Download as PDF, PPTX

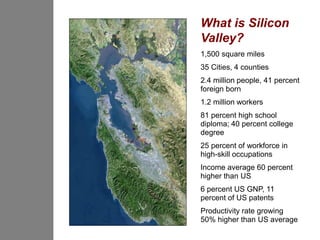

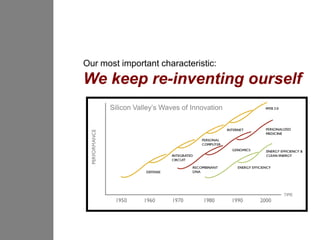

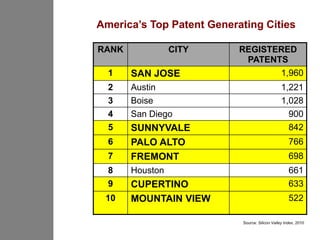

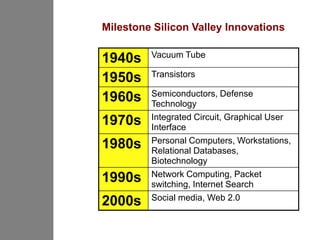

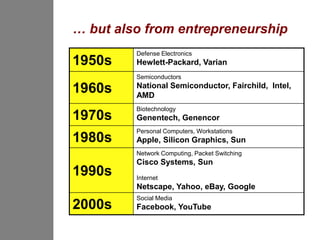

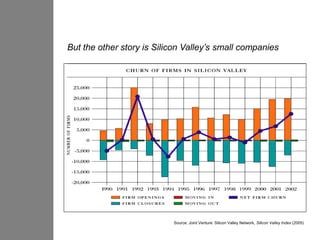

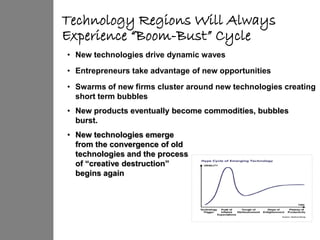

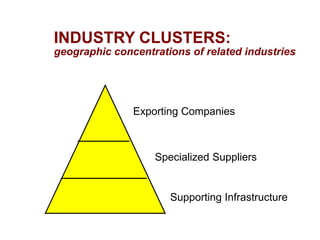

Silicon Valley is a 1,500 square mile region encompassing 35 cities and 4 counties that is home to over 2.4 million people and 1.2 million workers. It has historically been a hotbed of innovation and entrepreneurship, generating waves of new technologies and industries since the 1940s and responsible for 6% of the US GDP and 11% of US patents. However, Silicon Valley's success is not due to innovation alone, but also a culture of entrepreneurship and a cluster effect where related industries, suppliers, and infrastructure coalesce to support new technologies. While bubbles and downturns are inevitable, Silicon Valley has proven resilient by continually reinventing itself with new innovations. It is now building new clusters in renewable energy