Downloaded 23 times

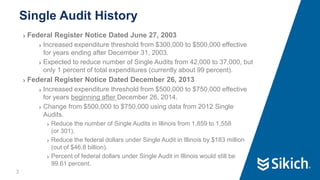

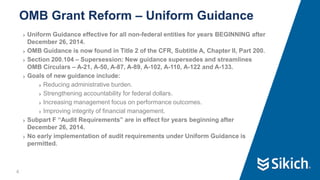

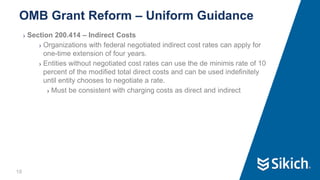

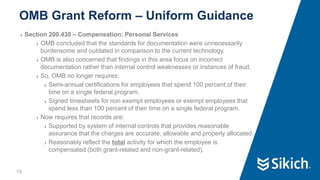

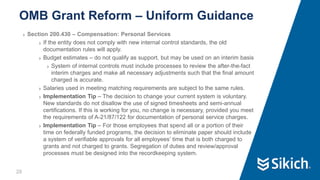

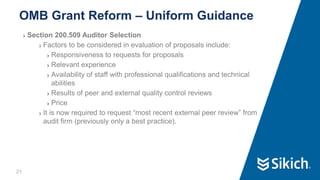

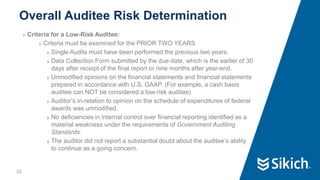

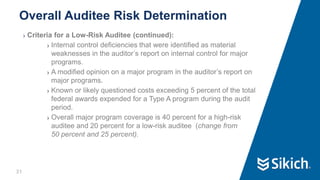

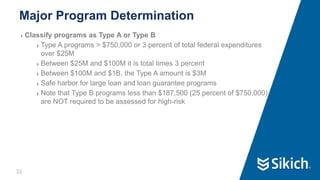

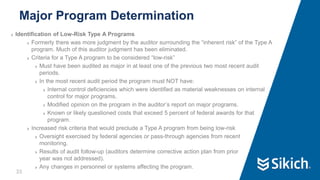

The document discusses the impact of the Uniform Guidance on performing single audits. Some key points include: - The Uniform Guidance consolidated and streamlined eight OMB circulars into one set of guidance. It aims to reduce administrative burden while strengthening accountability. - Major changes under the Uniform Guidance include increasing the threshold for single audits to $750,000, revising internal control and documentation standards for compensation costs, and requiring consideration of an auditor's most recent peer review in the selection process. - Planning procedures for single audits involve determining federal awards expended, distinguishing between subrecipients and vendors, identifying program clusters using the Catalog of Federal Domestic Assistance, and assessing overall auditee risk

![Affordable Care Act Reporting Requirements for 2015 [Webinar Slides]](https://cdn.slidesharecdn.com/ss_thumbnails/acareportingwebinar-june16-150616201027-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)