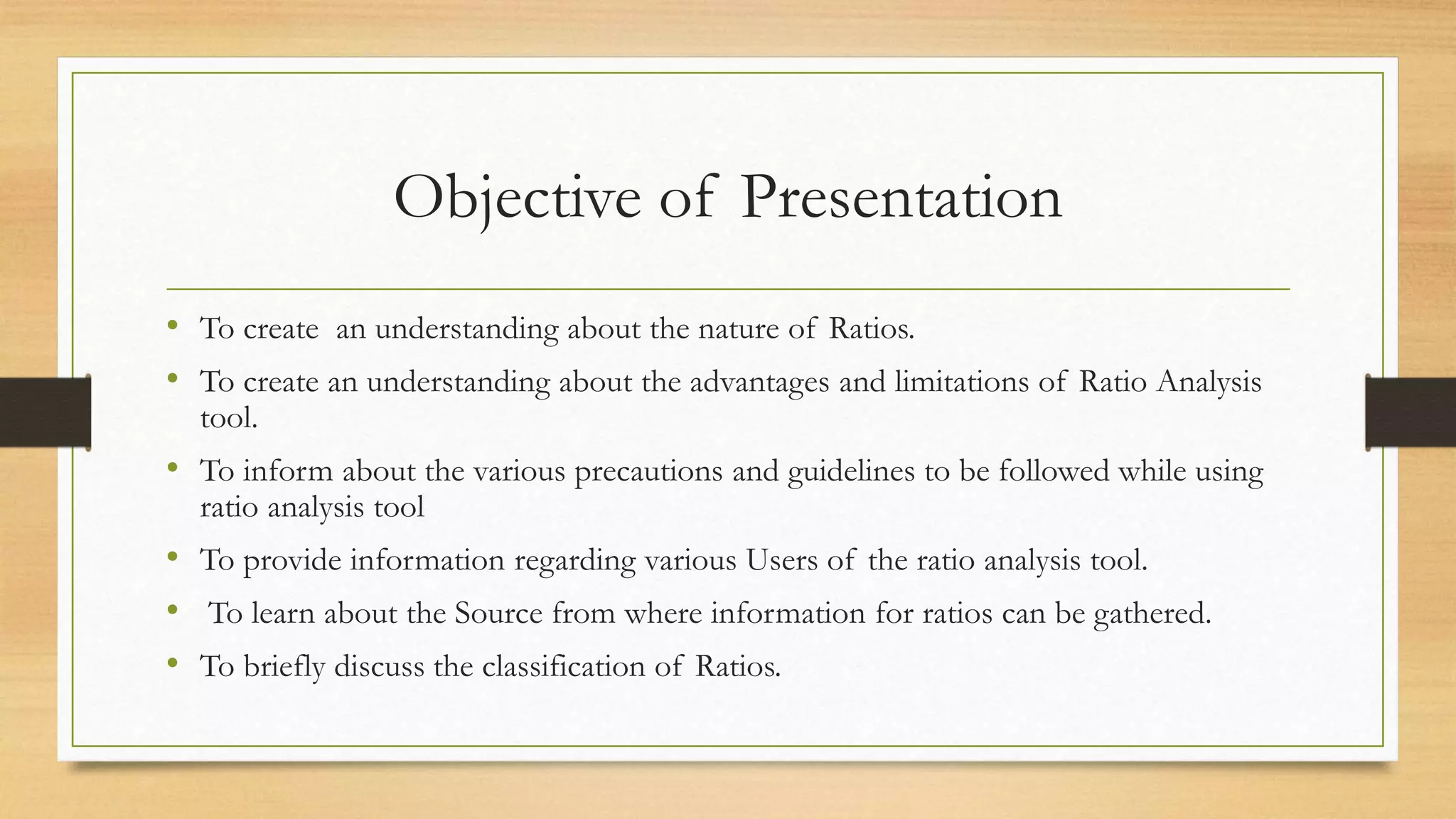

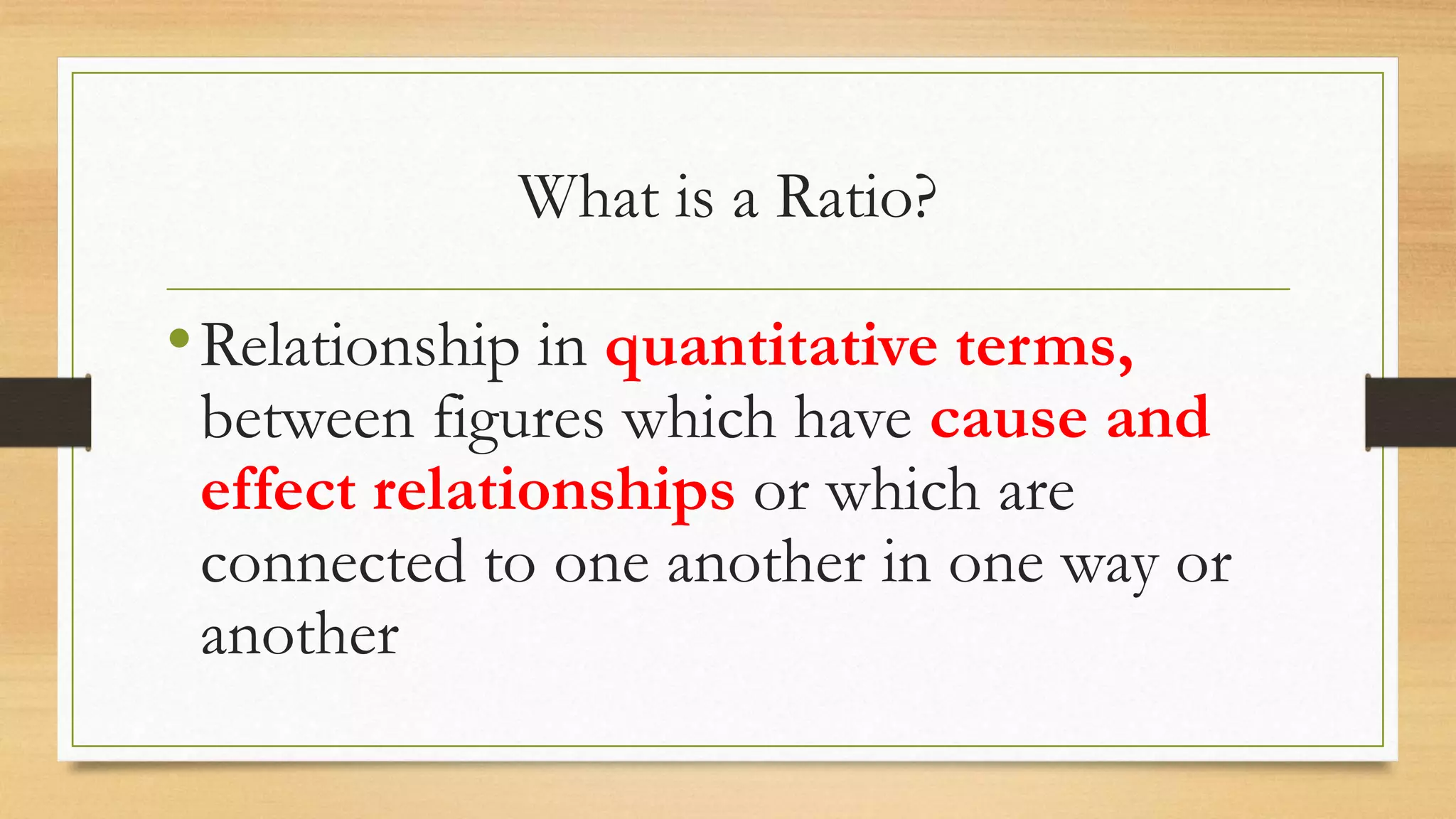

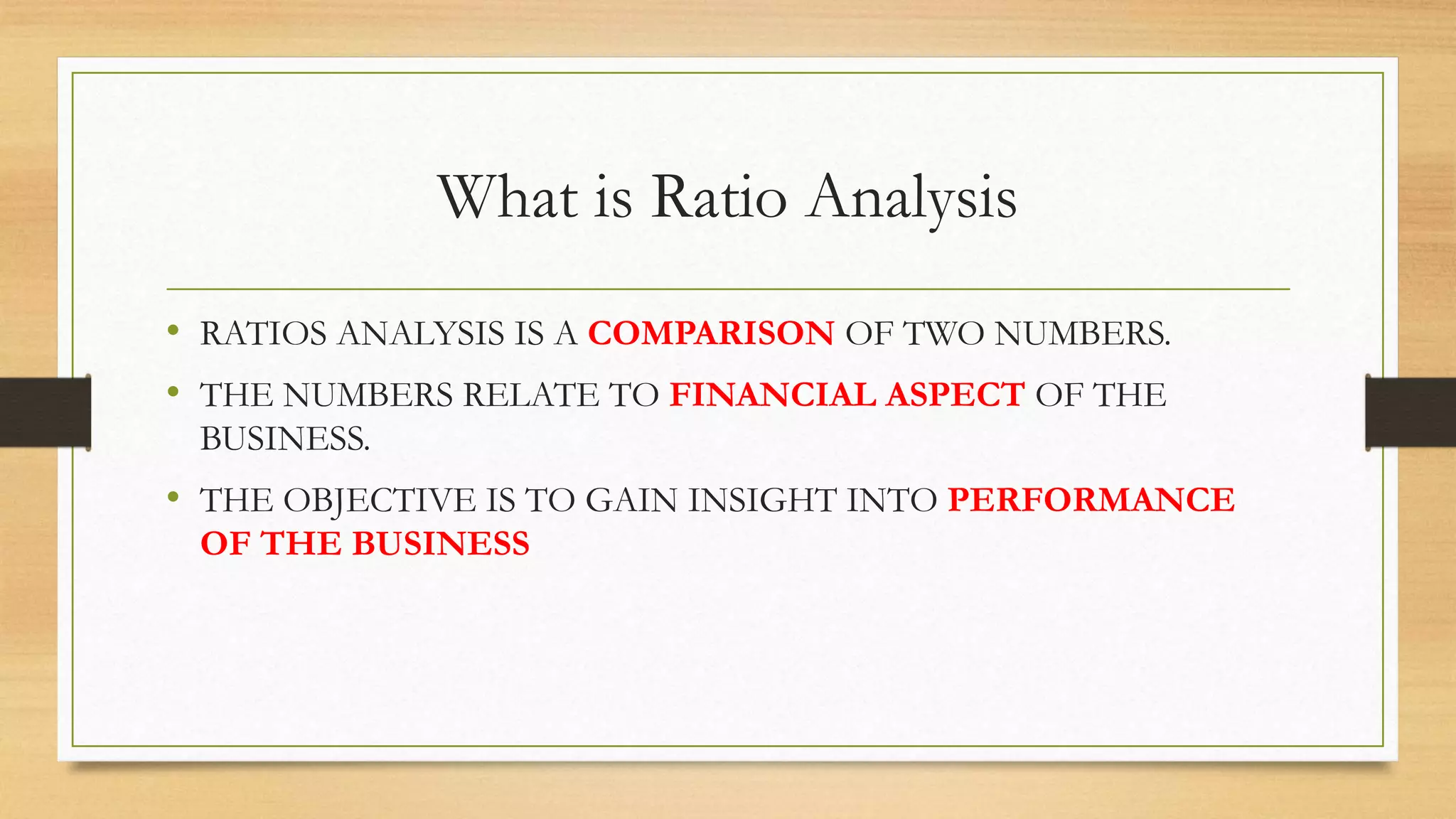

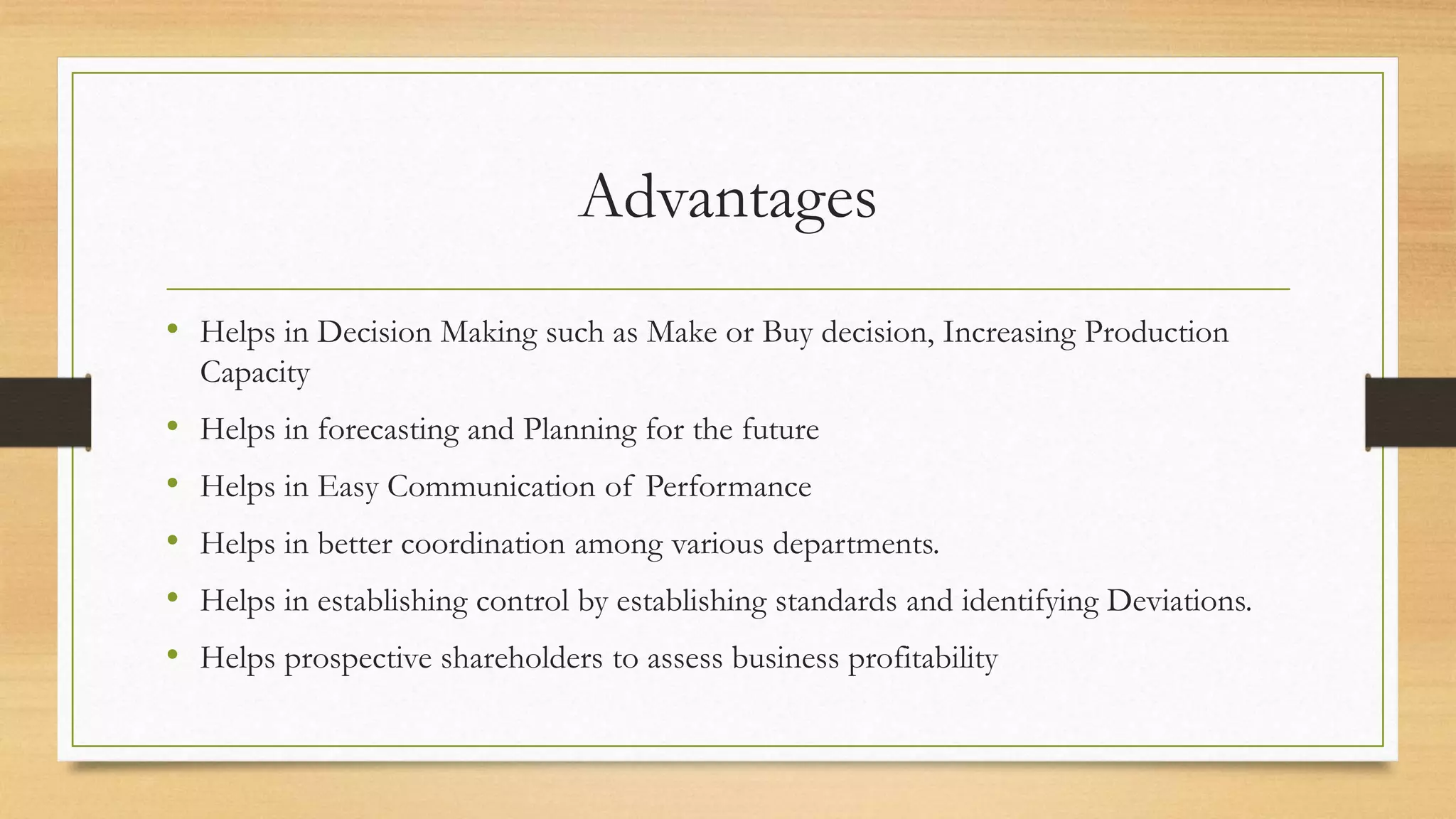

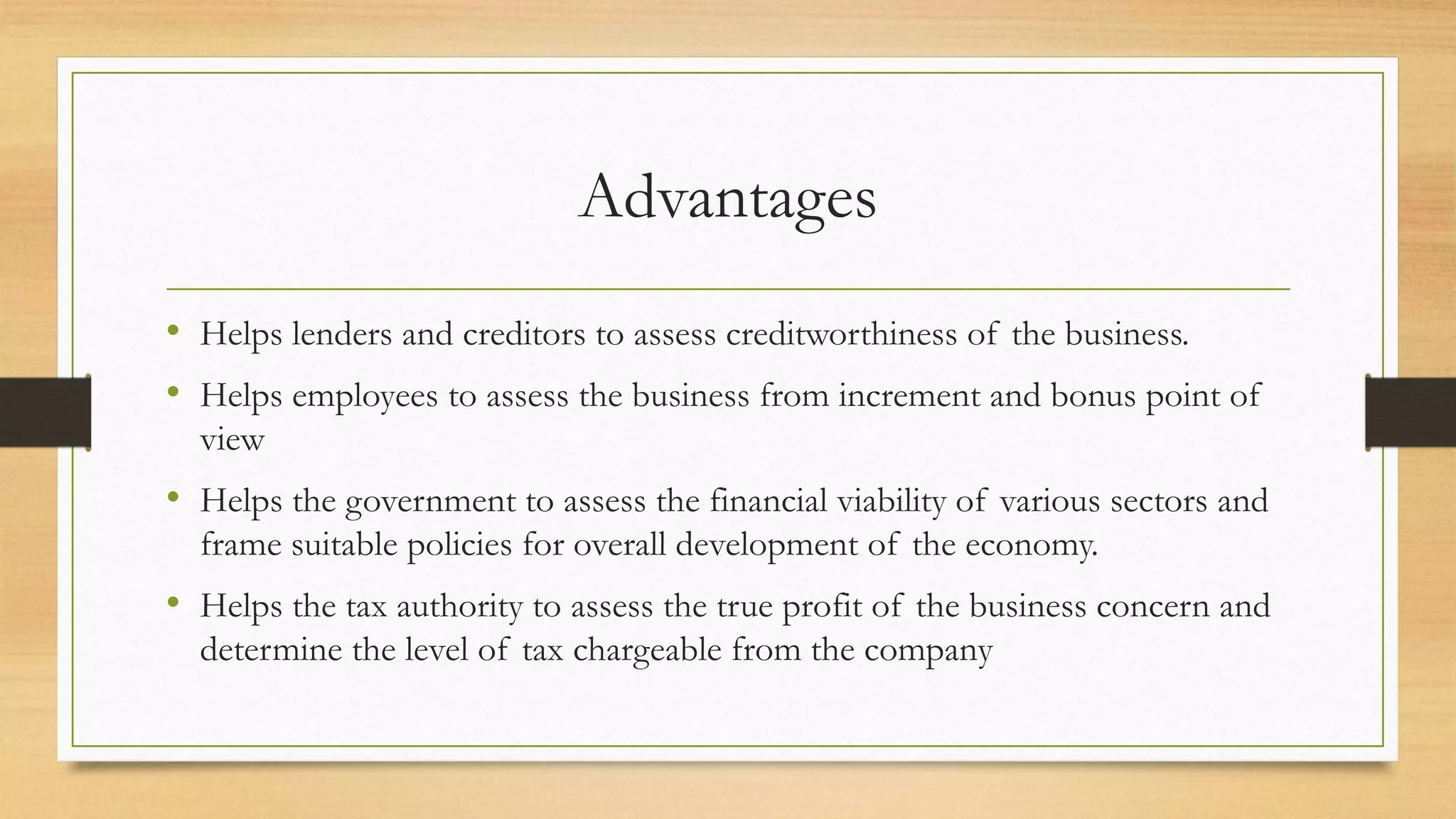

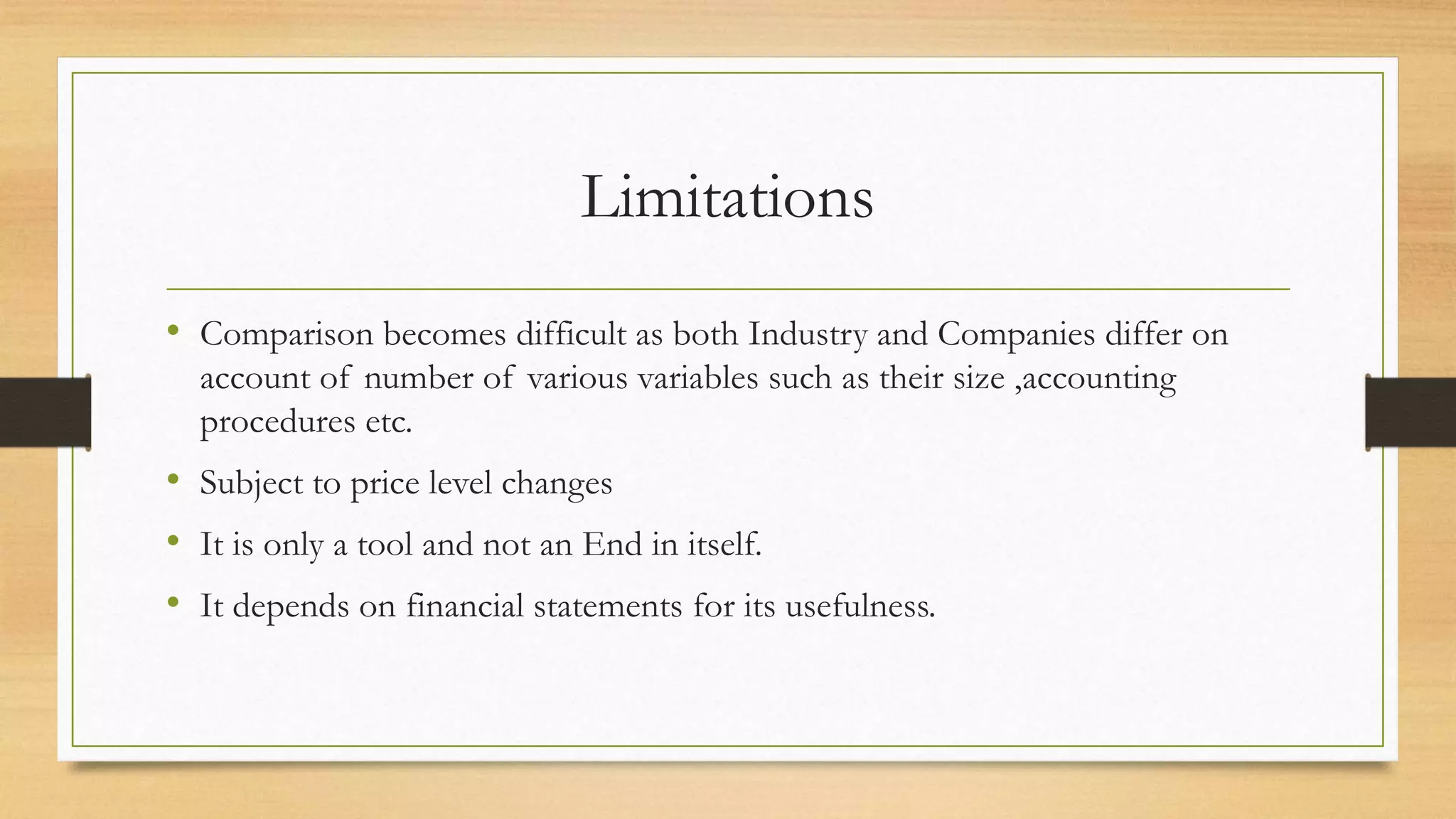

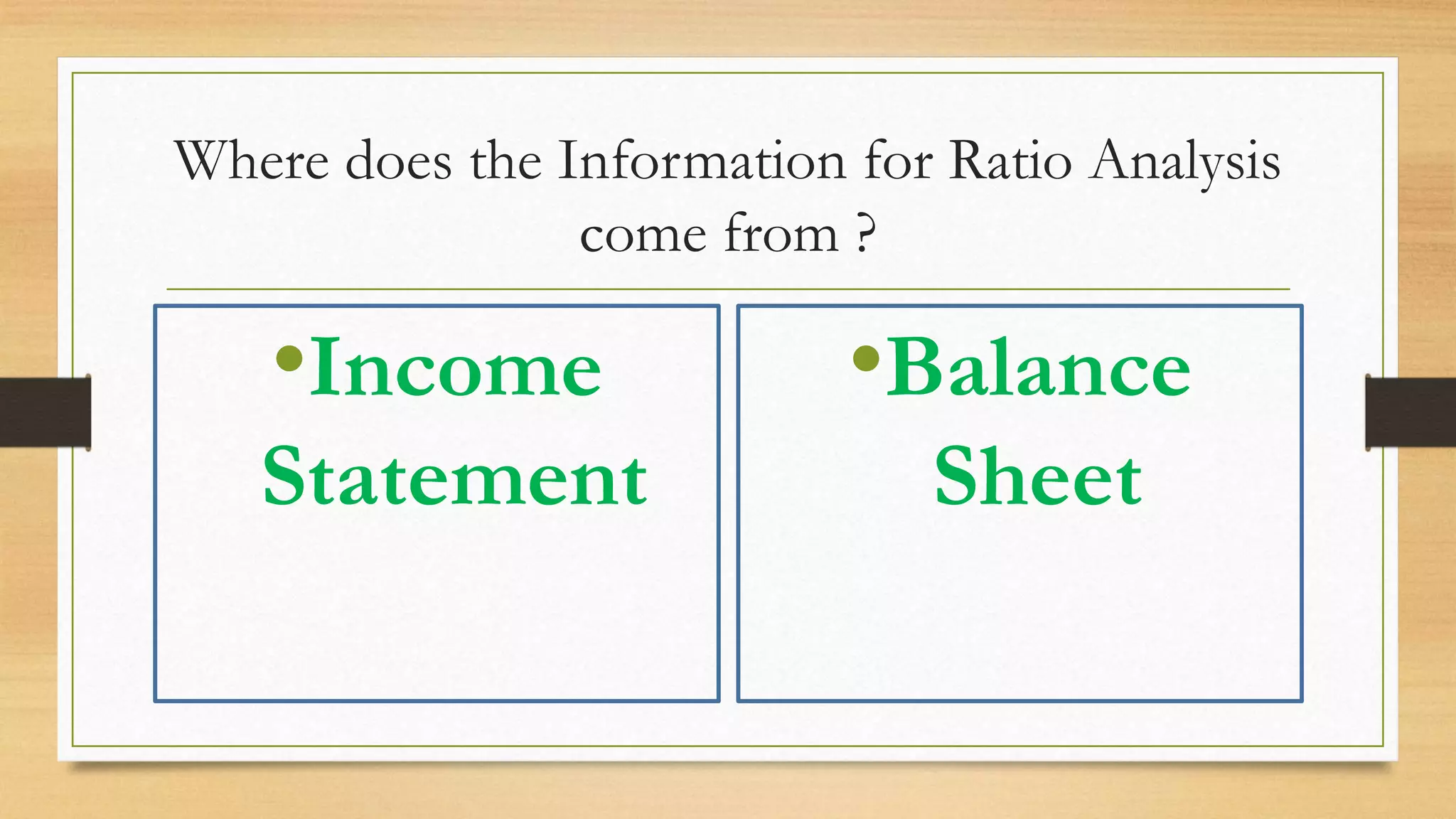

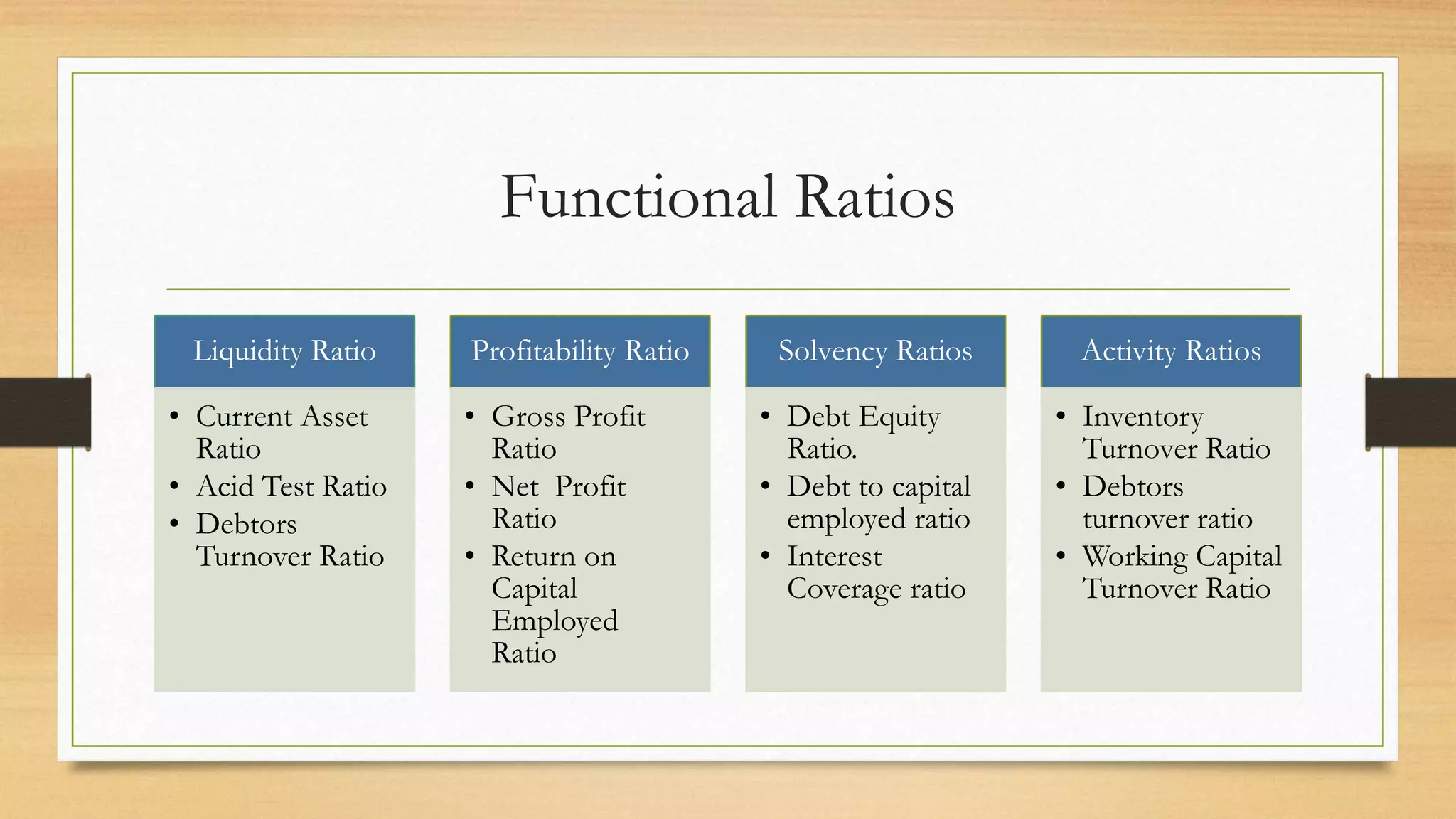

This document presents an overview of ratio analysis, including its definition, advantages, limitations, and users. It emphasizes the importance of understanding ratios for decision-making and highlights various forms and classifications of ratios. The document also addresses the sources of information needed for ratio analysis and provides guidelines for effective use.