Pricing Strategy for a pharma data analytics company

•

2 likes•306 views

Microeconomics Class Project: Formulated pricing strategy for syndicated subscription data services to biopharmaceutical companies. Recommendations included price differentiation and versioning, pricing based on utility, bundling, two-part tariff, cost reduction strategies.

More Related Content

Similar to Pricing Strategy for a pharma data analytics company

Similar to Pricing Strategy for a pharma data analytics company (20)

Recently uploaded

Recently uploaded (20)

Pricing Strategy for a pharma data analytics company

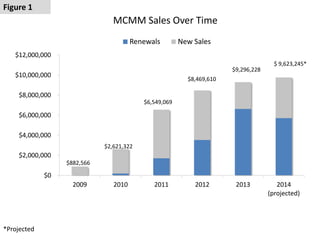

- 1. *Projected MCMM Sales Over Time $0 $2,000,000 $4,000,000 $6,000,000 $8,000,000 $10,000,000 $12,000,000 2009 2010 2011 2012 2013 2014 (projected) Renewals New Sales $882,566 $2,621,322 $6,549,069 $9,296,228 $ 9,623,245* $8,469,610 Figure 1

- 2. 2014 Projected ($) TOTAL SALES 9,623,245 DIRECT EXPENSES Fixed Direct Salaries 777,947 Fixed Consulting/Outside Svcs. 159,264 Fixed Computer Programming 71,743 Fixed Travel and Entertainment 38,402 Variable Honoraria (money paid out for surveys) 1,114,006 Fixed Data 1,191 Total Direct Expense 2,162,552 Contribution Margin 7,786,812 Contribution Margin Percent of Revenue 78% 2014 Profit & Loss Statement 0% 20% 40% 60% 80% 100% Contribution Margin Data Honoraria Travel & Entertainment Computer Programming Consulting Svcs Direct Salaries Figure 2

- 3. MCMM 2014 Pricing by Therapeutic Area $50,000 $100,000 $150,000 $200,000 Level 1 (low volume) Level 2 Level 3 Level 4 Level 5 (high volume) Product Pricing Bands . 7-20 20-35 35-75 >75 Pricing Principles • Syndicated model • Volume-based by disease state • 2nd degree price discrimination: 25% disc for add’l subscriptions • 1st degree price discrimination: small biotechs offered much lower price for slightly less value Assumptions • Monopoly – switching costs, product differentiation, entry barriers/ capital investment • Data volume is a proxy for value ( volume = value = price) Figure 3

- 4. Purchasing Client’s Semi-Annual Message Volume Therapeutic Category’s Semi- Annual Survey Volume A: x < 7 B: 7 ≤ x < 20 C: 20 ≤ x < 35 D: 35 ≤ x < 75 E: 75 ≤ x Level 5 Therapeutic Category 140 ≤ x $124,727 $156,198 $166,968 $182,201 $197,434 Level 4 Therapeutic Category 75 ≤ x < 140 $105,908 $124,727 $140,393 $156,198 $182,201 Level 3 Therapeutic Category 50 ≤ x < 75 $90,675 $98,292 $109,061 $132,483 $156,198 Level 2 Therapeutic Category 30 ≤ x < 50 $67,825 $83,058 $90,675 $101,165 $124,727 Level 1 Therapeutic Category (1 report only) 10 ≤ x < 30 $60,208 $67,825 $75,442 $83,058 $93,256 2014 Prices for a 12-month Subscription, per Therapeutic Area Figure 4

- 5. $0 $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 2009 2010 2011 2012 2013 2014 1 2 3 4 5 Sales by Price Band, Over Time Figure 5

- 6. Utility of a Therapeutic Area for a Pharmaceutical Client Price- utility gap Few drugs in a therapeutic category Many drugs in a therapeutic category Utilityofproducttopharmaclients Time (years) Utility over time, for a therapeutic category Data Volume (and price) Figure 6

- 7. Demand Analysis $100,000 $120,000 $140,000 $160,000 $180,000 $200,000 $220,000 $240,000 0 5 10 15 20 25 Priceperunit Units Demanded Level 5 Pricing - Actual Demand 2009-2014 Figure 7

- 8. Marginal Cost to service an additional client Manager time $2,092.50 Analyst time $2,092.50 $4,185.00 0% 20% 40% 60% Direct Salaries Consulting Svcs Computer Programming Travel & Entertainment Honoraria Data Breakdown of Cost Structure and Contribution Margin 0% 20% 40% 60% 80% 100% Variable Fixed Fixed vs. Variable Costs Figure 8

- 9. Recommendations Increase Demand Reduce Cost Structure Horizontal differentiation • Custom questions value-add • Adjust price based on client reservation price • More data from value survey respondents Decrease payments to low value survey respondents Payments 25% could afford to lose $1.24M sales Bundle with other Zitter products Decrease labor costs by automating data exchange labor ~50% could afford to lose $1.73M sales Two Part Tariff – base subscription for web portal data only, PPT deliverables cost extra; • entry price point will demand Charge price for peak years of utility curve, price when utility is low Figure 9