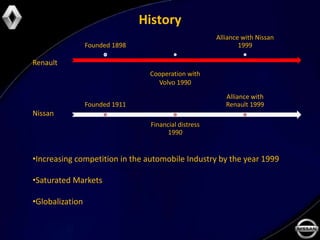

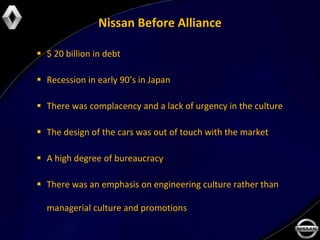

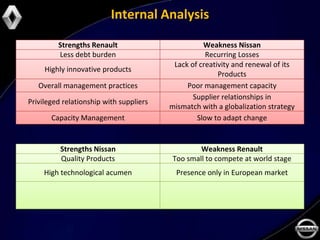

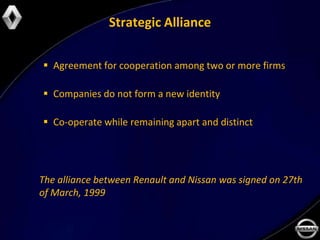

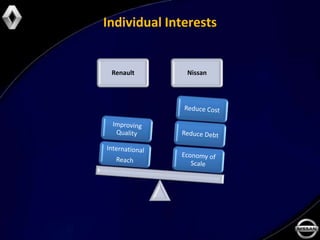

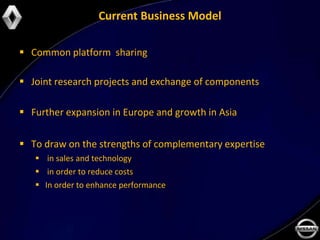

The document summarizes the strategic alliance formed in 1999 between Renault and Nissan, who were both facing challenges from increasing global competition and saturated markets. Nissan was $20 billion in debt and had issues with complacency and bureaucracy. Renault lacked international presence and a diverse product line. The alliance aimed to develop synergies while preserving autonomy, improve quality, and benefit from each other's strengths. Key goals achieved included becoming the third largest automaker with a 9% global market share and a significant presence worldwide.