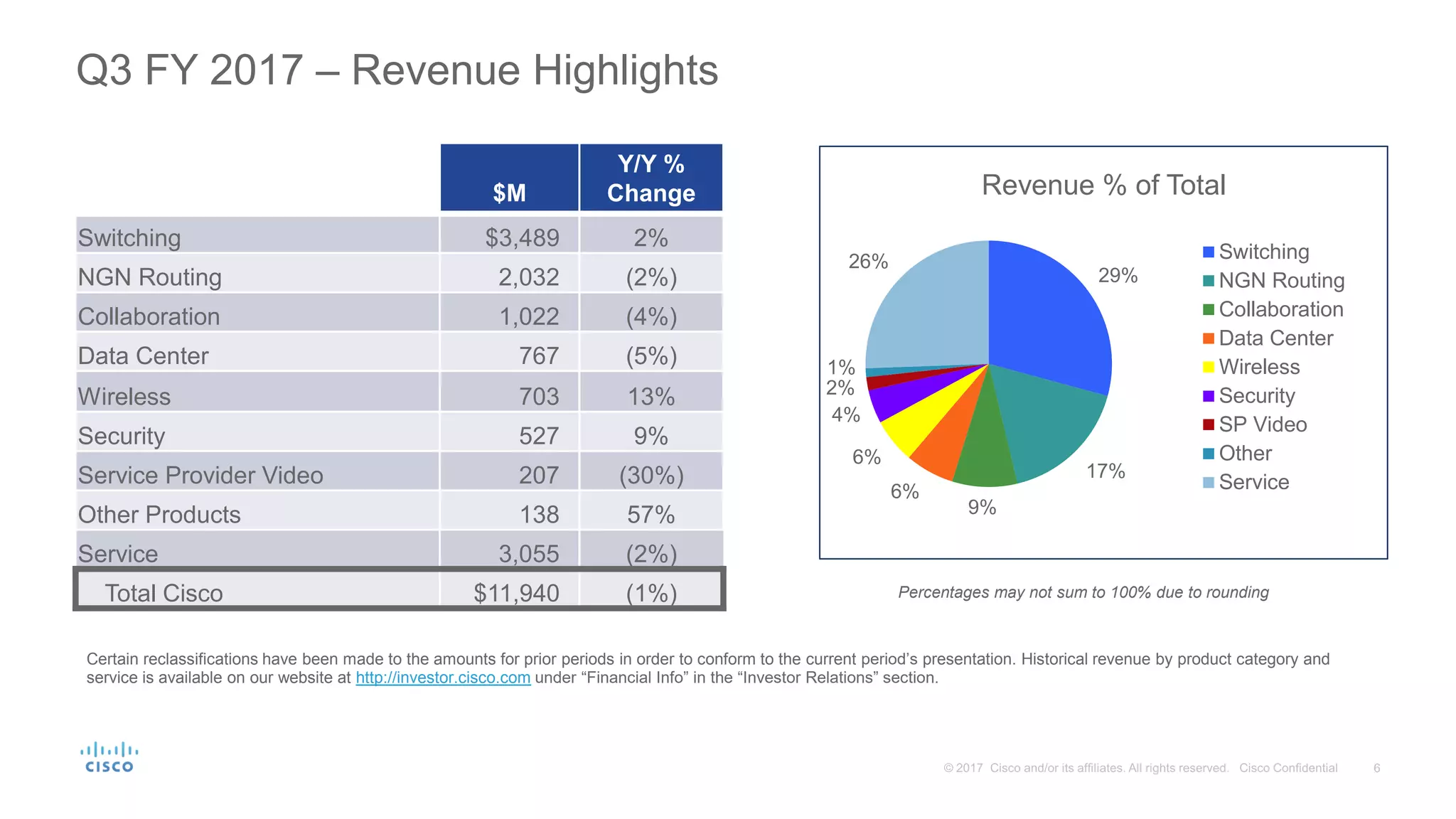

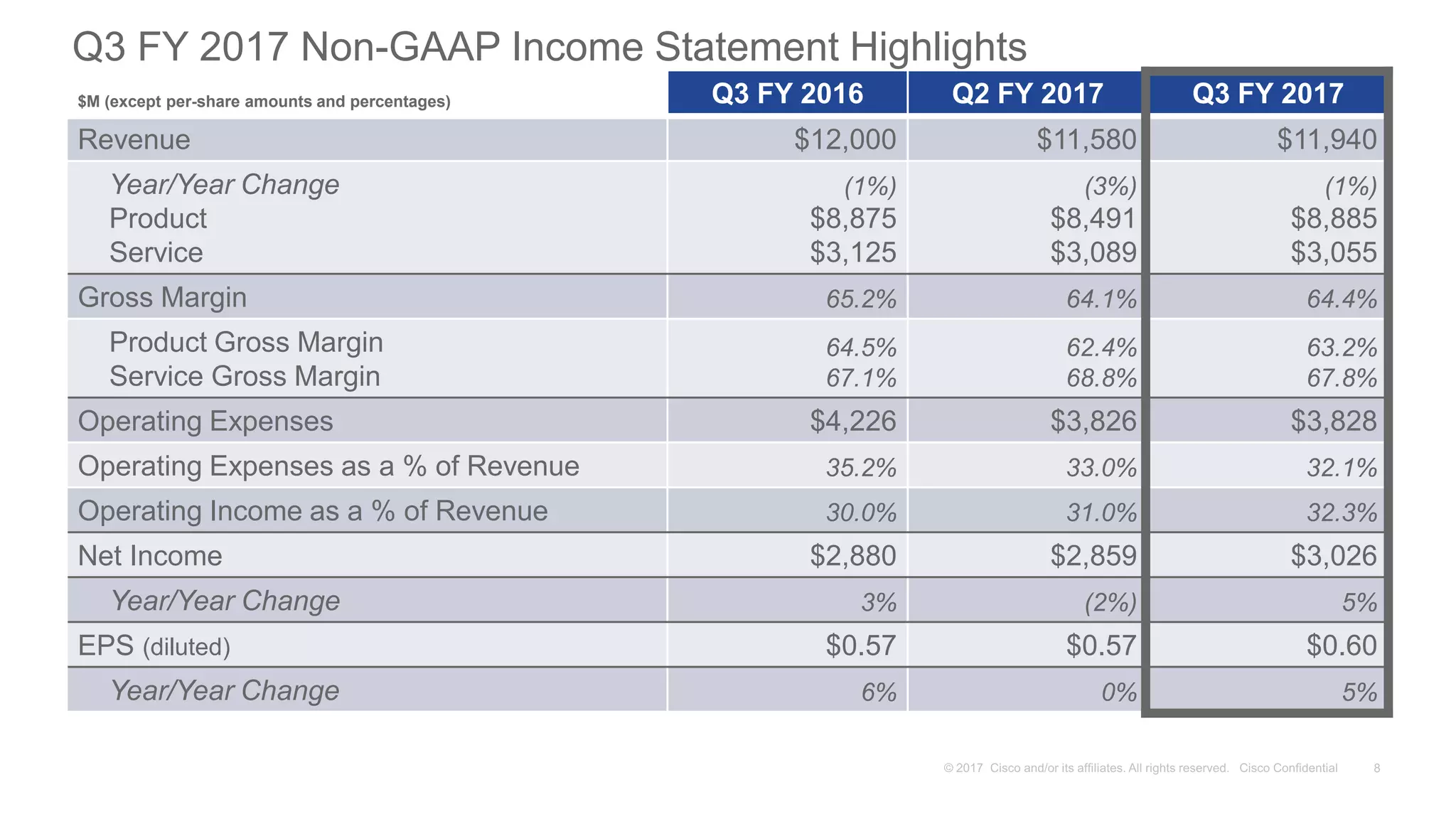

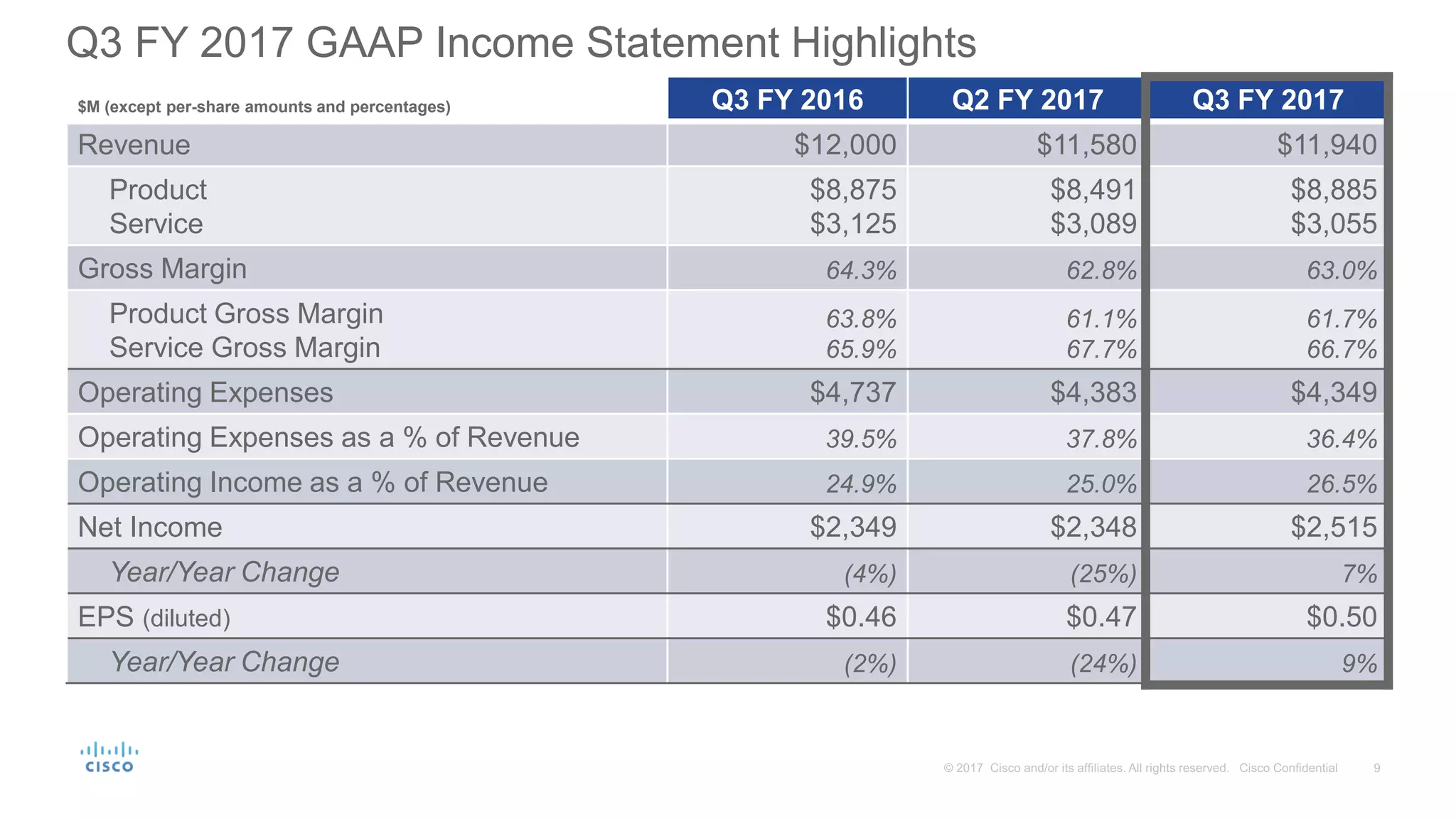

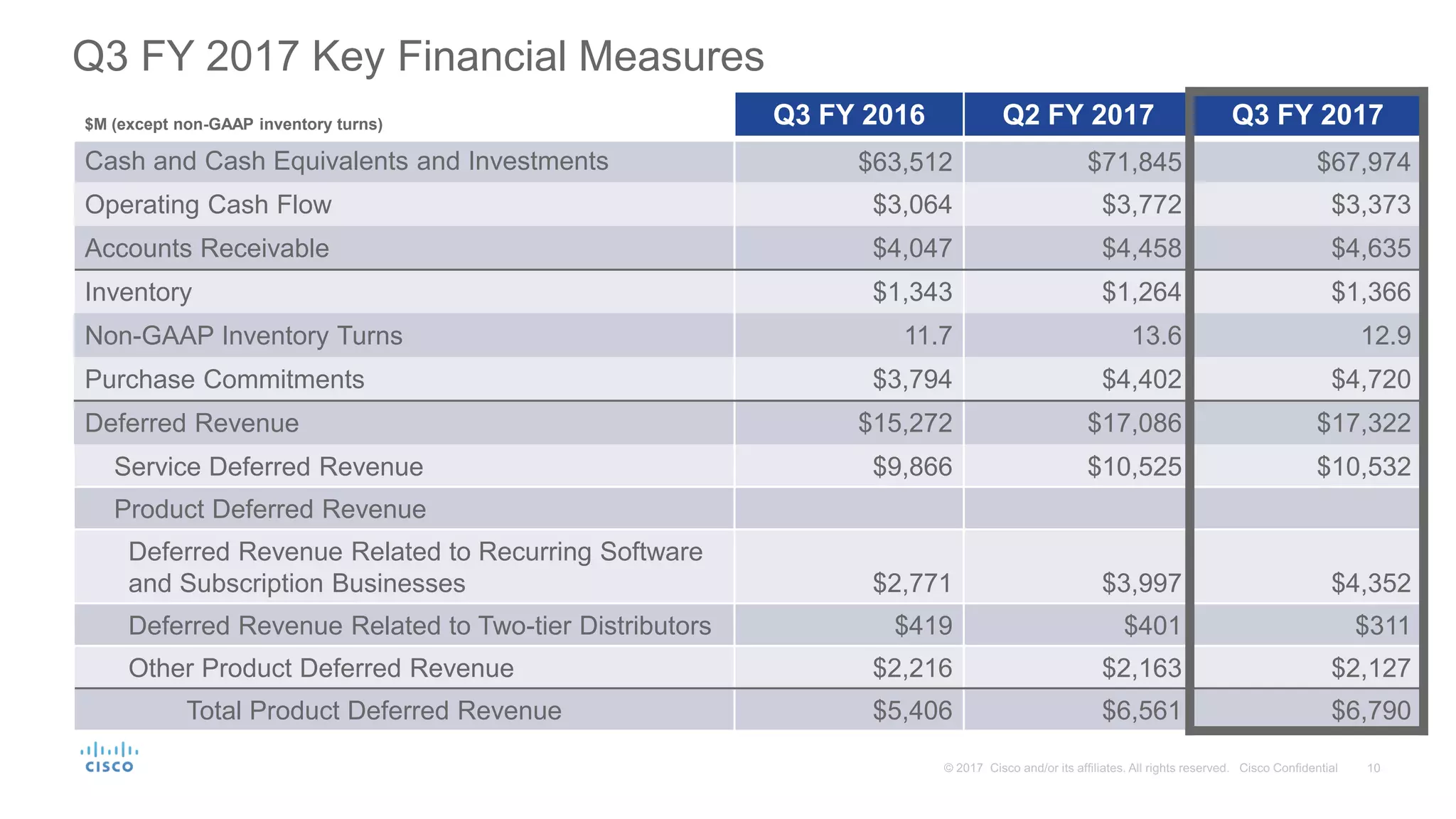

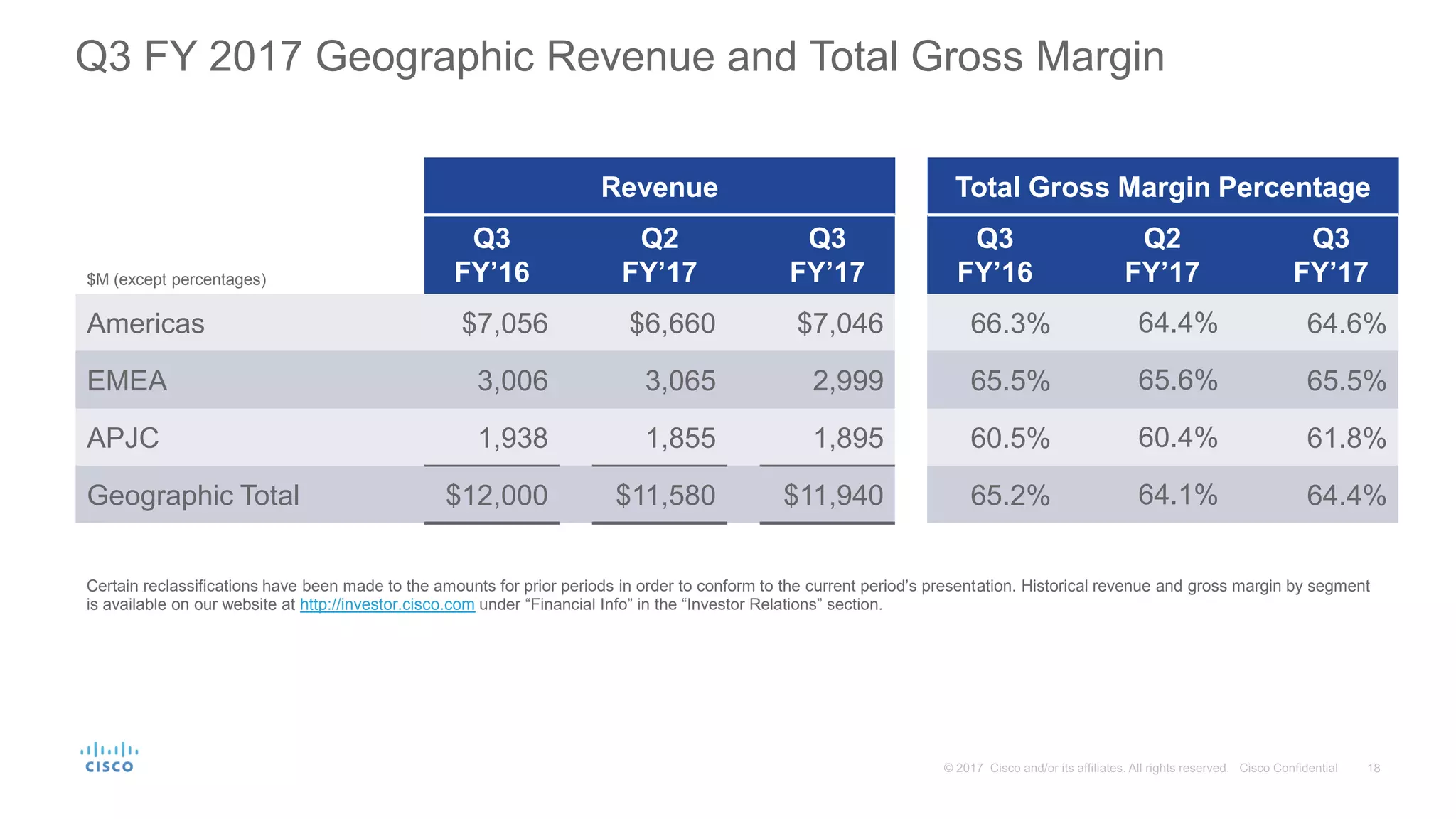

This document provides a summary of Cisco's Q3 Fiscal Year 2017 conference call. The call highlighted Cisco's financial results for Q3 2017, including total revenue of $11.9 billion, down 1% year-over-year, and non-GAAP EPS of $0.60, up 5% year-over-year. Cisco also discussed key business trends, such as its continued transition to more software and subscription revenue through investments in areas like analytics. Finally, Cisco expressed confidence in its strategy for long-term growth and profitability and in continuing to execute well.