Download to read offline

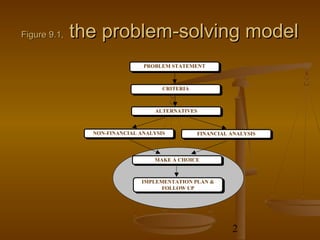

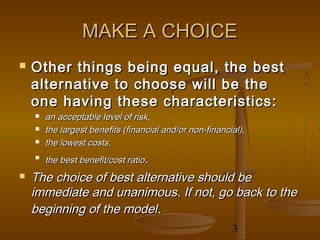

The document discusses how to present a business case and make choices. It outlines a problem-solving model that involves defining the problem and criteria, evaluating alternatives through non-financial and financial analysis, making a choice, and implementing a plan with follow up. The document provides guidance on evaluating alternatives both financially and non-financially. It emphasizes the importance of planning implementation, controlling results through variance analysis, and effectively presenting the business case.

![MindMap - Developing a Business Case [Please Download for better view]](https://cdn.slidesharecdn.com/ss_thumbnails/developingabusinesscase-131126105037-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)