Ofcom's review identifies several issues with the current public service broadcasting (PSB) model in the UK and proposes some solutions to prepare PSB for the digital future:

1. The costs of ITV1, ITV Wales, ITV Scotland, and Five will likely exceed the benefits by 2009-2012, making it rational for them to return their licenses.

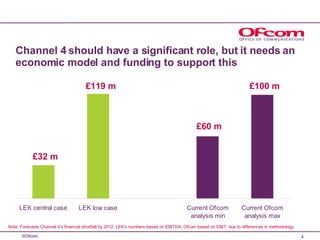

2. Channel 4 will face a significant financial shortfall of £330-420 million per year by 2012 that requires a new economic model and funding solution.

3. Both institutions like the BBC and competitive funding could play important roles in the future by enhancing reach, values, independence, flexibility, and efficiency.

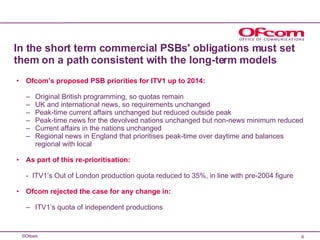

4. In the short term,

![Budapest 2010-psm[1]](https://cdn.slidesharecdn.com/ss_thumbnails/budapest-2010-psm1-100623155927-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Budapest 2010-psm[1]](https://cdn.slidesharecdn.com/ss_thumbnails/budapest-2010-psm1-100623155647-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)