Download to read offline

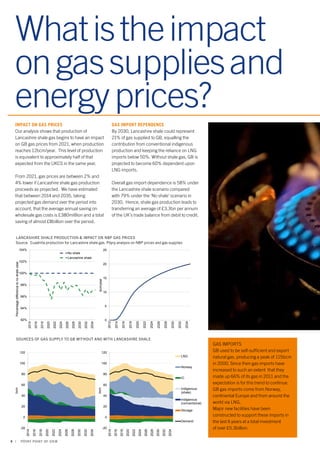

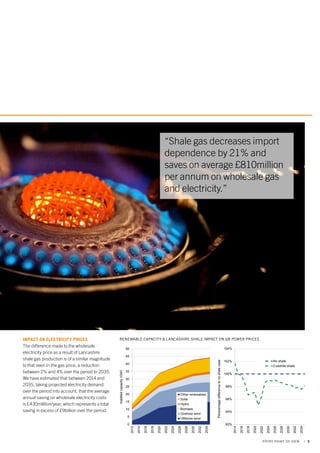

The document explores the potential impacts of Lancashire shale gas production on Great Britain's energy market, highlighting a projected production of 20 bcm/year by 2035 which could lower wholesale gas and electricity prices by 2% to 4%. It suggests that shale gas could reduce GB's import dependence by 21%, saving an average of £3.3 billion annually, while enabling compliance with renewable energy targets. Overall, the study concludes that exploiting Lancashire's shale gas reserves could provide significant economic benefits without compromising environmental goals.