Download to read offline

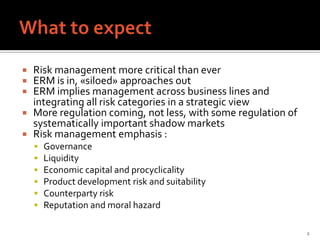

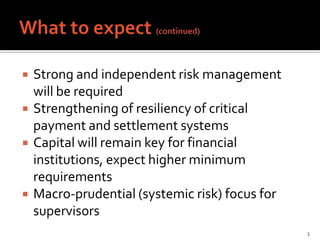

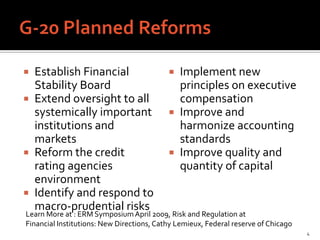

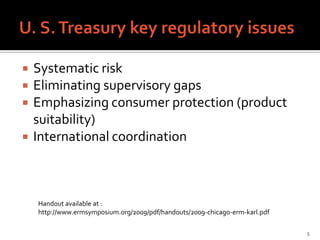

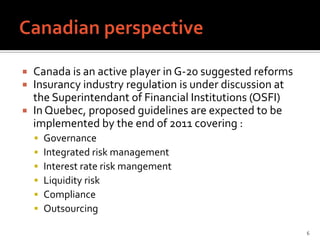

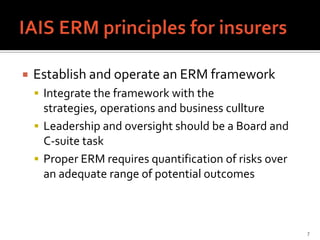

The document summarizes the key points from an RMA Insurance Roundtable discussion on risk management that took place on June 5, 2009 in Mississauga, Ontario. Some of the main topics discussed include: - The increasing importance of enterprise risk management (ERM) and moving away from siloed risk management approaches. - Expectations of increased regulation, particularly around systemic risks. - Key risk management focus areas like governance, liquidity, product development, and counterparty risk. - International regulatory reforms being discussed through organizations like the Financial Stability Board and the need for stronger risk management practices.