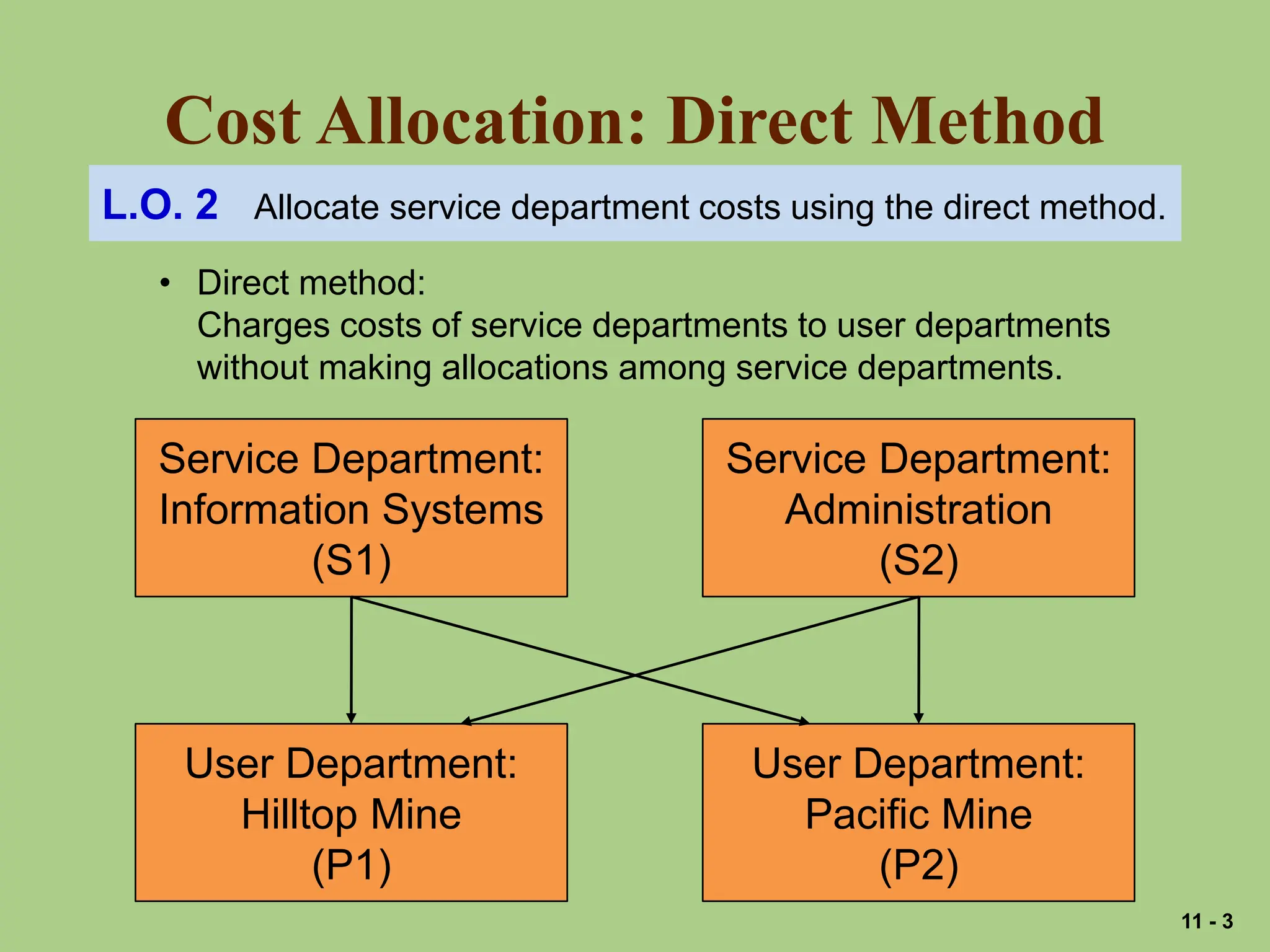

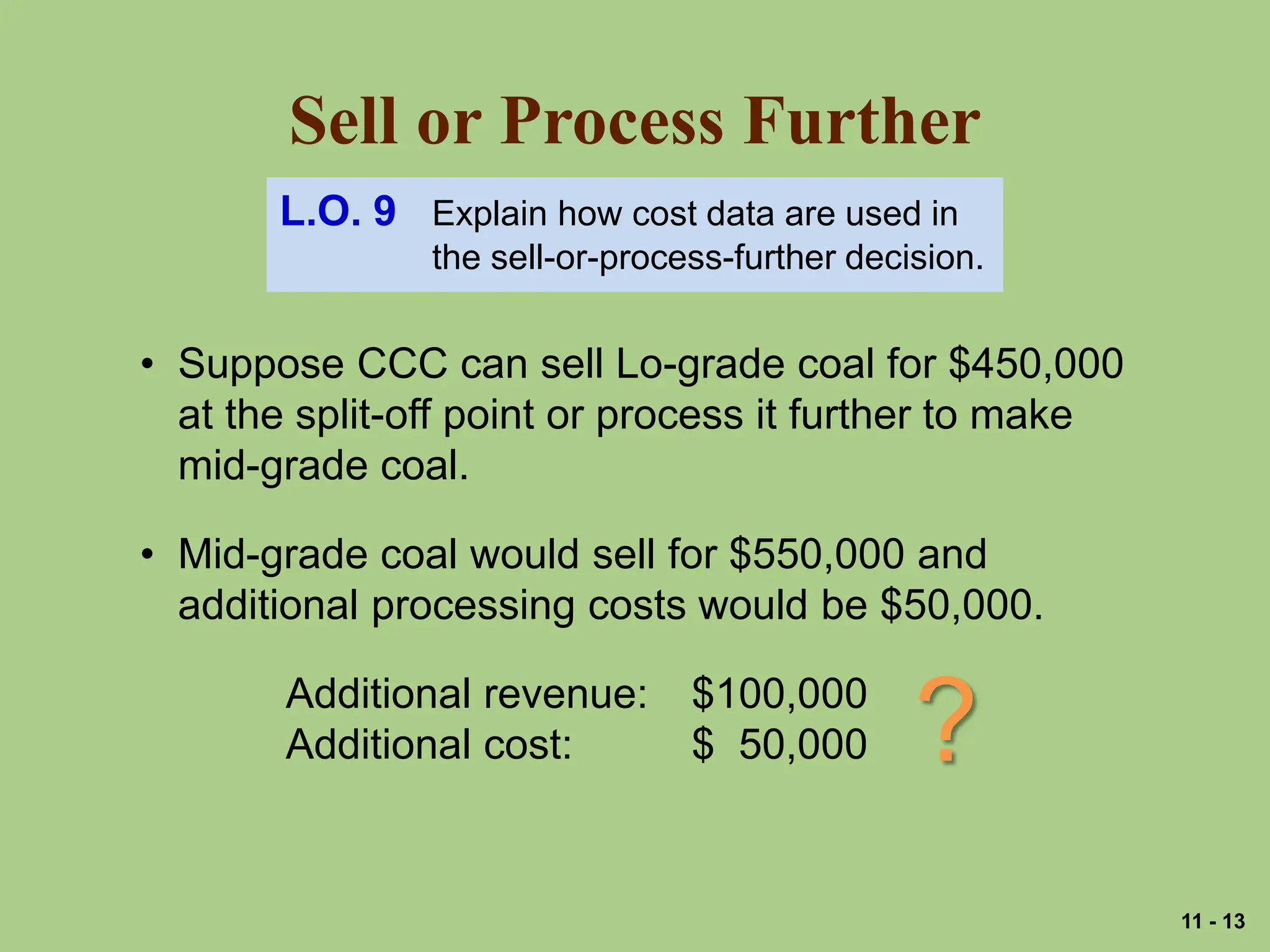

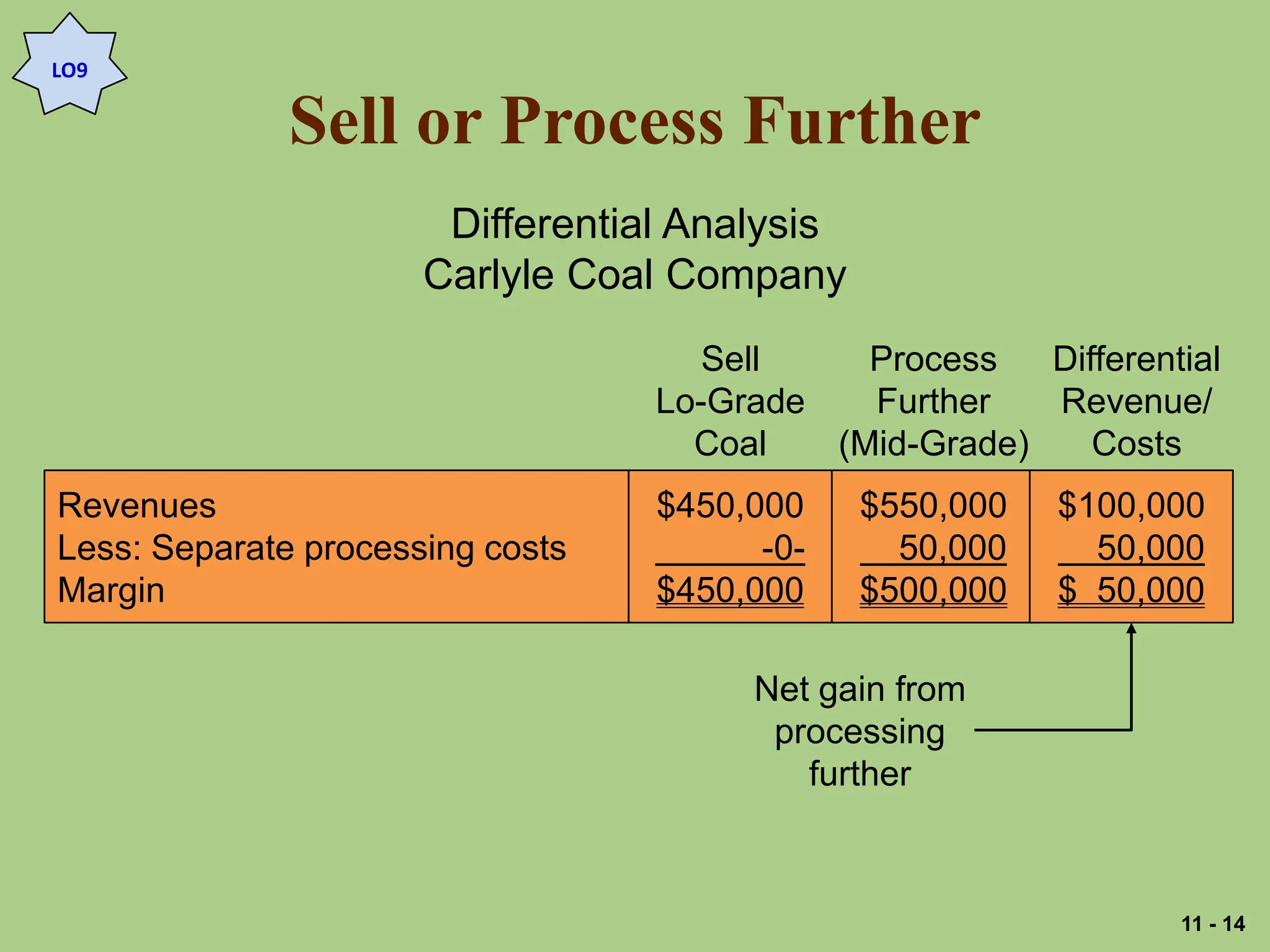

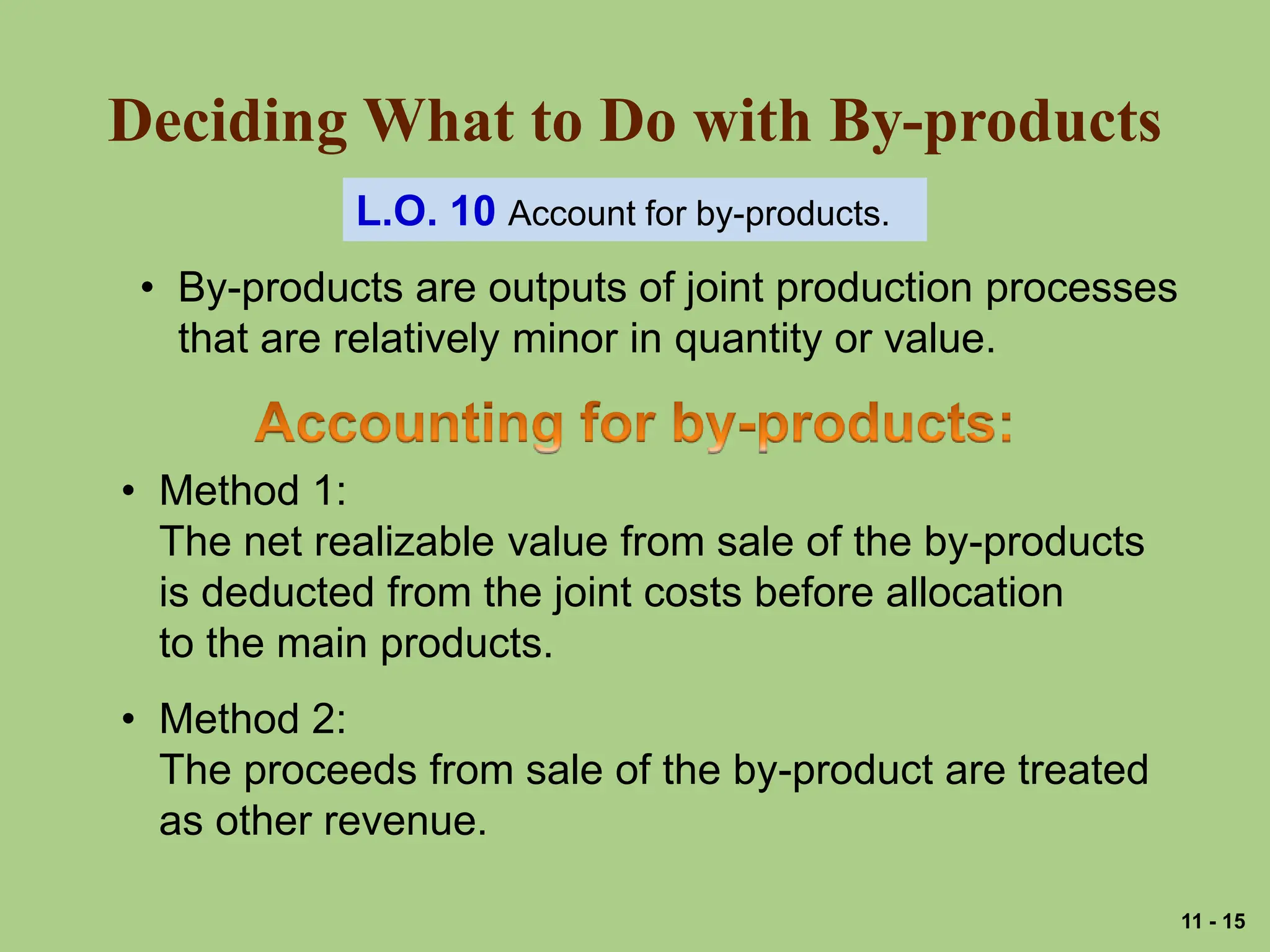

The document discusses various methods for allocating costs between service and production departments, including direct, step, and reciprocal methods. It also covers allocating joint costs using the net realizable value and physical quantities methods, and how cost data is used to determine whether to sell a joint product or process it further. By-products are accounted for by either deducting their net realizable value from joint costs or treating proceeds as other revenue. Spreadsheets can be used to solve reciprocal cost allocation problems through simultaneous equations.