Download as PDF, PPTX

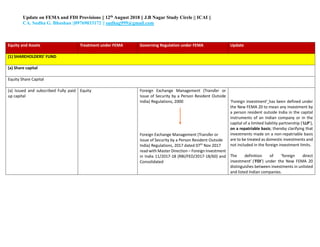

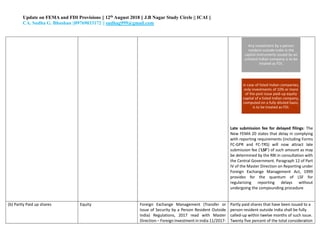

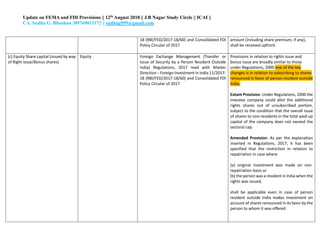

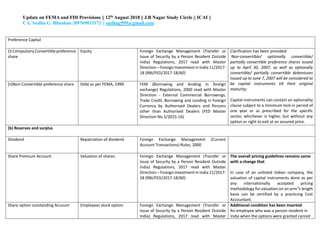

The document provides an update on provisions related to foreign exchange management (FEMA) and foreign direct investment (FDI) in India. Key changes include clarifying that investments made on a non-repatriable basis are treated as domestic rather than foreign investments. For FDI, investments in unlisted companies are treated as FDI, while for listed companies only investments of 10% or more equity are considered FDI. Other updates relate to share issuance timelines, valuation methods, employee stock ownership plans, and external commercial borrowing regulations.