Downloaded 149 times

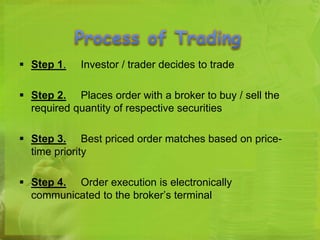

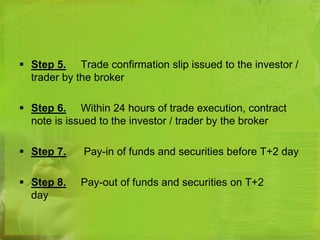

The document discusses the secondary market, where securities are traded after being initially offered to the public in the primary market. In the secondary market, investors can trade existing securities, like stocks and bonds, among themselves through a stock exchange. The secondary market provides liquidity to investors and facilitates price discovery of securities. Some key participants in the secondary market include stockbrokers, clearing corporations, and depositories.