Downloaded 10 times

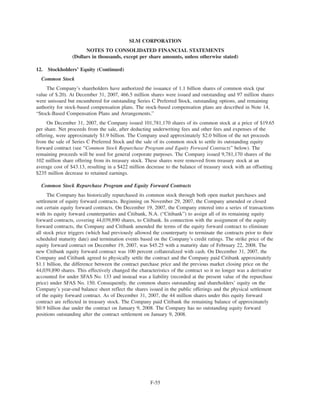

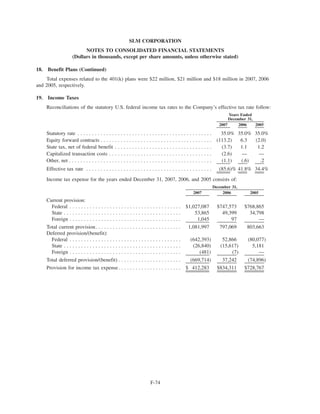

This document is SLM Corporation's annual report on Form 10-K filed with the United States Securities and Exchange Commission for the fiscal year ended December 31, 2007. It provides information on SLM Corporation's business, operations, financial results, subsidiaries, legal proceedings, risks and other disclosures required by the SEC. Specifically, the document includes SLM Corporation's audited financial statements, discusses its student loan portfolio and business segments, discloses legal and regulatory risks, and incorporates portions of its proxy statement by reference.