This document provides an overview of the steel industry in India. It discusses the size and structure of the Indian steel market, including major players. Some key points:

- India is the 2nd largest producer of crude steel globally, with production of over 10 million tonnes in 2022. The steel industry is divided into integrated producers and secondary producers.

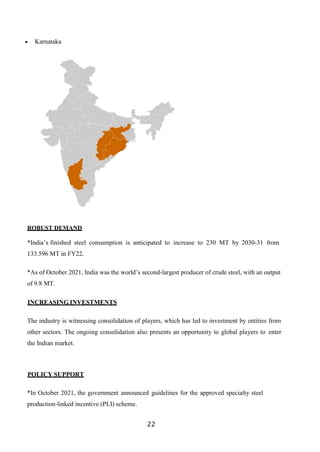

- The market size of the steel industry has grown significantly in the last decade, with production up 75% since 2008. Production in 2022 was over 133 million tonnes of crude steel.

- The government anticipates steel production will exceed 300 million tonnes by 2030-31, with consumption reaching 206 million tonnes. Major investments have been made to

![51

Reference books:

• Brigham, E. and Houston, J., n.d. Fundamentals of financial management.

• Higgins, R., Koski, J. and Mitton, T., 2019. Analysis for financial management. New York, NY:

McGraw-Hill Education.

• Khan, M. and Jain, P., 2014. Financial management. New Delhi: McGraw Hill Education.

• Palmer, J., 1983. Financial ratio analysis. New York, N.Y.: American Institute of Certified Public

Accountants.

Journals:

• Dundas, J., 2009. Understanding Code Patterns – Analysis, Interpretation & Measurement.

International Journal of Computer and Electrical Engineering, pp.46-55.

Websites:

• En.wikipedia.org. 2021. Steel industry - Wikipedia. [online] Available at:

<https://en.wikipedia.org/wiki/Automotive_industry> [Accessed 28 March 2021].

• Tatasteel.com. 2021. Largest steel Manufacturer, Biggest Automobile Company in India.[online]

Available at: <https://www.tatamotors.com/> [Accessed 22 March 2021].

• Investopedia. 2021. Reading Financial Performance. [online] Available

at:<https://www.investopedia.com/terms/f/financialperformance.asp#:~:

text=Financial%20performance%20is%20a%20subjective,health%20ov

er%20a%20given%20period.> [Accessed 23 March 2021].

• En.wikipedia.org. 2021. Tata steel - Wikipedia. [online] Available at:

<https://en.wikipedia.org/wiki/Tata_steel> [Accessed 28 March 2021].

• Moneycontrol.com. 2021. The three companies Balance Sheet, The three companies Financial

Statement & Accounts.[online] Available at:

<https://www.moneycontrol.com/financials/tatamotors/balance- sheet VI/TM03> [Accessed 22

Msheet VI21].](https://image.slidesharecdn.com/ka131-230322030324-b9d73048/85/steel-industry-project-docx-58-320.jpg)