移动游戏三大分类

WAP App HTML5

Game access •Operator(移动梦 •App store/market •Search

网) •Social platform •Portal/browser

•Portal(UC, 3G, etc) •In-game •Social platform

•Pre-install referral/ads

•Pre-install

•Search

Payment •Operator •Apple store •Least regulated

•Social platform •Social platform •Tech not ready

•Android-China

User ownership • Mainly operator •App store/market •Social platform

•Social games •Social games

•Social platform

CP profit sharing • 30% • 70% for app store •Close to web

games

Content •Low quality •High quality •Mid-high quality

differentiation •Little difference •Much difference •Much difference

Key challenge •Access points •Payment •Timeline

For Internal Use Only 29

30.

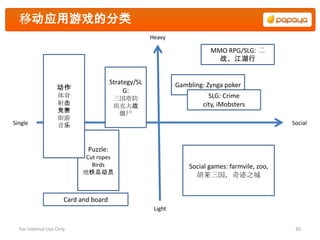

移动应用游戏的分类

Heavy

MMO RPG/SLG: 二

战、江湖行

Strategy/SL Gambling: Zynga poker

动作 G:

体育 三国塔防 SLG: Crime

射击 坦克大战 city, iMobsters

竞赛 僵尸

街游

Single 音乐 Social

Puzzle:

Cut ropes

Birds Social games: farmvile, zoo,

地铁总动员 胡莱三国,奇迹之城

Card and board

Light

For Internal Use Only 30

31.

游戏类别典型代表

Hardcore

Premium Free

Casual

For Internal Use Only 31

32.

中国iOS前20名的游戏

Category # of games Games

Card and Board -

Puzzle 3 Zombie,Where is my water

Action 4 Infinity, Asphalt,Fruit Ninja, King of fighters

Strategy/SLG 1 三国塔防

Social games 4 胡莱三国,开心水族箱,摩尔庄园,Smurfs

SLG online games 3 掌上三国, Japan life, Galaxy empire,

Gambling 1 Texas poker

MMO RPG/SLG 4 二战风云,神仙道,Dungeon Hunter, 江湖行

• 挺多成功手游是web game的拓展版

For Internal Use Only 32

33.

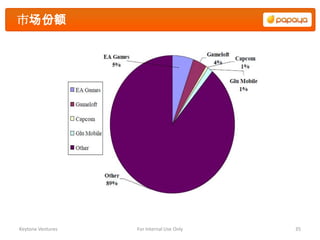

VC支撑的中国移动游戏公司

Cross Game

Company Game type Investors

PC/Mobile categories

顽石 Yes App MMO/Social 挚信资本/成为/IDG资本

胡莱 Yes App Social 红杉,腾讯

摩尔庄园(淘米) Yes App Social 启明,Saban capital

博雅 Yes App Cards 红杉中国

摩卡世界 Yes App Social/SLG 海纳亚洲

恺英网络 Yes App Social/SLG 凯鹏华盈/经纬创投/清科创投

Redatoms No App Music/SLG GSR

Animoca Yes App Social 英特尔投资

TipCat Yes App Puzzle/action 红杉中国

涂鸦移动 No App Social 凯鹏华盈/创新工场/清科创投

木瓜移动 No App Social 凯旋创投/DCM

梦龙移通 No App Action 达晨创投

啪嗒游戏 Yes App Social 创新工场

3G游游 No App Action/Puzzle 银泰资本/招商和腾

盈趣信息 No App Puzzle 晨兴创投

• 9 out of 15 companies offer games across PC browser and mobile platform

• 10 out of 15 are social related games

For Internal Use Only 33

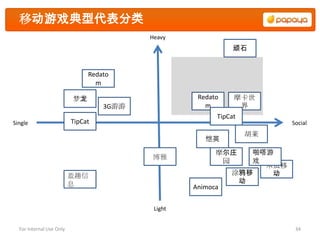

34.

移动游戏典型代表分类

Heavy

顽石

Redato

m

梦龙 Redato 摩卡世

3G游游 m 界

TipCat

Single TipCat Social

胡莱

恺英

摩尔庄 啪嗒游

博雅

园 戏

木瓜移

盈趣信 涂鸦移 动

息 动

Animoca

Light

For Internal Use Only 34

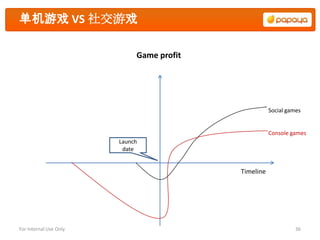

单机游戏 VS 社交游戏

Game profit

Social games

Console games

Launch

date

Timeline

For Internal Use Only 36

37.

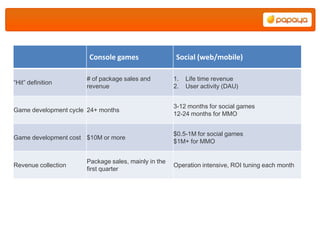

Console games Social (web/mobile)

# of package sales and 1. Life time revenue

“Hit” definition

revenue 2. User activity (DAU)

3-12 months for social games

Game development cycle 24+ months

12-24 months for MMO

$0.5-1M for social games

Game development cost $10M or more

$1M+ for MMO

Package sales, mainly in the

Revenue collection Operation intensive, ROI tuning each month

first quarter

38.

Zynga vs. EA/Blizzard

Zynga as a reference (Q3-2011)

Games DAU

Texas poker 6,300,000

Farm ville 7,300,000

City ville 10,400,000

Empire allies 3,200,000 Top 7 of 17-20 games

Word w/ frieds 5,900,000 count for 75% of the

Pioneer trail 1,700,000 activity

Castle ville 8,300,000

Total 58,000,000

Console game as a reference

Q3-2011 Total 1M+ 1M+ seller Comments

games seller % of total

rev

EA 322 99 74% 1/3 games count for 3/4 income

Blizzard 285 43 74% 1/6 games count for 3/4 income

For Internal Use Only 38

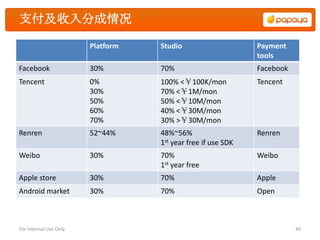

支付及收入分成情况

Platform Studio Payment

tools

Facebook 30% 70% Facebook

Tencent 0% 100% <¥100K/mon Tencent

30% 70% <¥1M/mon

50% 50% <¥10M/mon

60% 40% <¥30M/mon

70% 30% >¥30M/mon

Renren 52~44% 48%~56% Renren

1st year free if use SDK

Weibo 30% 70% Weibo

1st year free

Apple store 30% 70% Apple

Android market 30% 70% Open

For Internal Use Only 40

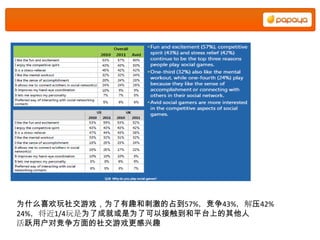

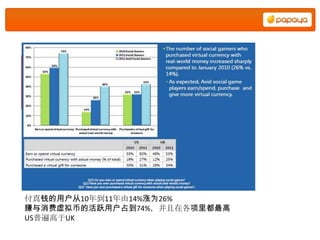

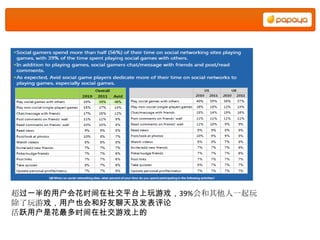

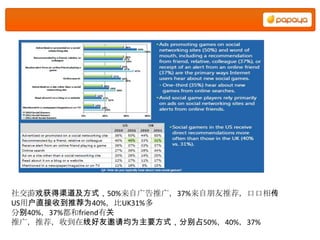

Why Mobile SocialGaming?

• Highly profitable business model low costs of development, customer acquisition

(through social networks), and publishing (no physical product)

• Lower risk R&D - social games can be rolled out much more quickly with smaller

budgets and development teams. Since games are played as a service delivered

over Internet, developers can utilize real-time customer activity to access and

modify components of games throughout game’s life. Publisher can use data to

decide whether to continue investing in a game or kill the project (reinforce

winners and cut losses on losers). Average cost $550k vs $10m on console device

• Zynga has no inherent advantage on Mobile – lack of dominating market share,

lack of high quality content to drive acceptance

• Xbox Live have proven that players want to play their games with other people

$750 million in revene ($60/year subscription fee) why not on mobile?

• Many console publishers are struggling to adapt to online/mobile

Keytone Ventures For Internal Use Only 47