India has a deep-rooted legacy in toy-making, dating back to the Indus Valley Civilization. Fast forward to today, the country is at a pivotal moment in reclaiming its position as a global toy manufacturing powerhouse. 🚀

𝗞𝗲𝘆 𝗜𝗻𝘀𝗶𝗴𝗵𝘁𝘀 𝗳𝗿𝗼𝗺 𝗿𝗲𝗽𝗼𝗿𝘁:

🔹 𝗛𝗶𝘀𝘁𝗼𝗿𝗶𝗰𝗮𝗹 𝗥𝗼𝗼𝘁𝘀 – Toys like marbles (2000 BC) and Chaupar (4th century) evolved with Indian civilization.

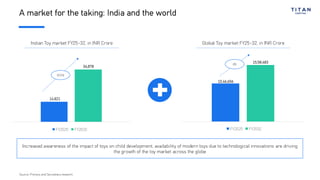

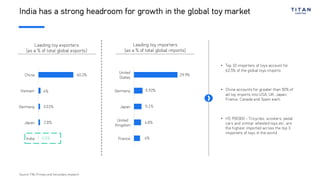

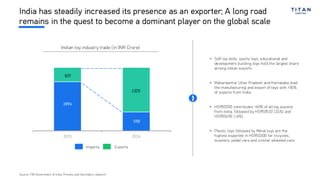

🔹 𝗘𝘅𝗽𝗼𝗿𝘁𝘀 𝗼𝗻 𝘁𝗵𝗲 𝗥𝗶𝘀𝗲 – Post-1990s liberalization, imports from China dominated, but today, India is reclaiming its space with a ~𝟰𝟬% 𝗲𝘅𝗽𝗼𝗿𝘁 𝗿𝗶𝘀𝗲 𝘀𝗶𝗻𝗰𝗲 𝟮𝟬𝟮𝟯.

🔹 𝗚𝗼𝘃𝗲𝗿𝗻𝗺𝗲𝗻𝘁 𝗜𝗻𝘁𝗲𝗿𝘃𝗲𝗻𝘁𝗶𝗼𝗻𝘀 – Import duties up from 20% to 70%, dedicated toy clusters and a national action plan to boost domestic production.

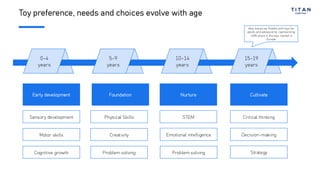

🔹 𝗖𝗵𝗮𝗻𝗴𝗶𝗻𝗴 𝗖𝗼𝗻𝘀𝘂𝗺𝗲𝗿 𝗟𝗮𝗻𝗱𝘀𝗰𝗮𝗽𝗲 –DIWK (Double Income With Kids) households, urbanization (3% YoY), growing e-commerce penetration are fueling demand.

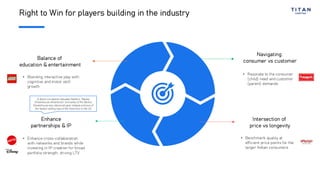

The intersection of 𝗲𝗱𝘂𝗰𝗮𝘁𝗶𝗼𝗻, 𝗲𝗻𝘁𝗲𝗿𝘁𝗮𝗶𝗻𝗺𝗲𝗻𝘁, 𝗮𝗻𝗱 𝗶𝗻𝗻𝗼𝘃𝗮𝘁𝗶𝗼𝗻 is transforming this industry. For entrepreneurs, it’s about balancing consumer (child) delight with customer (parent) demands while 𝗯𝘂𝗶𝗹𝗱𝗶𝗻𝗴 𝗜𝗣𝘀 𝗮𝗻𝗱 𝗽𝗮𝗿𝘁𝗻𝗲𝗿𝘀𝗵𝗶𝗽𝘀. With the right ecosystem 𝗲𝗰𝗼𝘀𝘆𝘀𝘁𝗲𝗺 𝗲𝗻𝗮𝗯𝗹𝗲𝗿𝘀, 𝗺𝗮𝗿𝗸𝗲𝘁 𝗽𝗼𝘁𝗲𝗻𝘁𝗶𝗮𝗹, 𝗮𝗻𝗱 𝘀𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗳𝗼𝗰𝘂𝘀, India is set to 𝗯𝗲𝗰𝗼𝗺𝗲 𝗮 𝗴𝗹𝗼𝗯𝗮𝗹 𝘁𝗼𝘆 𝗽𝗼𝘄𝗲𝗿𝗵𝗼𝘂𝘀𝗲. 🏆

At Titan Capital, We back visionary entrepreneurs who drive India’s growth story. If you’re building in this space, we’d love to hear from you! 🚀

📩 Reach out: startups@titancapital.vc