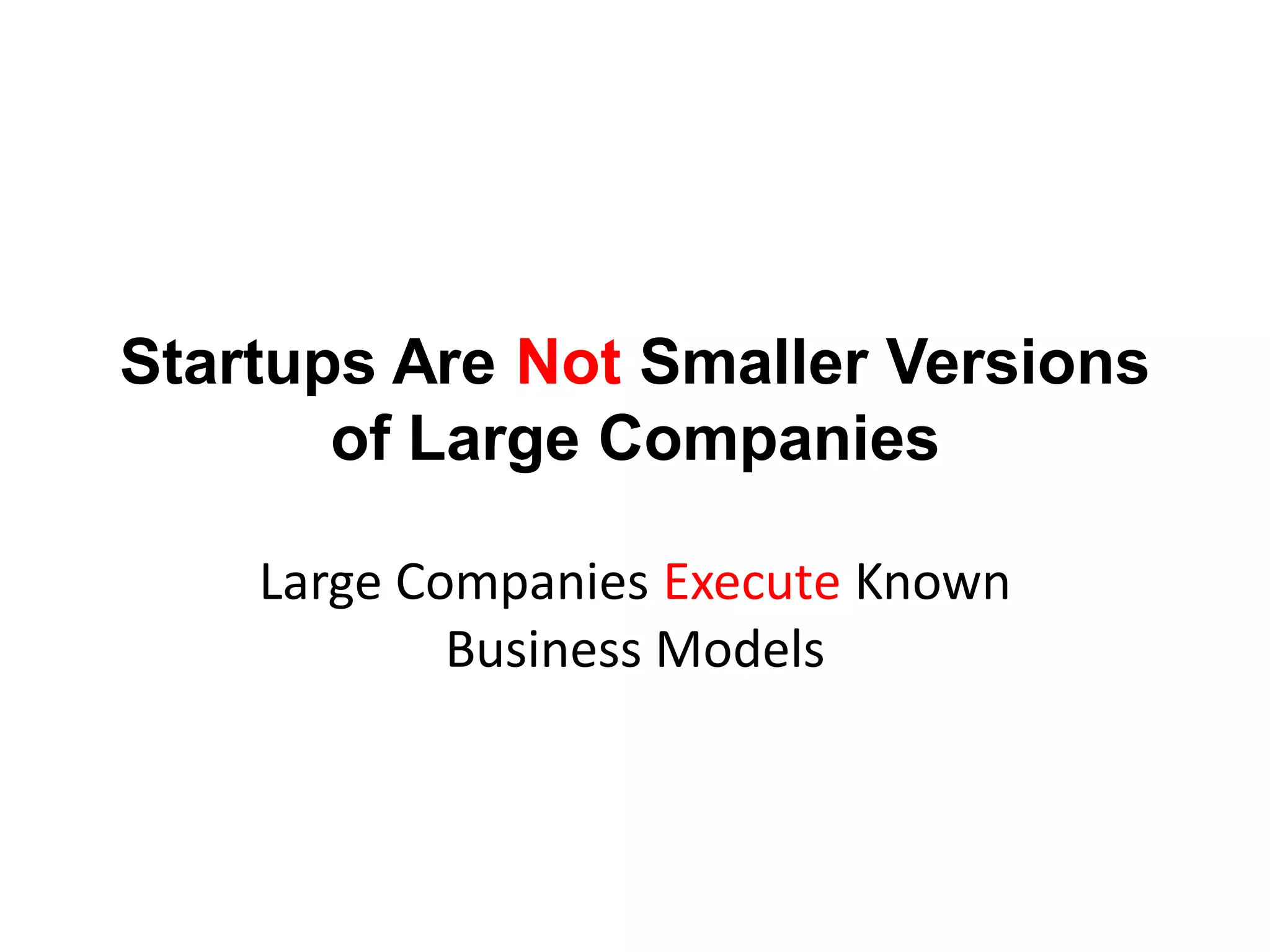

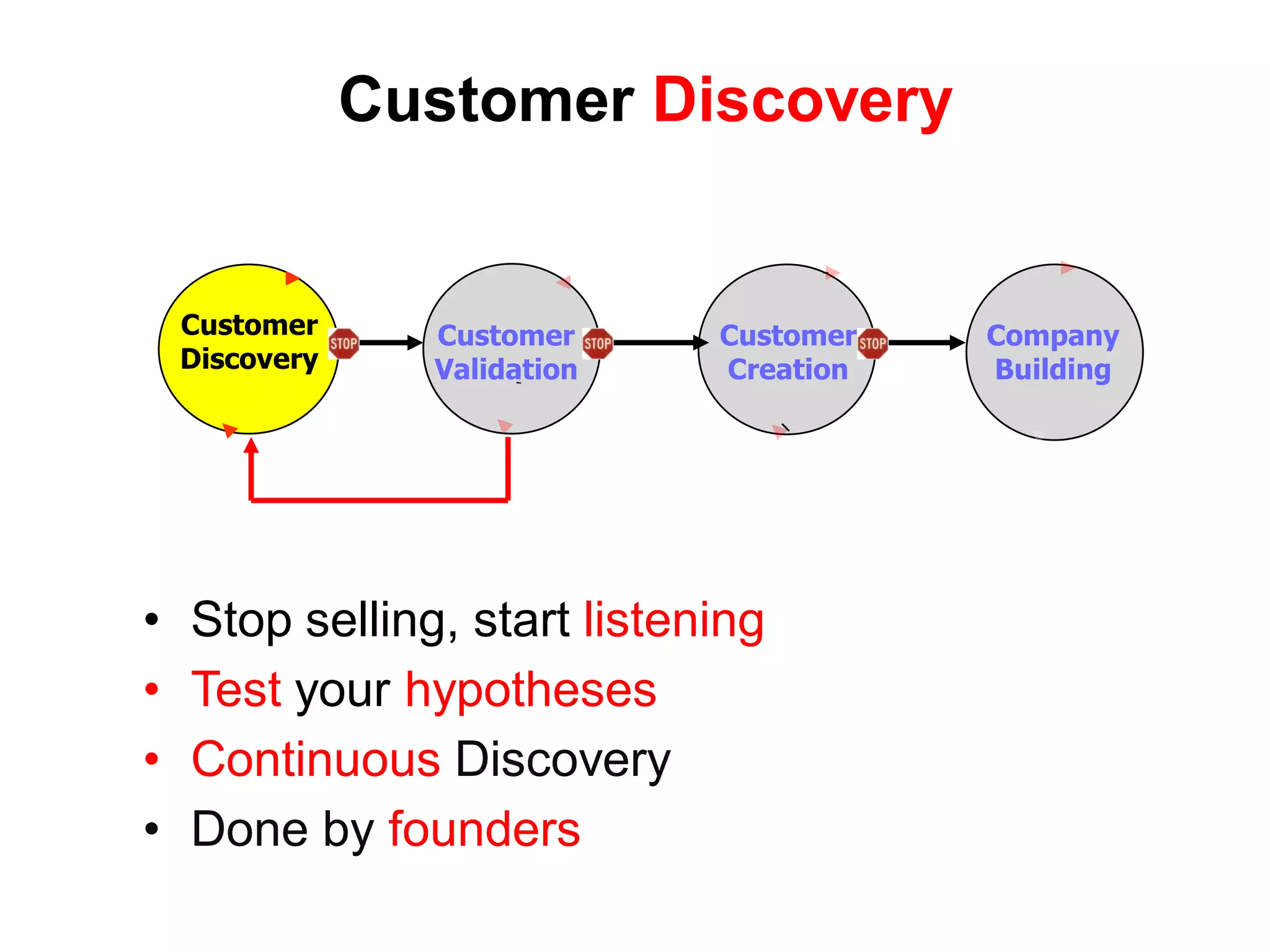

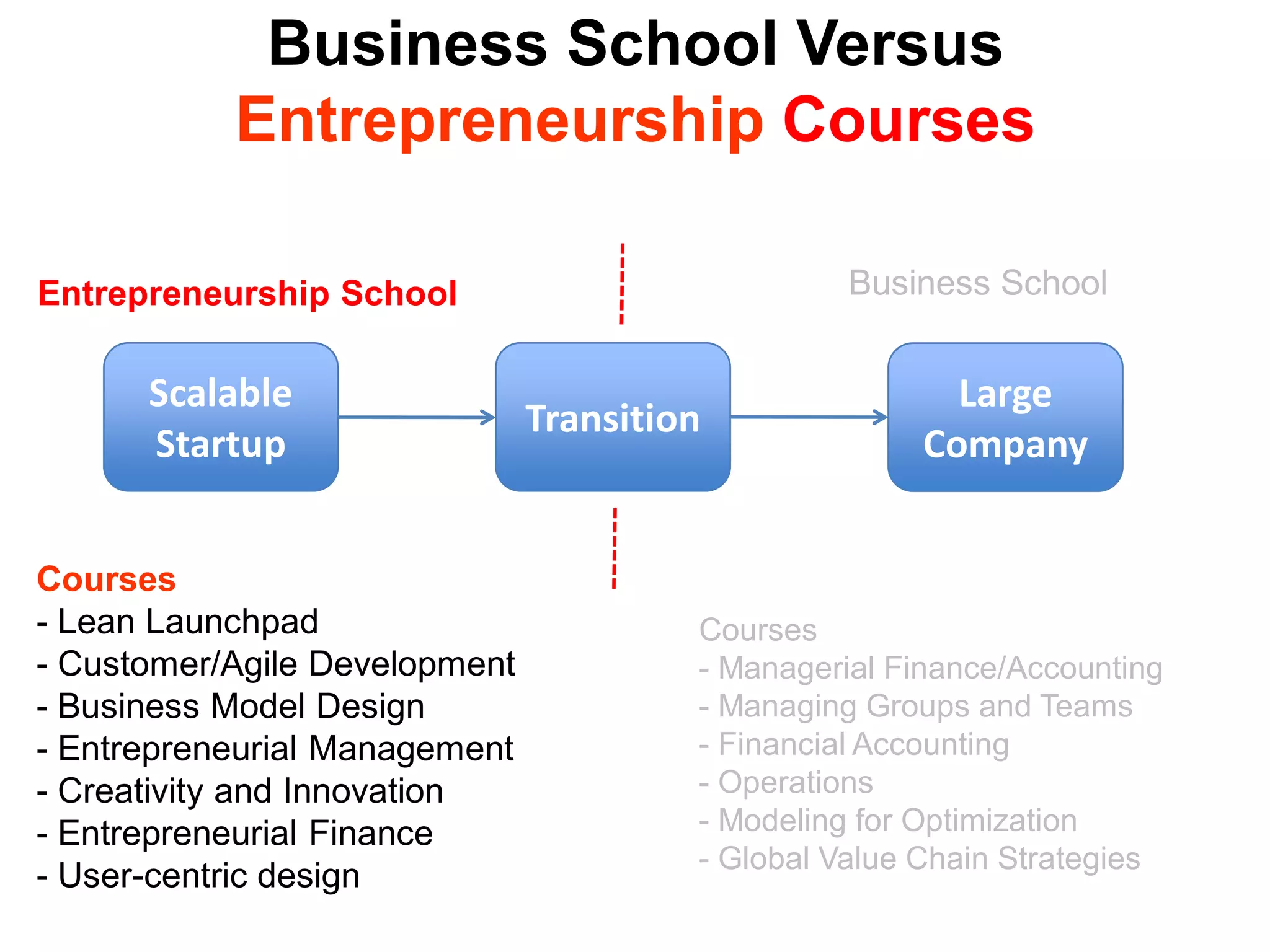

The document summarizes Steve Blank's talk on demolishing the status quo in entrepreneurial education. In 3 sentences: The talk discusses how startups search for a business model while established companies execute known models; it argues that business schools focus on managing large companies and don't teach the customer development process essential for startups; and it proposes establishing entrepreneurship schools that teach the iterative business model development process used by startups.