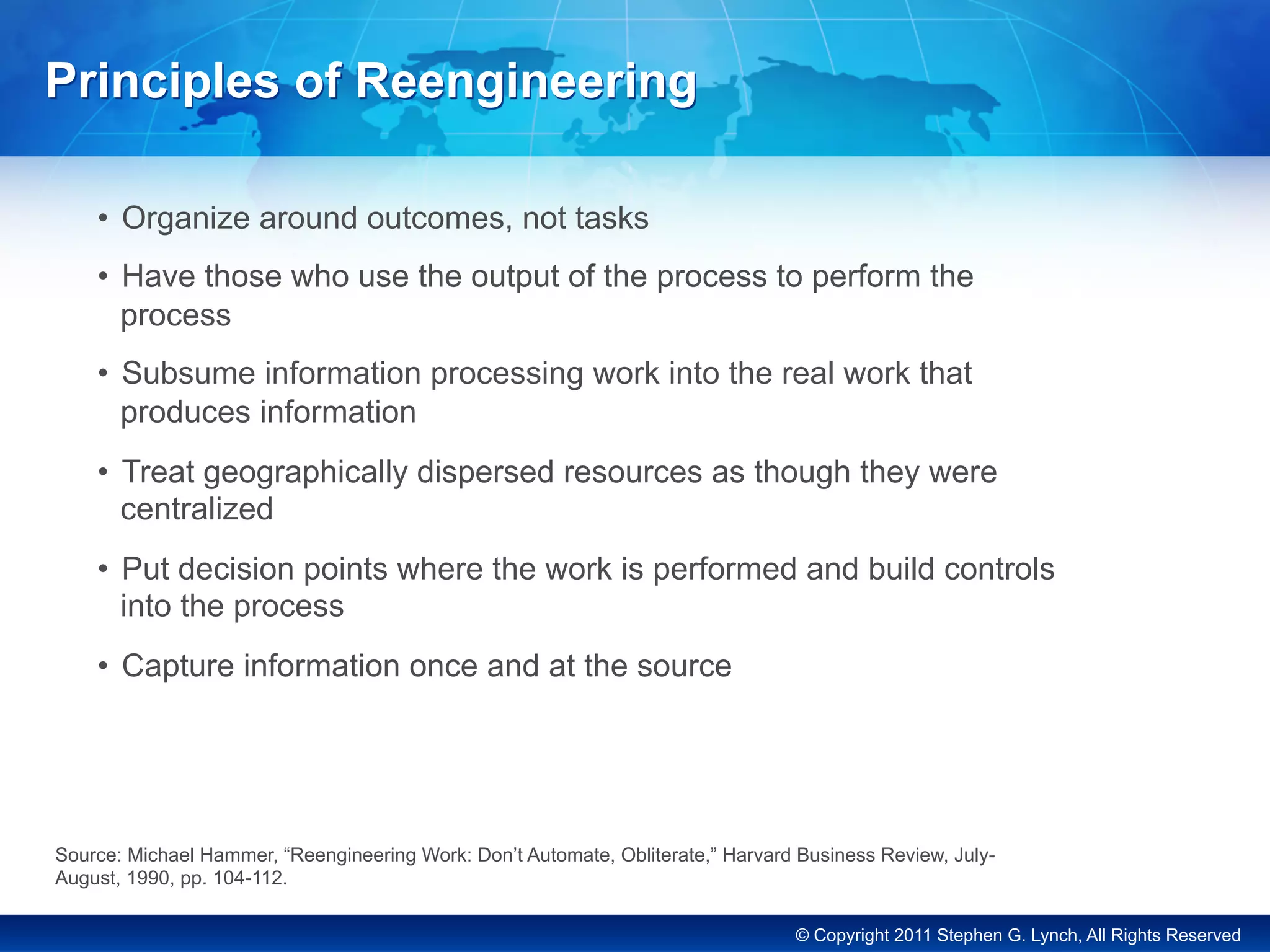

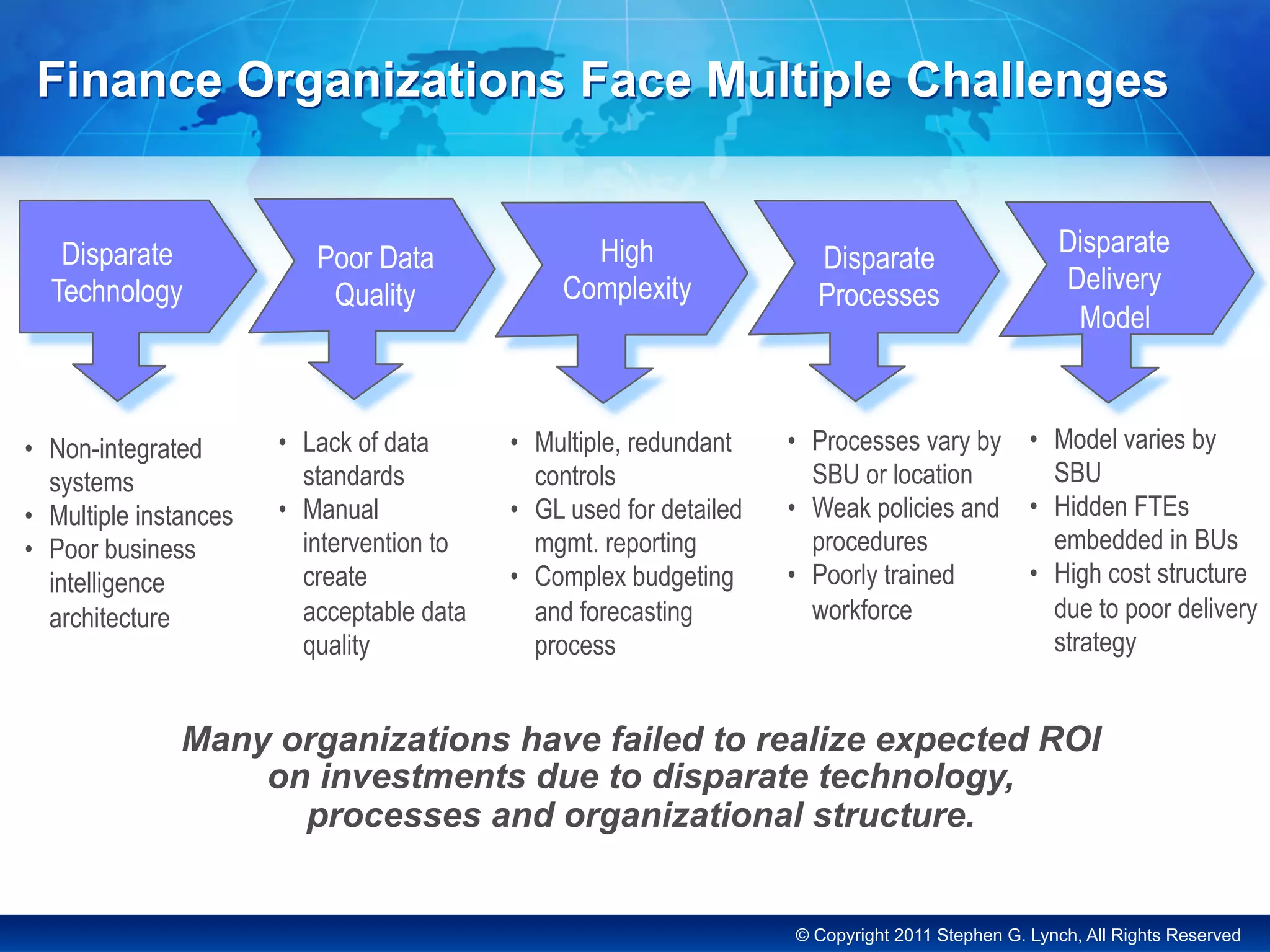

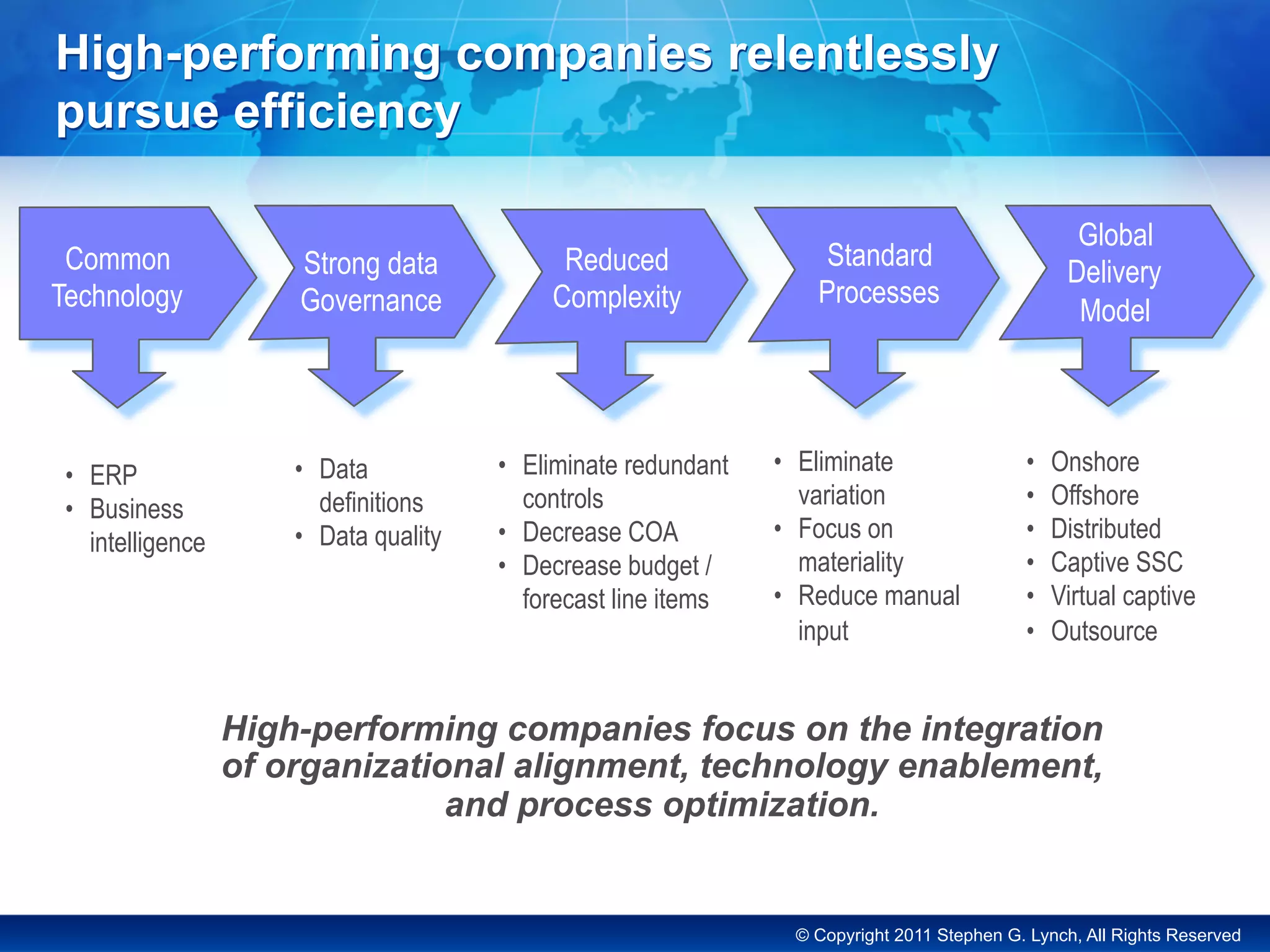

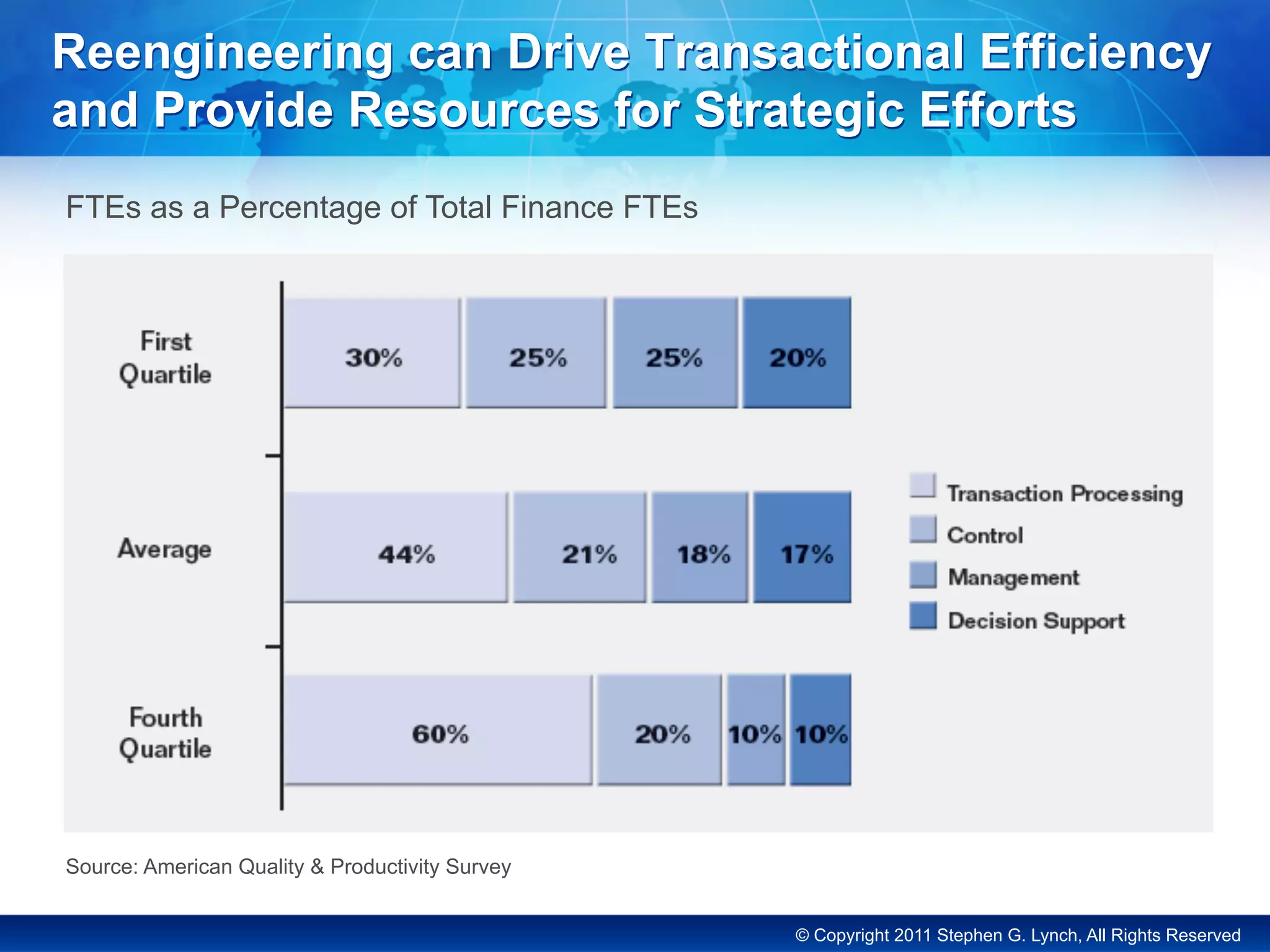

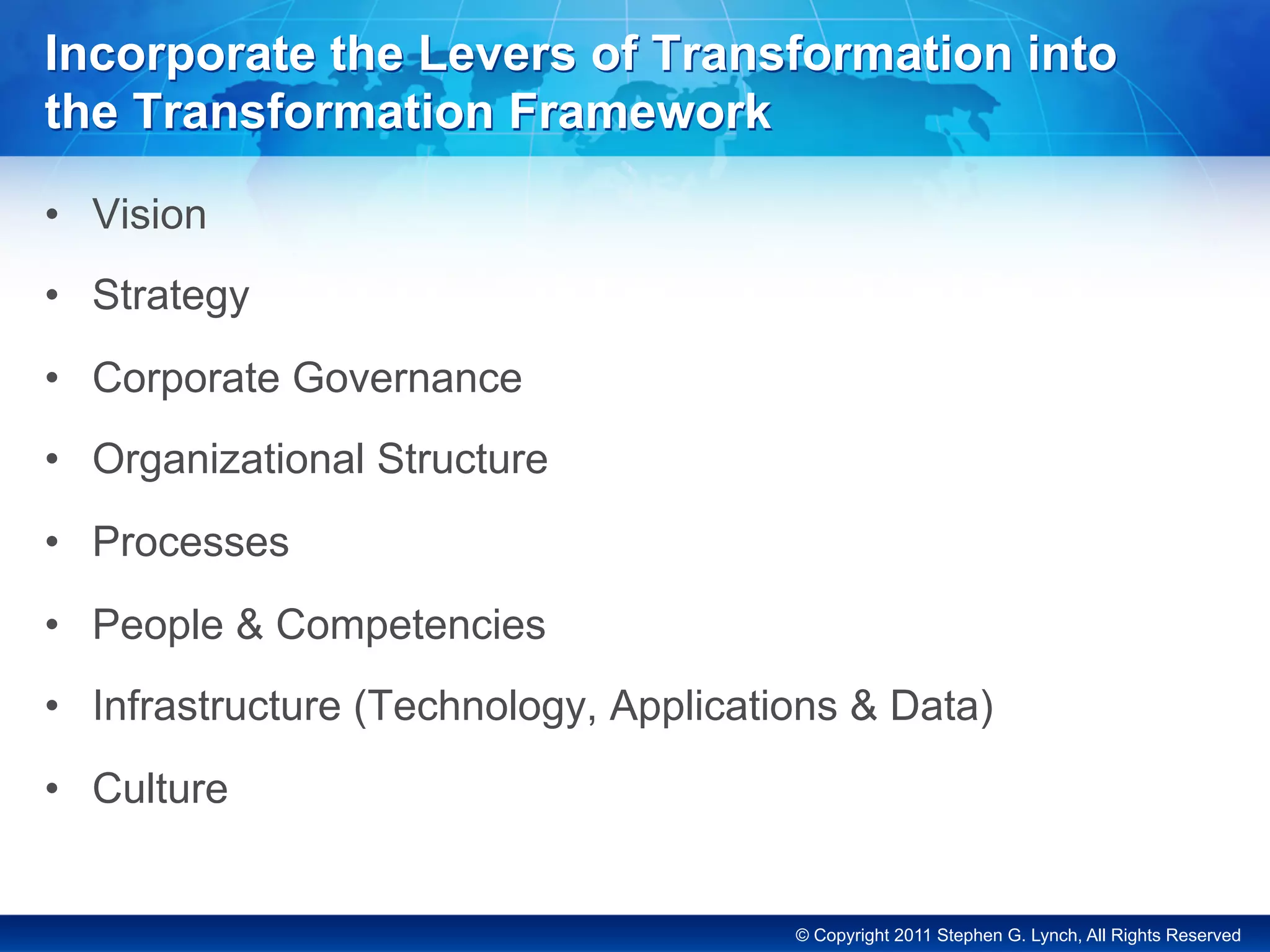

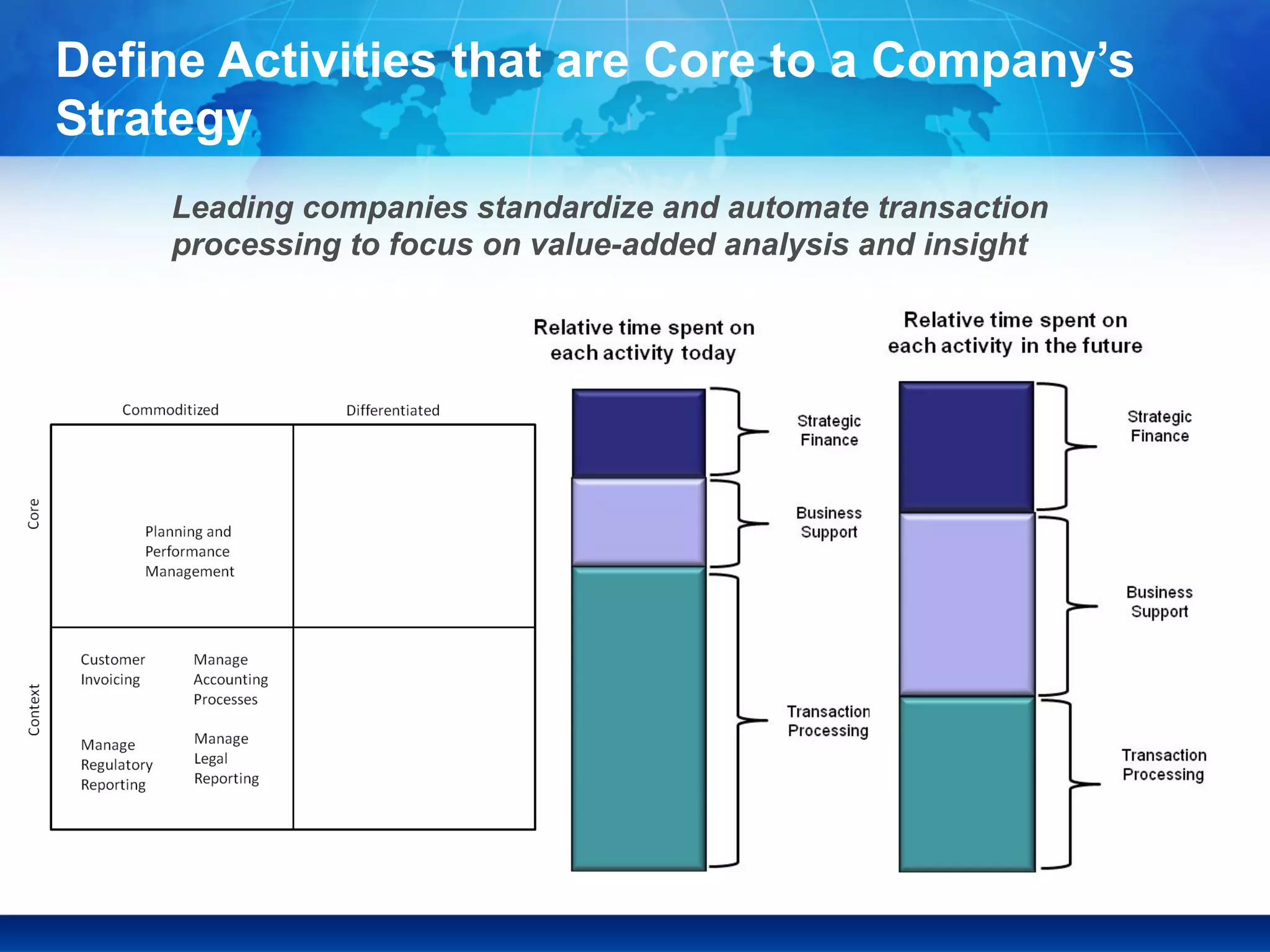

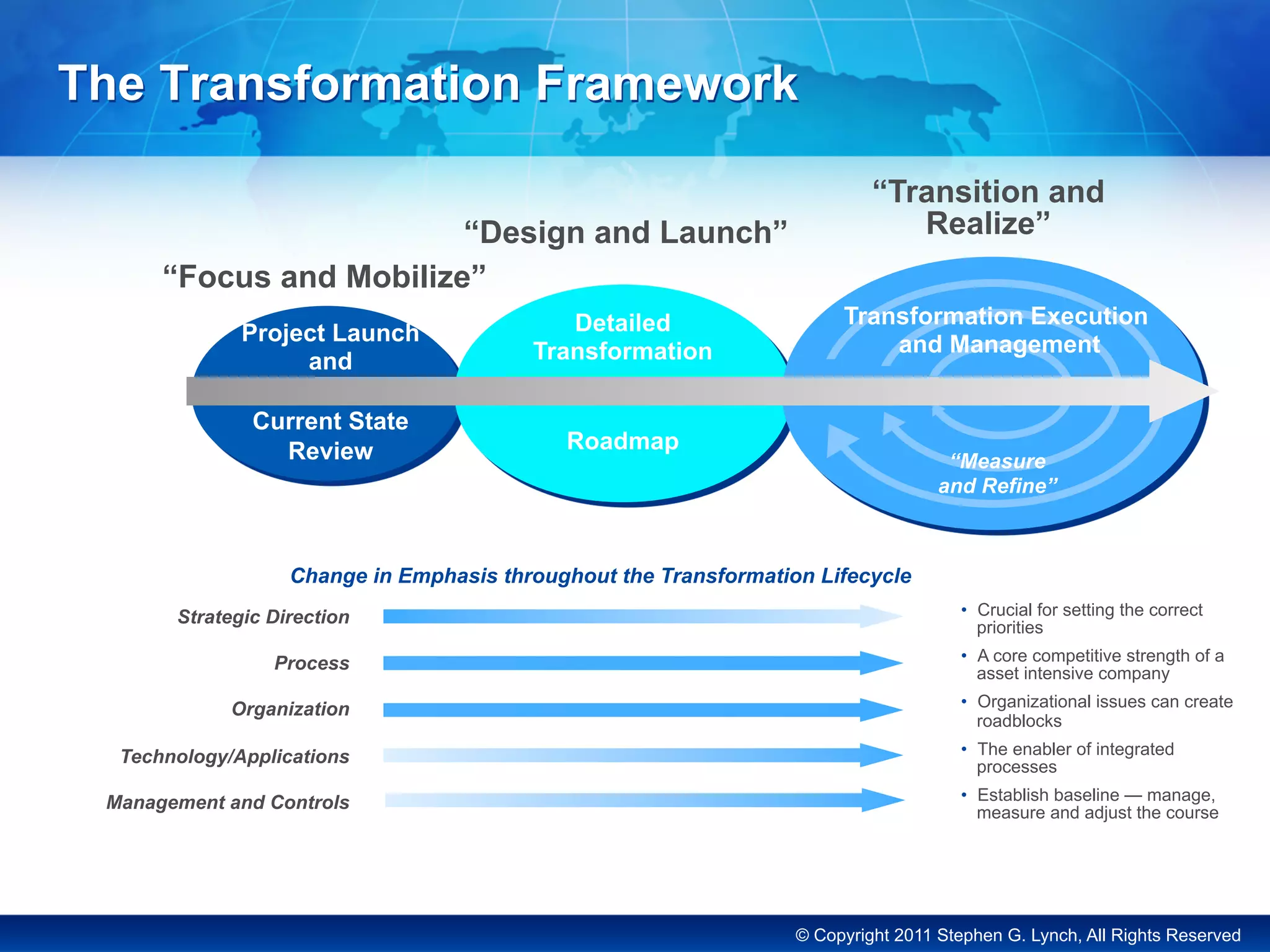

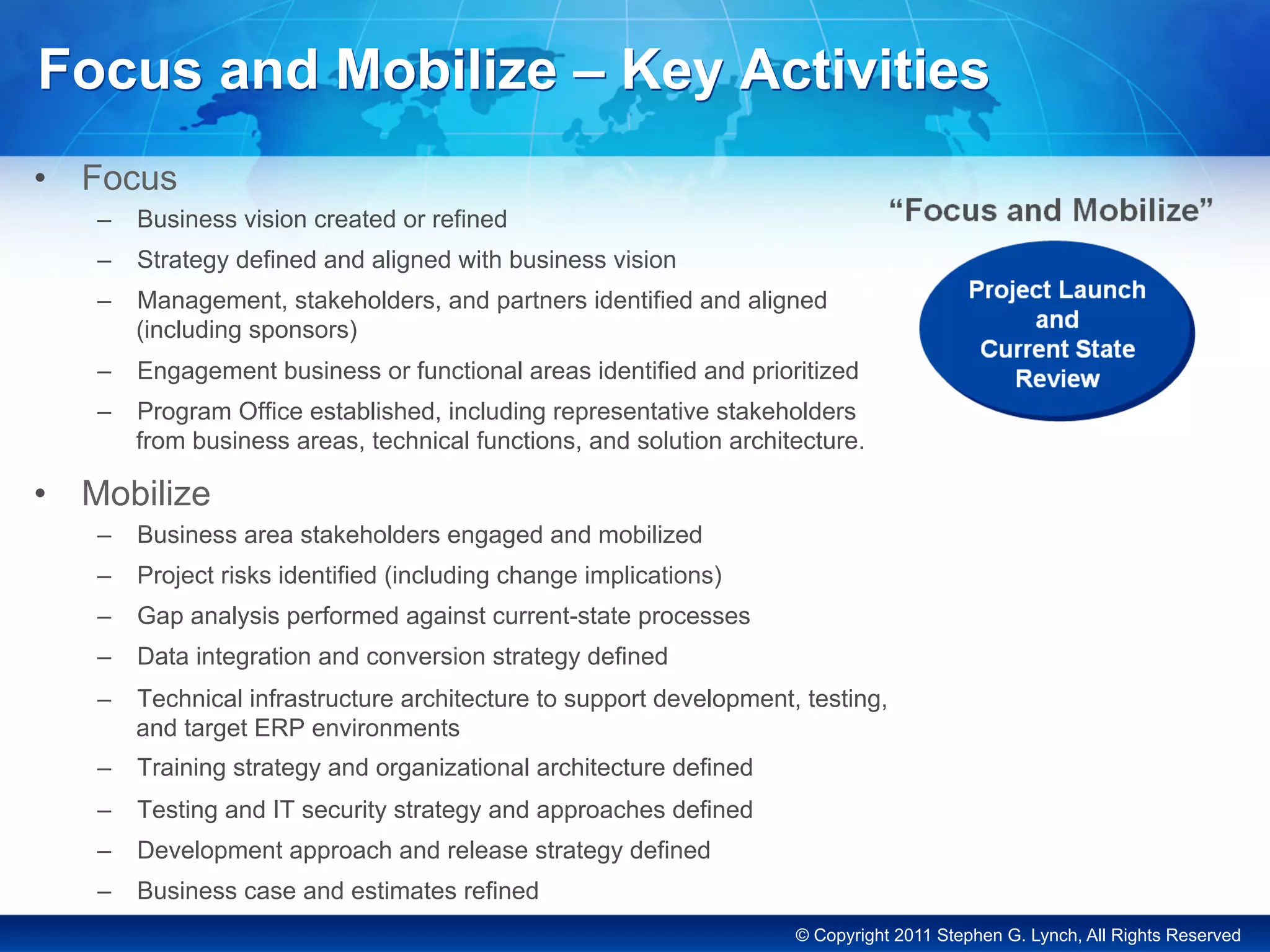

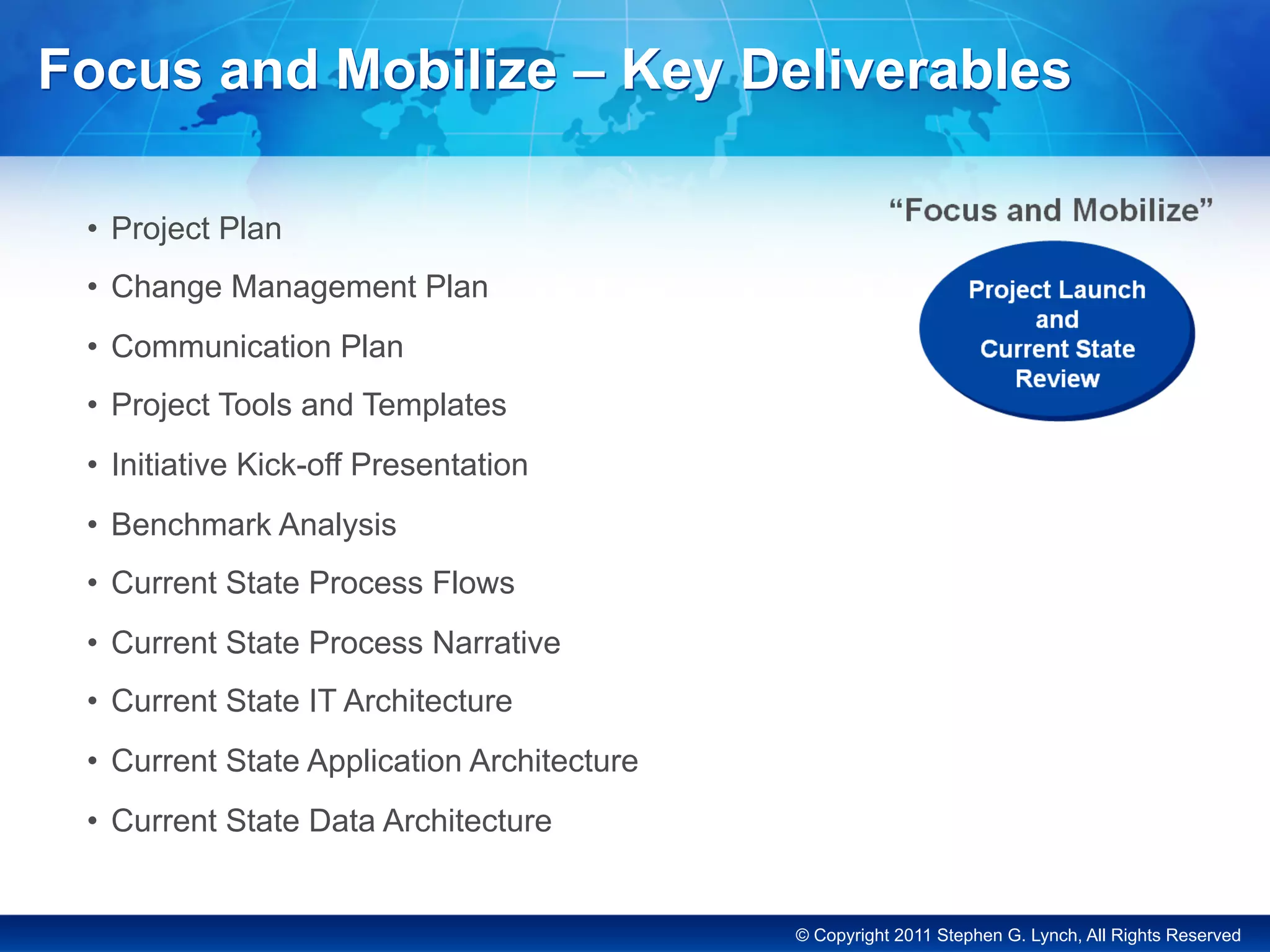

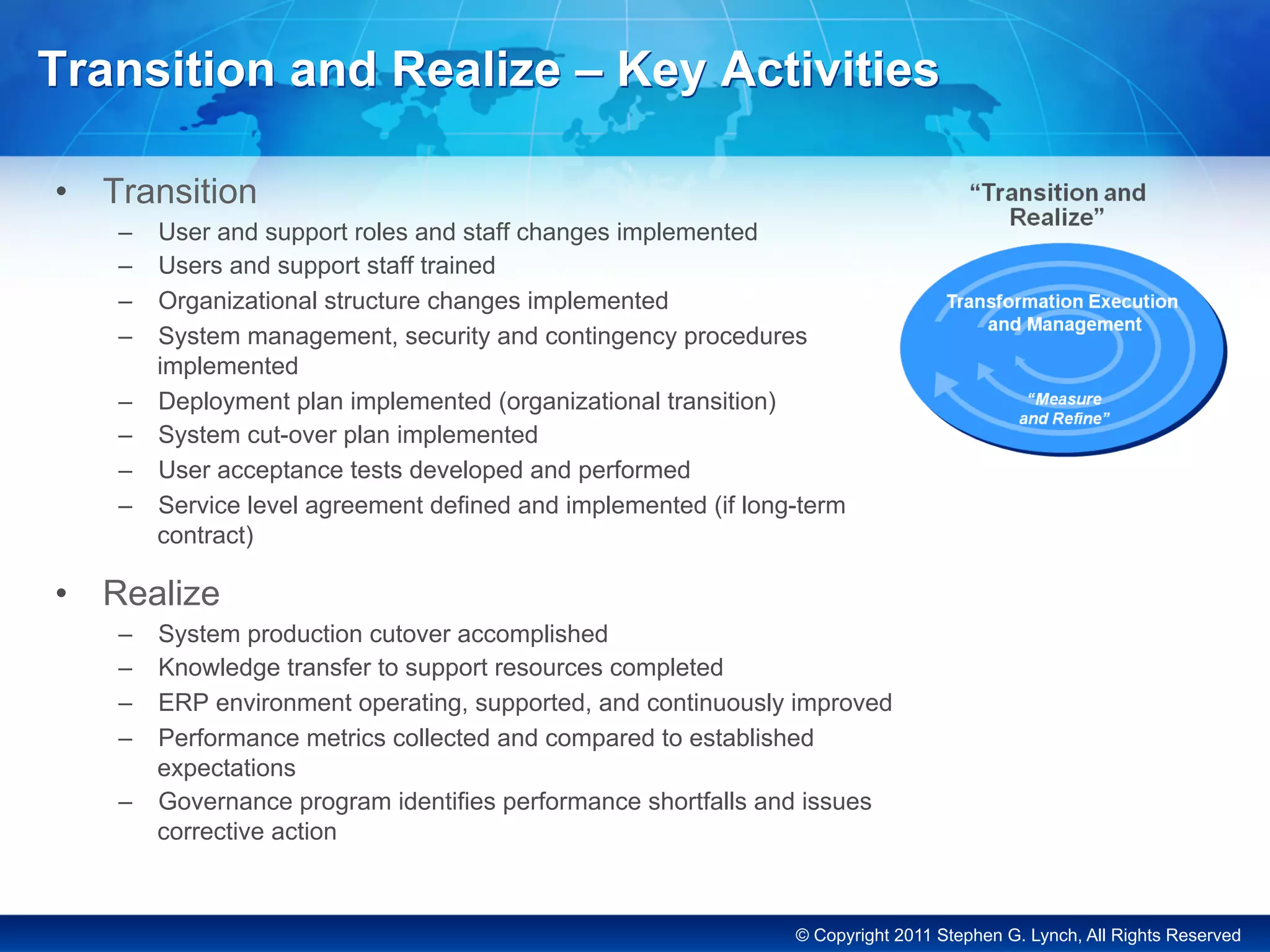

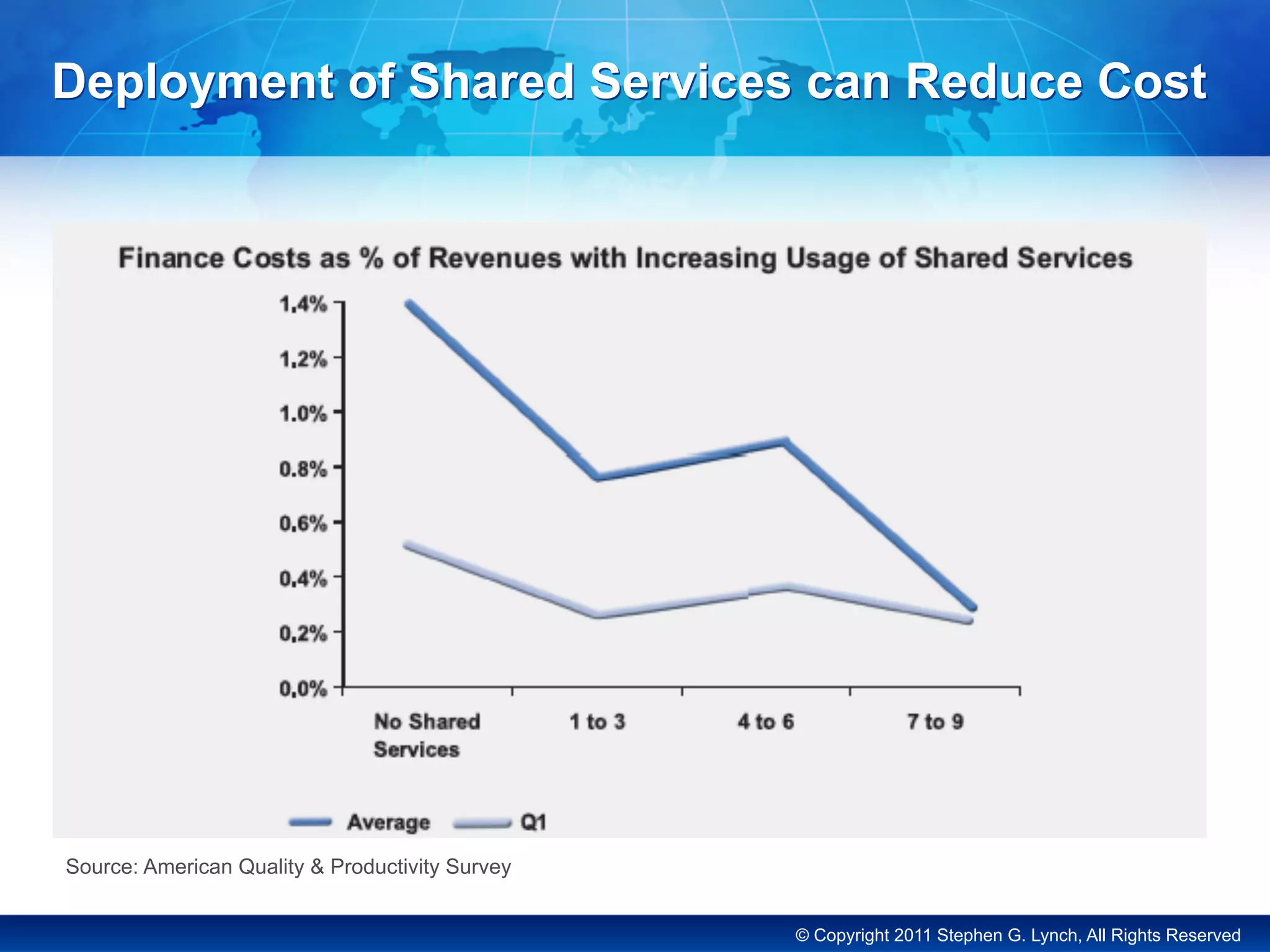

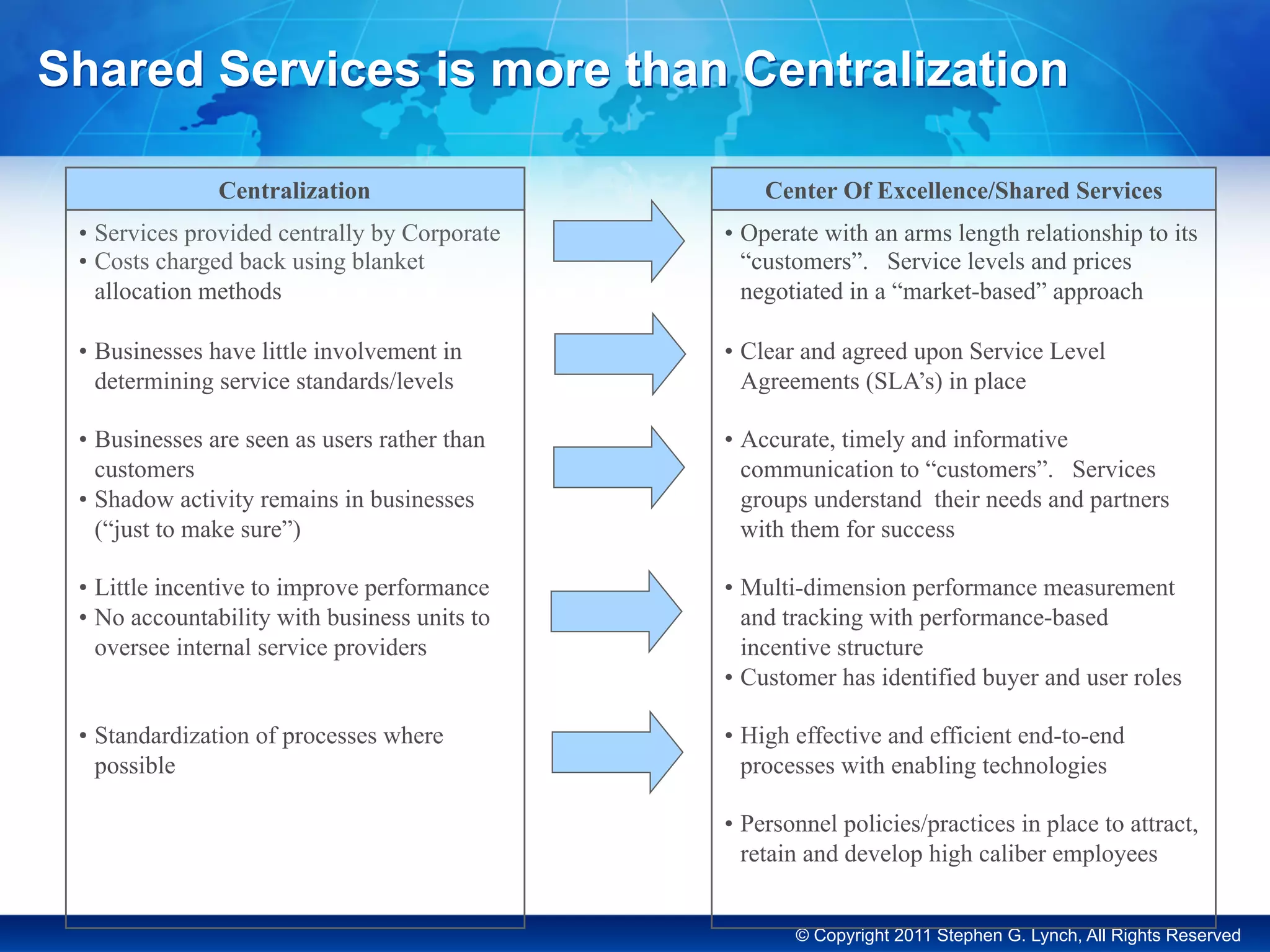

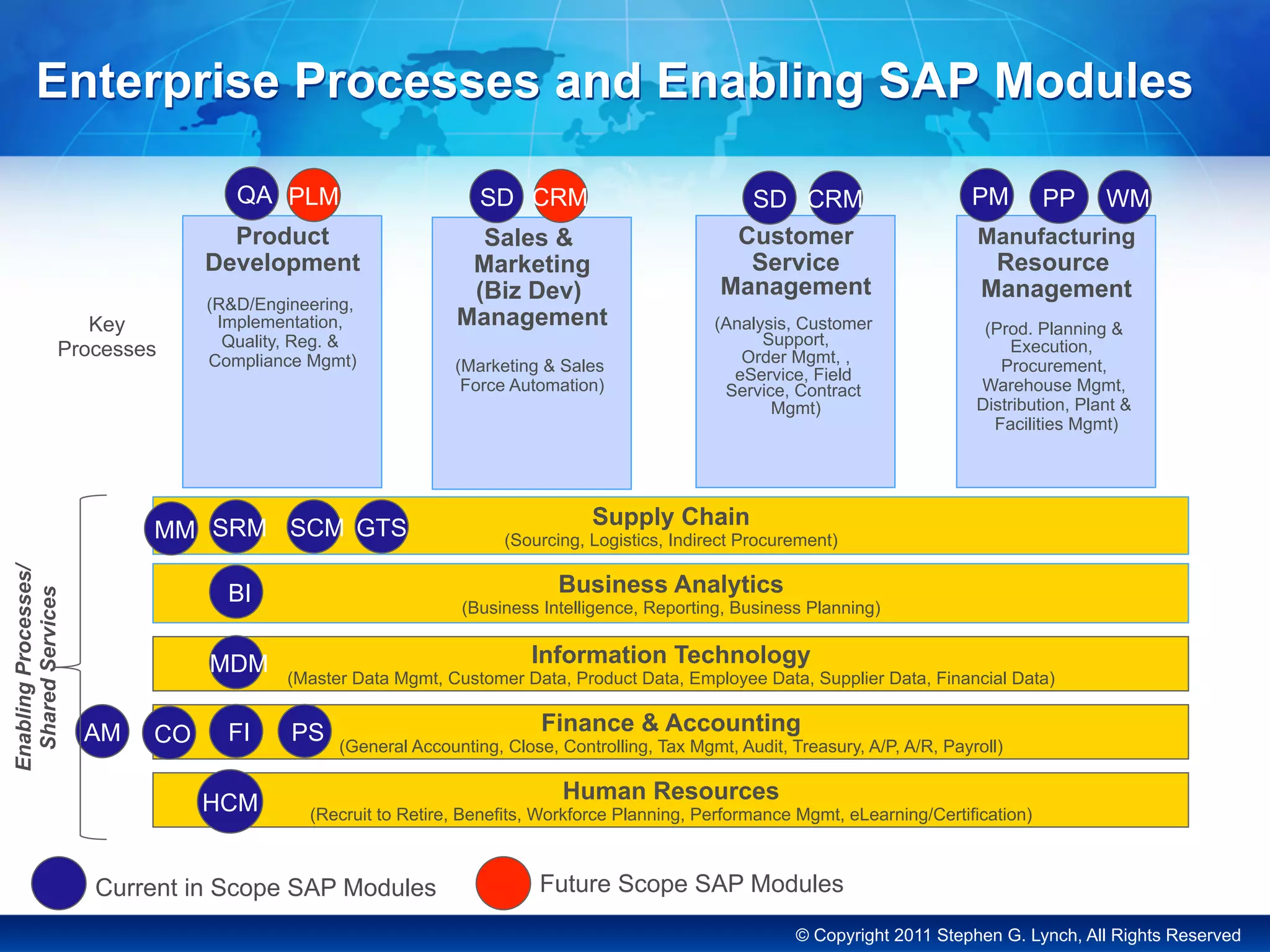

This document discusses reengineering the finance function. It begins by introducing the presenter and describing the goals of the workshop, which are to understand reengineering principles, frameworks, shared services, outsourcing trends, and managing change. It then discusses what reengineering is and principles such as organizing around outcomes. It describes challenges finance organizations face and how reengineering can address these. The transformation framework covers phases from project launch to transition and realization. Key activities and deliverables are outlined for each phase. Critical success factors like executive support and alignment with strategy are also noted.