SIM Equity Research Project - Spring 2014 - CCK - Martin Smith

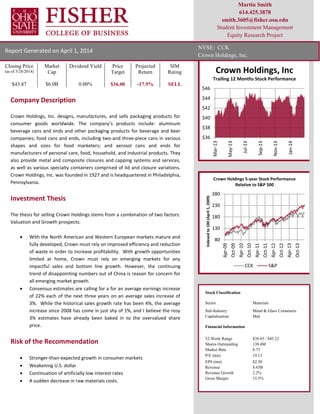

1. Closing Price

(as of 3/28/2014)

$43.87

Market

Cap

$6.0B

Dividend Yield

0.00%

Price

Target

$36.00

Projected

Return

-17.9%

SIM

Rating

SELL

$36

$38

$40

$42

$44

$46

Mar-13

May-13

Jul-13

Sep-13

Nov-13

Jan-14

Crown Holdings, Inc

Trailing 12 Months Stock Performance

80

130

180

230

280

Apr-09

Oct-09

Apr-10

Oct-10

Apr-11

Oct-11

Apr-12

Oct-12

Apr-13

Oct-13

Indexedto100(April1,2009)

Crown Holdings 5-year Stock Performance

Relative to S&P 500

CCK S&P

Report Generated on April 1, 2014

NYSE: CCK

Crown Holdings, Inc.

Martin Smith

614.425.3878

smith.3605@fisher.osu.edu

Student Investment Management

Equity Research Project

Company Description

Crown Holdings, Inc. designs, manufactures, and sells packaging products for

consumer goods worldwide. The company’s products include: aluminum

beverage cans and ends and other packaging products for beverage and beer

companies; food cans and ends, including two-and three-piece cans in various

shapes and sizes for food marketers; and aerosol cans and ends for

manufacturers of personal care, food, household, and industrial products. They

also provide metal and composite closures and capping systems and services,

as well as various specialty containers comprised of lid and closure variations.

Crown Holdings, Inc. was founded in 1927 and is headquartered in Philadelphia,

Pennsylvania.

Investment Thesis

The thesis for selling Crown Holdings stems from a combination of two factors:

Valuation and Growth prospects.

With the North American and Western European markets mature and

fully developed, Crown must rely on improved efficiency and reduction

of waste in order to increase profitability. With growth opportunities

limited at home, Crown must rely on emerging markets for any

impactful sales and bottom line growth. However, the continuing

trend of disappointing numbers out of China is reason for concern for

all emerging market growth.

Consensus estimates are calling for a for an average earnings increase

of 22% each of the next three years on an average sales increase of

3%. While the historical sales growth rate has been 4%, the average

increase since 2008 has come in just shy of 1%, and I believe the rosy

3% estimates have already been baked in to the overvalued share

price.

Risk of the Recommendation

Stronger-than-expected growth in consumer markets

Weakening U.S. dollar

Continuation of artificially low interest rates

A sudden decrease in raw materials costs.

Stock Classification

Sector Materials

Sub-Industry Metal & Glass Containers

Capitalization Mid

Financial Information

52-Week Range $38.85 / $45.22

Shares Outstanding 138.4M

Market Beta 0.73

P/E (ttm) 19.13

EPS (ttm) $2.30

Revenue 8.65B

Revenue Growth 2.2%

Gross Margin 15.5%

2. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 2 of 20

Table of Contents

Company Description ................................................................................................................................................................................................................ 1

Investment Thesis ..................................................................................................................................................................................................................... 1

Risk of the Recommendation..................................................................................................................................................................................................... 1

Company Overview......................................................................................................................................................................................................................... 3

Operating Segments.................................................................................................................................................................................................................. 3

Aerosol Packaging .............................................................................................................................................................................................................................3

Beverage Packaging...........................................................................................................................................................................................................................3

Food Packaging and Closures............................................................................................................................................................................................................4

Specialty Packaging ...........................................................................................................................................................................................................................5

Business Segments .................................................................................................................................................................................................................... 5

Americas Beverage............................................................................................................................................................................................................................5

North America Food..........................................................................................................................................................................................................................5

European Beverage...........................................................................................................................................................................................................................5

European Food..................................................................................................................................................................................................................................6

Asia Pacific ........................................................................................................................................................................................................................................6

Non-Reportable Segments................................................................................................................................................................................................................6

Competitive Advantage ............................................................................................................................................................................................................. 6

The Customer is Always Right ...........................................................................................................................................................................................................6

Location, Location, Location..............................................................................................................................................................................................................7

Recent News and Share Performance ........................................................................................................................................................................................ 7

Investment Thesis ........................................................................................................................................................................................................................... 8

Key Fundamental and Economic Drivers .................................................................................................................................................................................... 8

North America...................................................................................................................................................................................................................................8

International .....................................................................................................................................................................................................................................8

Financial Analysis ...................................................................................................................................................................................................................... 8

Revenue ............................................................................................................................................................................................................................................8

Operating Margins ............................................................................................................................................................................................................................9

Share Buyback...................................................................................................................................................................................................................................9

Peer Comparison...............................................................................................................................................................................................................................9

Liquidity Analysis...............................................................................................................................................................................................................................9

Discounted Cash Flow Analysis ................................................................................................................................................................................................ 10

Multiple Analysis..................................................................................................................................................................................................................... 10

Relative to the S&P 500 Benchmark................................................................................................................................................................................................10

Relative to its Sector .......................................................................................................................................................................................................................10

Relative to its Industry ....................................................................................................................................................................................................................11

Crown Multiples Evaluation ............................................................................................................................................................................................................11

Risks to the Recommendation ................................................................................................................................................................................................. 12

External Risks ..................................................................................................................................................................................................................................12

Conclusion .................................................................................................................................................................................................................................... 14

Recommendation.......................................................................................................................................................................................................................... 14

Appendixes ................................................................................................................................................................................................................................... 15

Appendix 1: Forecast of Income Statement............................................................................................................................................................................. 15

A. Income Statement...............................................................................................................................................................................................................15

B. Detailed Breakdown of Income Statement .........................................................................................................................................................................16

Appendix 2: Select Balance Sheet a Cash Flow Figures............................................................................................................................................................. 17

Appendix 3: Discounted Cash Flow Analysis ............................................................................................................................................................................ 18

Appendix 4: Sensitivity Analysis.............................................................................................................................................................................................. 19

A. Price Target Sensitivity Analysis ..........................................................................................................................................................................................19

B. Potential Upside / Downside Sensitivity Analysis ................................................................................................................................................................19

Sources......................................................................................................................................................................................................................................... 20

3. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 3 of 20

Company Overview

In 1891, William Painter invented the crown cap for

bottling carbonated beverages. The following year,

he founded the Crown Cork and Seal Company in

Baltimore, Maryland and set out to convince

bottlers that his cap was ideal for their product.

Crown Cork and Seal thrived in the early years,

expanding manufacturing into Europe, South

America, and Asia by 1906. In 1927, Crown Cork

and Seal merged with the New Process Cork

Company creating Crown Holdings, Inc. (hereby

known as Crown or “the Company”).

In the 1930’s, Crown commanded more than half

of the world’s market share for bottle caps. The

company acquired Acme Can Company of

Philadelphia and entered the tin can business in

1936, further expanding its footprint. However,

the expansive growth and profitability slowed, and

by 1957 Crown was on the verge of bankruptcy

from a series of poor diversification moves. John

Connelly, a former supplier to Crown, acquired

control of the company.

In just one year’s time, Connelly orchestrated the

beginnings of a miraculous turnaround, moving the

corporate headquarters to Philadelphia, paring

down the size of the organization, and

implementing stringent economies. In five short

years, Connelly had achieved a 1,646% increase in

profits on a relatively insignificant sales increase. A

$100 investment in Crown in 1957 would be worth

approximately $66,000 today; proof of the

leadership present in the office of the CEO.

Operating Segments

Crown Holdings operates its business in four

segments: Aerosol Packaging, Beverage Packaging,

Food Packaging and Closures, and Specialty

Packaging.

Aerosol Packaging

The Company’s customers for aerosol cans and

ends include manufacturers of personal care, food,

household, and industrial products. Some of these

companies include Colgate Palmolive, KIK Custom,

Procter & Gamble, SC Johnson, and Unilever. The

aerosol can business is highly competitive, so

Crown competes by offering its customers a broad

range of products including multiple sizes, multiple

color schemes, and shaped packaging.

Beverage Packaging

The Company supplies beverage cans and ends and

other packaging products to a variety of beverage

and beer companies, including Anheuser-Busch

InBev, Carlsberg, Coca-Cola, Cott Beverages, Dr

Pepper Snapple Group, Heineken, National

Beverage, and Pepsi-Cola. Crown’s beverage

business is built around local, regional and global

markets, which has served to develop their

understanding of global consumer expectations.

4. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 4 of 20

The beverage market is dynamic and highly

competitive, with each packaging manufacturer

working with its customers to satisfy consumers’

ever-changing needs. Crown competes by offering

its customers broad market knowledge, resources

at all levels of its worldwide organization, and

extensive research and development capabilities

that have enabled the Company to provide its

customers with innovative products. They meet

their customers’ beverage packaging needs with an

array of two-piece beverage cans and ends, and

metal bottle caps. Innovations include the

SuperEnd® beverage can end, shaped beverage

cans which include size differentiation, such as slim

line cans for low calorie products or larger sizes for

high volume consumption.

Beverage can manufacturing is capital intensive,

requiring significant investment in tools and

machinery. Crown is currently seeking to

effectively manage its invested capital while also

continuing its research and development efforts to

reduce can and end diameter, lighten the metal

content of its cans, reduce non-metal costs, and

reduce water and energy usage while improving

production processes.

Food Packaging and Closures

The Company manufactures a variety of food cans

and ends, including two and three-piece cans in

numerous shapes and sizes. They sell these food

cans to food marketers such as Bonduelle, Cecab,

Mars, Simmons Foods, Nestlé, Princes Group and

Stockmeyer. The Company offers a wide variety of

metal vacuum closures and sealing equipment

solutions to leading marketers such as Abbot

Laboratories, Danone, H. J. Heinz, Nestlé, Premier

Foods, and Unilever. Crown supplies total

packaging solutions, including metal and composite

closures, and capping systems and services.

Additionally the Company works closely with

customers, retailers, and glass and plastic container

manufacturers to develop innovative closure

solutions and meet customer requirements.

Technologies used to produce food cans include

three-piece welded, two-piece drawn and wall-

0 1000 2000 3000

Amercas Beverage

North America Food

European Beverage

European Food

Asia Pacific

Non-Reportable

Segments

Sales (in Millions of Dollars)

Sales by Reportable Segment

2011 2012 2013

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2011 2012 2013

Sales Growth by Reportable Setment

Amercas

Beverage

North America

Food

European

Beverage

European Food

Asia Pacific

Non-Reportable

Segments

5. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 5 of 20

ironed, as well as two-piece drawn and redrawn.

The Company also offers its LIFTOFF™ series of

food ends, including its Easylift™ full aperture steel

food can ends, and PeelSeam™, a flexible

aluminum foil laminated end.

Crown offers expertise in closure design and

decoration, ranging from quality printing in up to

nine colors, to inside-the-cap printing, which offers

customers new promotional possibilities. The

Company’s commitment to innovation has led to

developments in packaging materials, surface

finishes, can shaping, lithography, filling, sealing

and opening techniques, and improved

environmental performance. The Company

manufactures easy-to-open, vacuum sealed, and

traditional can ends for a large variety of heat-

processed and dry food products including fruits

and vegetables, meat, seafood, soups, ready-made

meals, infant formula, coffee, and pet food.

Specialty Packaging

The Company’s specialty packaging business is

primarily located in Europe and Asia. They produce

a wide variety of specialty containers with

numerous lid and closure variations. The

Company’s specialty packaging customers include

Abbott Laboratories, Akzo Nobel, Britvic, Kraft,

Mars, Nestlé, Nippon Paints, PPG, Tikkurlia Oy and

United Biscuits.

Business Segments

The company’s activities are usually divided into

five reportable business segments and one non-

reportable segment which contribute differently to

the overall performance of Crown: Americas

Beverage, North America Food, European

Beverage, European Food, and Asia Pacific.

Americas Beverage

The Americas Beverage segment manufactures

aluminum beverage cans and ends and steel

crowns and supplies a variety of customers from its

operations in the U.S., Brazil, Canada, Colombia,

and Mexico. The U.S. and Canadian beverage can

markets are mature markets which have

experienced slightly declining volumes in recent

years. In Brazil, the Company's sales unit volumes

have increased in recent years primarily due to

market growth. Crown recently began

construction on a new facility in northern Brazil

and expects to begin commercial shipments in the

first half of 2014.

North America Food

The North America Food segment manufactures

steel and aluminum food cans and ends and metal

vacuum closures. From their manufacturing

facilities they are able to supply a variety of

customers with operations in the U.S. and Canada.

The North American food can and closures market

is a mature market which has experienced stable to

slightly declining volumes in recent years.

European Beverage

The Company's European Beverage segment

manufactures steel and aluminum beverage cans

and ends, and supplies a variety of customers from

its operations throughout Eastern and Western

Europe, the Middle East, and North Africa. In

recent years, the European beverage can market

6. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 6 of 20

has been growing at approximately 4.7%, with

beverage cans increasing from 52% of total

revenue in 2011 to 56% in 2013.

European Food

The European Food segment manufactures steel

and aluminum food cans, ends, and metal vacuum

closures. Crown supplies a variety of customers

from its operations throughout Europe and Africa.

The European food can market is a mature market

which has experienced stable to slightly declining

volumes in recent years.

Asia Pacific

The Company's Asia Pacific segment primarily

consists of beverage can operations in Cambodia,

China, Malaysia, Singapore, Thailand, and Vietnam.

This segment also includes the Company's non-

beverage can operation of food cans and specialty

packaging in China, Singapore, Thailand, and

Vietnam. In recent years, Crown’s beverage can

businesses in Asia have experienced significant

growth.

In 2012, Crown commercialized new beverage can

plants in Putian, Ziyang and Heshan, China and

expanded capacity at its plant in Ho Chi Minh City,

Vietnam. In the fourth quarter of 2012, the

Company acquired an aluminum beverage can and

end production facility in Vietnam and also

acquired a controlling interest in Superior Multi-

Packaging Ltd. (“Superior”), a listed company on

the Singapore Exchange. Superior primarily

produces specialty packaging containers for

consumer products companies at its facilities in

China, Singapore, and Vietnam.

In the first quarter of 2013, the Crown

commercialized additional beverage can lines at its

facilities in Putian, China and Bangi, Malaysia. In

the second quarter of 2013, they also

commercialized new beverage can plants in

Danang, Vietnam and Bangkok, Thailand; and in

July, the Company began production at its new

plant in Sihanoukville, Cambodia.

Non-Reportable Segments

The Company's non-reportable segments includes

the aerosol can businesses in North America and

Europe, its specialty packaging business in Europe

and its tooling and equipment operations in the

U.S. and U.K. In recent years, their specialty

packaging and aerosol can businesses have

experienced slightly declining sales volumes.

Competitive Advantage

The Customer is Always Right

Most of Crown’s products are sold in highly

competitive markets, primarily differentiated on

price and quality. Crown is not the biggest or most

efficient of the manufacturing companies, so it is

unlikely that they will be able to compete based on

economies of scale. However, in contrast to their

bulky brethren, Crown has tremendous skill in die

forming and metal fabrication, crisp printing in up

to nine colors, unique packaging materials, and

new surface finishes, allowing them to much more

easily adapt to the customer’s needs. This inherent

flexibility allows Crown to sell to players of all sizes,

filling a niche opportunity ignored by their

competitors.

7. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 7 of 20

Location, Location, Location

Crown took the dramatic step of closing its largest

manufacturing facilities and moving their

operations closer to the customers, as opposed to

their source of raw-materials. Additionally,

because customers rarely keep containers on site,

Crown opts to keep more than a month’s inventory

on hand, reducing both delivery cost and time,

while improving customer satisfaction numbers

worldwide.

Recent News and Share Performance

On October 31, 2013, Crown announced an

agreement to buy Spanish food-can maker Mivisa

Envases SAU for €1.2 billion ($1.64 billion)

including debt from Blackstone Group, N+1

Mercapital and the company’s management.

Mivisa is the largest food can producer in the

Iberian Peninsula, with nine manufacturing

facilities in Spain and another in Morocco. The

move will increase Crown’s footprint in Europe and

the Middle East, where Crown generated over $4

billion in sales in 2013 (47% of revenues according

to Bloomberg).

In order to close the deal, Crown agreed to pay

nine times Mivisa’s EBITDA, whereas the average

EBITDA multiple in four recent acquisitions within

the industry during the past 5 years was only 7.7x,

implying that Crown paid a 16.8% premium above

recent market levels. This premium equates to an

additional $275 million in purchase price. Despite

the premium paid, the chart below shows there

was a significant upside reaction to the acquisition

announcement, with shares surging 7.3% the day

the news hit. Since that time however, shares of

CCK have failed to keep their momentum going,

increasing only 2.2% whereas the S&P 500 has

increased 4.4% during the same timeframe.

$37

$38

$39

$40

$41

$42

$43

$44

$45

$46

31-Oct

14-Nov

28-Nov

12-Dec

26-Dec

9-Jan

23-Jan

6-Feb

20-Feb

6-Mar

Crown Holdings Share Price

Since Announcement of Mivisa Acquisition

-2%

0%

2%

4%

6%

8%

10%

12%

31-Oct

14-Nov

28-Nov

12-Dec

26-Dec

9-Jan

23-Jan

6-Feb

20-Feb

6-Mar

Crown Holdings Recent Performance

Compared to S&P 500

CCK

S&P

8. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 8 of 20

Investment Thesis

This paragraph aims to provide a brief overview of

the current and projected market climate, the

drivers of the Metal and Glass Containers industry,

and a target price based on these assumptions. An

explanation of the company’s financial statements

and ratios will help assess the firm’s current

situation, as well as provide a benchmark to

compare our Discounted Cash Flow model against.

Key Fundamental and Economic Drivers

The materials sector as a whole is highly correlated

to Gross Domestic Product (96.5% correlation over

the past year), and Crown Holdings is no exception

to that rule. While Crown manufactures containers

for food and beverage products, these containers

are primarily used for discretionary goods, meaning

sales are good in times of expansion and poor in

times of contraction.

North America

While GDP numbers in the United States have

shown slow but consistent growth, the North

American segment in both food and beverage are

mature markets, with sales declining on average

over the previous 3 years. As such, Crown is relying

more and more on developing economies in order

to generate the expendable income necessary for

the purchase of their products.

International

Due to the ever strengthening link between world

economies, the slow recovery of US markets are

having positive effects on some developing nations,

as the rising tide effect lifts all boats. However,

recent numbers suggest that a slowdown is present

in China. A slowdown in China could be

catastrophic to the Company, as the Asia Pacific

segment represents the largest growth segment

companywide. Additionally, a slowdown in China

could have far reaching effects to the world

economy, giving question as to whether the recent

uptrend in the materials sector is sustainable.

Chinese infrastructure spending has slowed

significantly, coupled with a weakening of the

Yuan. With both money growth and loan growth

decelerating, a sudden reacceleration in the

Chinese economy is unlikely, and I see this as a

headwind for the materials sector. Sluggish

economic data out of China and other emerging

markets give me pause as to whether CCK will be

able to achieve the lofty earnings estimates set

forth by analysts following the name.

Financial Analysis

A copy of the total pro forma income statement

can be found in appendix 1 on page 15. The

following paragraphs present and explain the

various assumptions used for the calculations as

well as the main takeaways from the analysis.

Revenue

As previously mentioned, Crown Holdings is

experiencing a decline in sales in their North

America segments due to the maturity of the

markets. That decline is being offset by

accelerating revenues out of their Asia Pacific

segment as well as their European Beverage

segment. The European Food segment was hit

9. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 9 of 20

hard due to the European Debt crisis and ensuing

European recession, but revenues are accelerating

once again. I expect the Company to grow sales at

a pace of 3%, coming in above the 0.9% they have

averaged throughout the previous five years, but in

line with the three year average. Historically

Crown has averaged 3.3% growth, but I believe

they will fall short of this number in the

foreseeable future as I am concerned with the

prospect of a Chinese slowdown.

Operating Margins

Crown has publicly stated during recent conference

calls as well as SEC filings that they would like to

positively influence their sales and administrative

expenses in order to improve margins. In the

previous five years, they have on average seen a

0.10% improvement, and I see this trend

continuing for an estimated three additional years.

However, it is only possible to cut costs so much,

and I feel it imprudent to assume that continued

cost cutting will continue beyond three years.

Share Buyback

Earnings per share have seen an upward

movement in recent years due in part to the

continuously decreasing outstanding share count.

During each of the previous three years, Crown has

purchased and retired approximately 4.5% of

outstanding shares, taking the total from 162.4

million in 2010 down to the current level of 138.4.

During this time period, interest rates have been

kept artificially low by the Federal Reserve,

allowing Crown to roll over debt at beneficial

levels. Low interest expense, coupled with strong

cash flows have resulted in a shareholder friendly

environment, and once again, I expect this pattern

to continue.

Peer Comparison

Metric (ttm) CCK OI BLL SLGN

Market Cap: 5.97B 5.42B 7.58B 3.09B

Revenue: 8.66B 6.97B 8.47B 3.71B

Gross Margin: 15.47% 19.08% 18.77% 14.74%

EBITDA: 1.05B 1.15B 1.17B 0.50B

Op. Margin: 10.59% 10.95% 10.32% 9.19%

Net Income: 324M 202M 406M 185M

Diluted EPS: 2.30$ 1.11$ 2.73$ 2.87$

P/E: 19.07 29.61 19.75 19.68

Crown Holdings main competitors within the metal

and glass containers sub-industry of the materials

sector are Owens-Illinois (OI), Ball Corp (BLL), and

Silgan Holdings (SLGN). Ball Corp represents

Crown’s closest competitor, as they offer metal

beverage, food, and aerosol containers to a

worldwide customer base.

Despite having a significantly smaller Market Cap

($5.97B vs $7.58B), the Company actually comes in

slightly higher in revenue ($8.66B vs $8.47B).

Crown Holdings’ gross margins are 3.3% lower than

that of Ball Corp, however, when it comes to

operating margins, Crown actually achieved a

number 0.27% superior to Ball Corp.

Liquidity Analysis

A reading of 0.67 for the more conservative quick

ratio shows that Crown does not have enough

liquid assets minus inventories to cover their short

term financial obligations. With a current ratio of

1.09, Crown has $1.09 in liquid assets for every

$1.00 of short-term obligations. While Crown

10. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 10 of 20

would be able to cover their debts, a 1.09 ratio

does not suggest an incredibly stable balance

sheet.

Discounted Cash Flow Analysis

A Discounted Cash Flow model has been included

as Appendix 3 (page 18) of this report, combining

data projected forward as part of the Income

Statement, Balance Sheet, and Statement of Cash

Flows. Despite a Terminal Growth Rate of 3.3% to

reflect the long-term growth rate of this 122 year

old company (a figure I believe to be generous), as

well as a 10% discount rate (a number often used

to value the market, but still relatively cheap

compared to most stocks within the basic materials

sector), my price target only amounted to $37.31,

representing a fair value 15.0% below the closing

price as of March 28, 2014.

Due to the lenient growth and discount rates

applied to the model, I opted to perform a

sensitivity analysis to show the reasonable range of

possible price targets. Using growth rates ranging

from 2.1% to 4.5% and discount rates ranging from

8% to 12%, I calculated price targets from $25.22

up to an unlikely figure of $71.06.

Multiple Analysis

Another useful approach to valuation of a company

involves comparing multiples to that of its

benchmark, sector, and industry. This helps to

determine if the stock is currently trading at a

discount, is fairly valued, or is selling at a premium

compared to its peers.

Relative to the S&P 500 Benchmark

The current share price reflects the 10 year

historical average when compared to Sales and

Cash Flows per share, and actually reflects a slight

discount versus historical earnings figures.

However, the Price-to-Book number is at the 10

year high point, 2.6 times the historical average of

3.3.

Relative to

S&P 500 High Low Median Current

Trailing P/E 11.5 0.7 1.0 0.9

Forward P/E 1.2 0.7 0.9 0.8

P/B 8.7 2.7 3.3 8.7

P/S 0.6 0.1 0.4 0.4

P/CF 1.3 0.4 0.9 0.9

Relative to its Sector

When compared to its peers within the materials

sector, the Price-to-Sales and Price-to-Cash Flows

once again are at their historical average. As with

the S&P 500 comparison, it appears that Crown is

again trading at a slight discount compared to its

current and projected earnings. However, similarly

to the S&P comparison, the price-to-book ratio is

once again at the historical high, approximately

twice the average level. This could mean that

investors have high hopes for growth in the

Relative to

Sector High Low Median Current

Trailing P/E 9.7 0.4 1.0 0.7

Forward P/E 1.4 0.4 0.9 0.8

P/B 7.3 2.7 3.7 7.3

P/S 0.8 0.2 0.5 0.5

P/CF 1.4 0.5 0.9 1.0

11. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 11 of 20

company, a figure not backed up by the low

forward price-to-earnings ratio.

Relative to its Industry

We see more of the same when looking at the

comparison of Crown versus its industry group. We

actually see a slight overvaluation when compared

to sales this time, but once again a slight discount

versus trailing price-to-earnings. In this instance,

the forward looking price-to-earnings number is in-

line with historical averages, but the price-to-book

number is once again at the 10 year high and

extremely elevated compared to averages.

Relative to

Industry High Low Median Current

Trailing P/E 12.9 0.8 1.1 1.0

Forward P/E 1.4 0.7 1.1 1.1

P/B 4.7 1.9 2.7 4.7

P/S 1.1 0.2 0.7 0.8

P/CF 1.9 0.5 1.3 1.3

Crown Multiples Evaluation

Relative valuations all seem to indicate that CCK is

trading at a fair to slightly discounted level, with

the exception of the price-to-book, which is

running counter to each of the other valuations.

That being said, I’ve use combined target multiples

with forecasted values for earnings, book value,

sales, cash flow, and EBITDA per share to produce

the following table:

Forward P/E21.1 8.5 12.9 13.3 2.52 13.0 32.76$

P/B 22.5 8.1 10.1 22.5 2.32 12.0 27.82$

P/S 0.8 0.2 0.6 0.7 67.00 0.6 40.20$

P/CF 12.2 4.2 8.7 10.8 3.03 10.0 30.30$

P/EBITDA 11.8 1.8 5.7 6.1 5.65 6.0 33.90$

Average of all target prices 33.00$

Average of target prices (excluding P/B) 34.29$

Upside/Downside potential -21.8%

The target price in this instance varies from $27.82

(P/B) to $40.20, with the average coming in at

$33.00. However, because the price-to-book

number has appeared so detached from the rest of

the relative valuations, I feel it is prudent to

eliminate this figure from our calculation. The

exclusion of the price-to-book target raises our

average target price to $34.29, showing a fair value

21.8% lower than the current market price of

$43.78.

12. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 12 of 20

Risks to the Recommendation

While I have attempted to consider as many

variables as possible, it must be mentioned that

forecasting is an inexact science. Risks exist both

internally and externally, domestically and abroad

that could radically effect the assumptions set

forth, resulting in drastically different earnings and

stock price figures from my target numbers.

External Risks

Any company that operates outside the borders of

the United States faces some risks, but Crown

Holdings is increasingly an international operation.

Crown generated 73% of their 2011 and 2012 sales

abroad, with the figure increasing to 74% in 2013,

and that number is expected to grow in the future

due to the Company’s business strategy and the

Mivisa acquisition. A significant majority of the

Company’s growth is expected to come via

expansion into the developing markets of Eastern

Europe, Asia, the Middle East, and South America.

A prolonged period of political or economic

stability could drive sales higher than estimated in

these regions, resulting in an upward movement in

share price.

Furthermore, if the current European sovereign

debt crisis continues its improvement, there will

likely be a positive effect on the Company's

European business, as well as the businesses of the

Company's European customers and suppliers. If

this crisis wanes and leads to a significant

improvement in the valuation of the euro, the

value of financial assets that are denominated in

euros would be significantly increased when

translated to U.S. dollars for financial reporting

purposes. Any of these conditions could ultimately

improve the Company's overall business,

prospects, operating results, financial condition,

and cash flows, and such improvement may be

more pronounced if the Company expands in

Western Europe through potential acquisitions or

otherwise.

In its consolidated financial statements, Crown

translates financial results from the local currency

into U.S. dollars based on average exchange rates

prevailing during a reporting period. During times

of a weakening U.S. dollar, its reported

international revenue and earnings will be

increased because the local currency will translate

into more U.S. dollars, again resulting in better-

than-expected earnings results.

Crown uses various raw materials for the

production of their finished good. The availability

of these materials and their prices depends on

global and local supply, as well as demand forces,

governmental regulations (including tariffs), levels

of production, resource availability, transportation,

and other factors. In recent years, the

consolidation of steel suppliers, shortage of raw

materials affecting the production of steel, and the

increased global demand for steel, especially in

China, have contributed to an overall tighter supply

for steel, resulting in increased steel prices and

allocated cut backs of products by steel suppliers.

In 2013, steel and aluminum represented 25% and

39% respectively of the cost of goods sold. While

Crown passes most of the raw materials costs on to

their customers, the slowdown in the Chinese

economy may result in lower steel prices,

13. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 13 of 20

eliminating the threat of compressed margins due

to an inability to pass on price movements.

Crown has a substantial level of outstanding debt,

with the Mivisa acquisition only increasing that

indebtedness further. As a result, a significant

portion of the Company's cash flows are required

to pay interest and principal. Sales outpacing

expectations would result in increased cash flows,

improving their balance sheet and future

borrowing prospects available under their senior

secured credit facilities, allowing Crown to fund

future liquidity needs.

As of December 31, 2013, approximately $850

million of the Company's $3.8 billion of total

outstanding obligations were subject to floating

interest rates. The Company's annual interest

expense was $236 million, $226 million and $232

million for 2013, 2012 and 2011, respectively.

Based on the amount of variable rate debt

outstanding at December 31, 2013, a 1% increase

in variable interest rates would increase its annual

interest expense by $8.5 million. Negative changes

in economic conditions could result in the

continuation of artificially low interest rates,

thereby locking in the Company's interest expense

and stabilizing funds available for other projects.

14. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 14 of 20

Conclusion

Utilizing the bottom up approach of a Discount

Cash Flow model with an assumed terminal growth

rate of 3.3% and a discount rate of 10%, I came to a

target price of $37.31, which results in a potential

downside of 15%. Through using multiple

valuation methods, I calculated a price target of

$34.29, or a potential downside of 27.9% from the

closing price on March 28th

, 2014.

Due to the nature of multiples valuation versus the

discounted cash flow method, I am going to

assume that the DCF model is the more accurate

estimation of worth. After combining the two

targets, allowing for a weighting of 67% for the DCF

and 33% for the multiples valuation target, I came

to a final price target of $36.00, representing a

potential downside of 21.8%.

Final Price Target

Calculation

Price

Valuation

Weight

Potential

Upside /

Downside

Current Price 43.87$

Discounted Cash Flow

Price Target 37.31$ 67% -15.0%

Multiples Valuation

Price Targe 34.29$ 33% -21.8%

Final Price Target 36.00$ -17.9%

Recommendation

I recommend a SELL rating for Crown Holdings, Inc.

(CCK) for the following previously stated reasons:

Recent numbers suggest that a slowdown is

present in China. A slowdown in China could be

catastrophic to the Company, as the Asia Pacific

segment represents the largest growth

segment companywide. Additionally, a

slowdown in China could have far reaching

effects to the world economy, giving question

as to whether the recent uptrend in the

materials sector is sustainable.

Consensus estimates are calling for a for an

average earnings increase of 22% each of the

next three years on an average sales increase of

3%. While the historical sales growth rate has

been 4%, the average increase since 2008 has

come in just shy of 1%, and I believe the rosy

3% estimates have already been baked in to the

overvalued share price.

I believe Crown overpaid for their acquisition of

Mivisa Envases. Not only did Crown pay an

estimated $275 million above the market value

of the company, they took on a substantial

amount of debt in the process.

With the Federal Reserve winding down its

bond buying program and publically

announcing its intention to begin raising

interest rates six months after the program

ends, I fully expect borrowing rates to increase

proportionately. Currently the Company has

$850 million in debt, subject to floating rates,

so if sales come in below expectations and cash

flows are unable to cover obligations, Crown

will need to rollover their debt at higher rates,

further exacerbating the problem.

Company: Crown Holding, Inc.

Ticker: CCK

Current Price: $43.87 (March 28, 2014)

Target Price: $36.00

Recommendation: SELL

Analyst: Martin Smith

15. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 15 of 20

Appendixes

Appendix 1: Forecast of Income Statement

A. Income Statement

Summary of Operations 2008 2009 2010 2011 2012 2013 2014 E 2015E 2016E

Net sales 8,305$ 7,938$ 7,941$ 8,644$ 8,470$ 8,656$ 8,916$ 9,183$ 9,459$

Cost of products sold 6885 6551 6519 7120 7013 7180 7,406 7,628 7,857

Depreciation and amortization 216 194 172 176 180 134 138 142 146

Gross profit 1,204$ 1,193$ 1,250$ 1,348$ 1,277$ 1,342$ 1,372$ 1,413$ 1,456$

Gross Margin 14.5% 15.0% 15.7% 15.6% 15.1% 15.5% 15.4% 15.4% 15.4%

Selling and administrative expense 396 381 360 395 382 425 417 421 424

Provision for asbestos 25 55 46 28 35 32 40 41 42

Provision for restructuring 21 43 42 77 48 46 47 49 50

Asset impairments and sales 6 (6) (18) 6 (48) (12) (13) (13) (14)

Income from operations 756$ 720$ 820$ 842$ 860$ 851$ 880$ 916$ 953$

Interest expense 291 241 194 221 226 236 252 259 267

Loss from early extinguishments of debt 2 26 16 32 0 41 21 21 22

Interest income 21 (6) (4) 2 (7) (5) 0 0 0

Foreign exchange (1) 3 0 0 0

Income before income taxes 442$ 459$ 614$ 587$ 642$ 576$ 608$ 635$ 663$

Provision for/(benefit from) income taxes 112 7 165 194 (17) 148 152 159 166

Equity earnings/(loss) (2) 3 3 5 0 0 0 0

Net income 330 450 452 396 664 428$ 456$ 476$ 498$

Net income attributable to noncontrolling interests (104) (116) (128) (114) (105) (104) (117) (123) (128)

Net income attributable to Crown Holdings 226$ 334$ 324$ 282$ 559$ 324$ 338$ 354$ 369$

Net Margin 2.7% 4.2% 4.1% 3.3% 6.6% 3.7% 3.8% 3.9% 3.9%

Average shares outstanding (diluted) 162.9 161.9 162.4 154.3 148.4 140.7 134.4 128.3 122.5

Earnings per Share (GAAP) 1.39$ 2.06$ 2.00$ 1.83$ 3.77$ 2.30$ 2.52$ 2.76$ 3.01$

16. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 16 of 20

B. Detailed Breakdown of Income Statement

Summary of Operations 2008 2009 2010 2011 2012 2013 2014 E 2015E 2016E

Net sales 8,305$ 7,938$ 7,941$ 8,644$ 8,470$ 8,656$ 8,916$ 9,183$ 9,459$

Sales Growth -4.4% 0.0% 8.9% -2.0% 2.2% 3.0% 3.0% 3.0%

Cost of products sold 6885 6551 6519 7120 7013 7180 7,406 7,628 7,857

(as percent of sales) 82.9% 82.5% 82.1% 82.4% 82.8% 82.9% 83.1% 83.1% 83.1%

Depreciation and amortization 216 194 172 176 180 134 138 142 146

(as percent of sales) 2.6% 2.4% 2.2% 2.0% 2.1% 1.5% 1.5% 1.5% 1.5%

Gross profit 1,204$ 1,193$ 1,250$ 1,348$ 1,277$ 1,342$ 1,372$ 1,413$ 1,456$

Gross Margin 14.5% 15.0% 15.7% 15.6% 15.1% 15.5% 15.4% 15.4% 15.4%

Selling and administrative expense 396 381 360 395 382 425 417 421 424

(as percent of sales) 4.8% 4.8% 4.5% 4.6% 4.5% 4.9% 4.7% 4.6% 4.5%

Provision for asbestos 25 55 46 28 35 32 40 41 42

(as percent of sales) 0.3% 0.7% 0.6% 0.3% 0.4% 0.4% 0.4% 0.4% 0.4%

Provision for restructuring 21 43 42 77 48 46 47 49 50

(as percent of sales) 0.3% 0.5% 0.5% 0.9% 0.6% 0.5% 0.5% 0.5% 0.5%

Asset impairments and sales 6 (6) (18) 6 (48) (12) (13) (13) (14)

(as percent of sales) 0.1% -0.1% -0.2% 0.1% -0.6% -0.1% -0.1% -0.1% -0.1%

Income from operations 756$ 720$ 820$ 842$ 860$ 851$ 880$ 916$ 953$

Interest expense 291 241 194 221 226 236 252 259 267

(as percent of sales) 3.5% 3.0% 2.4% 2.6% 2.7% 2.7% 2.8% 2.8% 2.8%

Loss from early extinguishments of debt 2 26 16 32 0 41 21 21 22

(as percent of sales) 0.0% 0.3% 0.2% 0.4% 0.0% 0.5% 0.2% 0.2% 0.2%

Interest income 21 (6) (4) 2 (7) (5) 0 0 0

Foreign exchange (1) 3 0 0 0

Income before income taxes 442$ 459$ 614$ 587$ 642$ 576$ 608$ 635$ 663$

Provision for/(benefit from) income taxes 112 7 165 194 (17) 148 152 159 166

(as percent of sales) 25.3% 1.5% 26.9% 33.0% -2.6% 25.7% 25.0% 25.0% 25.0%

Equity earnings/(loss) (2) 3 3 5 0 0 0 0

Net income 330 450 452 396 664 428$ 456$ 476$ 498$

Net income attributable to noncontrolling interests (104) (116) (128) (114) (105) (104) (117) (123) (128)

(as percent of sales) -31.5% -25.8% -28.3% -28.8% -15.8% -24.3% -25.8% -25.8% -25.8%

Net income attributable to Crown Holdings 226$ 334$ 324$ 282$ 559$ 324$ 338$ 354$ 369$

Net Margin 2.7% 4.2% 4.1% 3.3% 6.6% 3.7% 3.8% 3.9% 3.9%

17. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 17 of 20

Appendix 2: Select Balance Sheet a Cash Flow Figures

2008 2009 2010 2011 2012 2013 2014 E 2015E 2016E

Balance Sheet

Assets

Receivables, net 734 714 936 948 1057 1064 1,158 1,256 1,359

(as percent of sales) 8.8% 9.0% 11.8% 11.0% 12.5% 12.3% 13.0% 13.7% 14.4%

Inventories 979 960 1060 1148 1166 1213 1,289 1,369 1,452

(as percent of sales) 11.8% 12.1% 13.3% 13.3% 13.8% 14.0% 14.5% 14.9% 15.3%

Liabilities and equity

Accounts payable and accrued liabilities 1,982 1,866 1,978 2,090 2,146 2,547 2,325 2,428 2,536

(as percent of sales) 23.9% 23.5% 24.9% 24.2% 25.3% 29.4% 26.1% 26.4% 26.8%

Statement of Cash Flows

Cash flows from operating activities

Depreciation and amortization 216 194 172 176 180 134 138 142 146

(as percent of sales) 2.6% 2.4% 2.2% 2.0% 2.1% 1.5% 1.5% 1.5% 1.5%

Cash flows from investing activities

Capital expenditures (174) (180) (320) (401) (324) (275) (298) (307) (316)

(as percent of sales) -2.1% -2.3% -4.0% -4.6% -3.8% -3.2% -3.3% -3.3% -3.3%

20. CCK: Crown Holdings, Inc. – Equity Research Project Martin Smith

Student Investment Management Spring 2014 Page 20 of 20

Sources

Crown Holdings, Inc. SEC Filings: 2010, 2011, 2012, and 2013 (Form 10-K)

Crown Holdings, Inc. FY 2013 Earnings Call Transcript

Crown Holdings, Inc. Corporate Website: www.crowncork.com

Standard & Poor’s Capital IQ: Accessed at the Ohio State University

Bloomberg: Accessed at the Ohio State University

Thomson Reuters Baseline: Accessed at the Ohio State University

Charles Schwab: www.schwab.com

Zacks.com: http://www.zacks.com/stock/news/121869/Crown-Holdings-Misses-On-Q4-Earnings

Yahoo Finance: finance.yahoo.com

Google Finance: www.google.com/finance

Morningstar: www.morningstar.com

http://blog.bcaresearch.com/downgrading-the-u-s-sp-materials-sector

http://www.bloomberg.com/news/2013-10-31/crown-to-acquire-mivisa-for-1-64-billion-from-blackstone-n-

1.html