Download to read offline

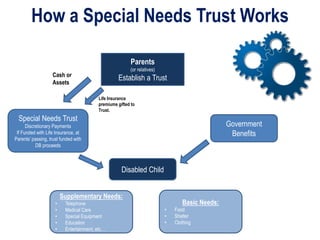

This document discusses special needs trusts and how they can provide financial support for disabled individuals. It notes that planning for the future care of a disabled loved one is best done now rather than later. It then provides details on how special needs trusts work, including that they allow government benefits to continue while providing supplementary funds, and are typically funded through cash, assets, retirement accounts or life insurance. The document recommends consulting an experienced estate planning attorney to properly establish a legally valid special needs trust tailored to an individual's needs and situation.