Download to read offline

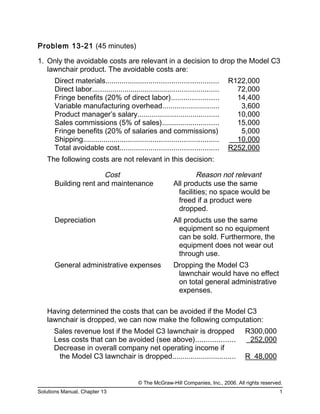

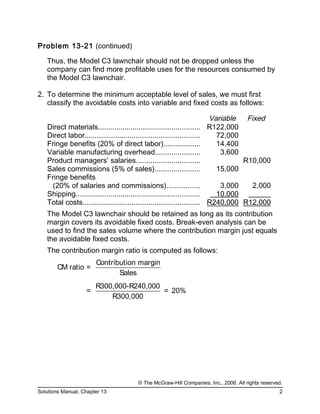

The document discusses financial decision-making regarding the model C3 lawnchair and product profitability in a manufacturing context. It emphasizes the importance of avoidable costs and contribution margins in determining whether to discontinue a product or prioritize production based on constraint resources like welding time. Additionally, it illustrates the impact of direct labor classification as either fixed or variable on overall production decisions and profitability.