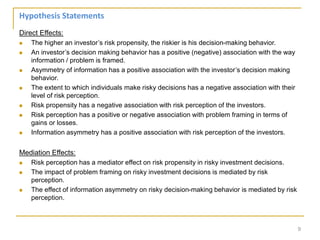

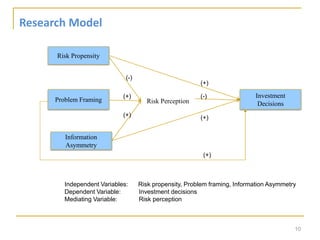

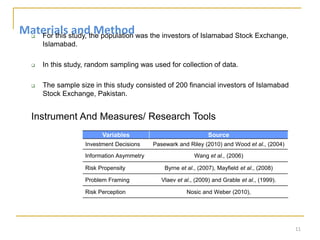

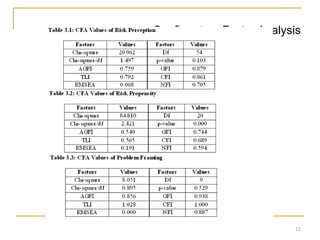

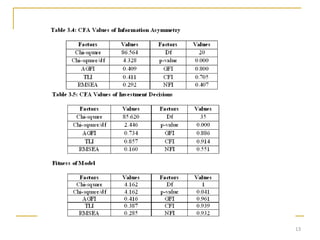

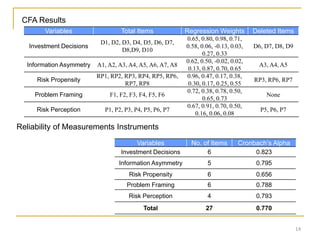

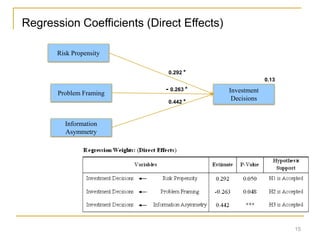

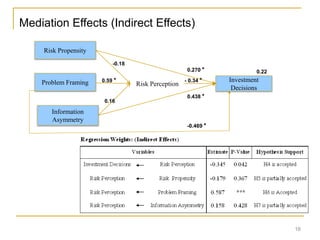

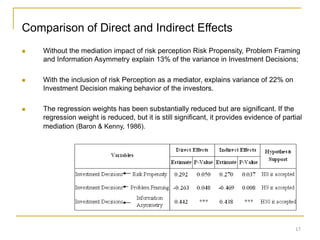

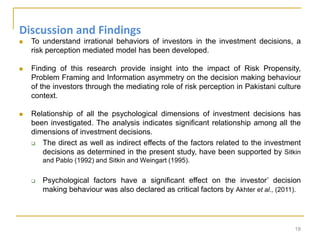

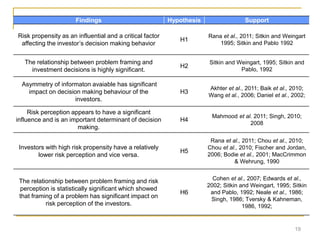

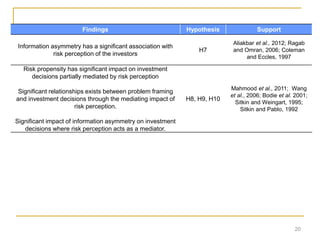

The document discusses a study on the impact of psychological factors on investment decision making. Specifically, it aims to analyze the impact of risk perception as a mediating factor between psychological variables (risk propensity, problem framing, information asymmetry) and investment decisions. The study uses a sample of 200 investors from the Islamabad Stock Exchange. Data is collected through a survey measuring the variables. Confirmatory factor analysis is conducted to validate the survey scales. The study aims to provide insights on how psychological biases influence investment decisions and help investors make more rational choices.

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)