Download to read offline

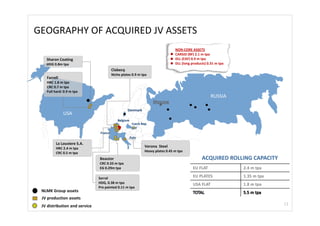

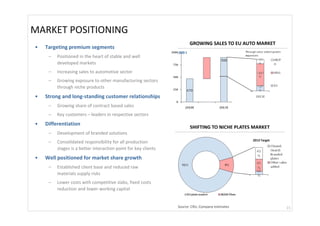

NLMK is acquiring a 50% interest in Steel Invest and Finance (SIF) from Duferco Group for approximately $600 million, which will result in SIF becoming a 100% subsidiary of NLMK and improve NLMK's downstream integration, product mix, geographic diversification, and access to premium markets in Europe and the US through SIF's rolling assets. The transaction is subject to regulatory approvals and is expected to close in the second quarter of 2011.