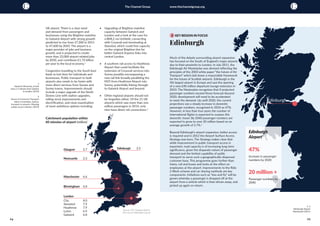

This document discusses the importance of investing in regional infrastructure in the UK to drive economic growth. It argues that the UK needs to invest more in key regional city centers beyond London to create a series of interconnected regional growth hubs. Specifically, it recommends focusing investment on improving road, rail, air and maritime links between major cities like Birmingham, Manchester, Liverpool, Leeds and Newcastle to boost trade, innovation and economic activity in these regions. The document also stresses the importance of improving global air links from regional airports to connect UK businesses to fast-growing international markets in Asia and elsewhere.

![28 29

The Channel Group www.thechannelgroup.org

for businesses to trade. Improving

connectivity between cities will allow

businesses to expand and make

trading more efficient. Similarly in the

southwest with the electrification of

the Great Western Railway travelling

to and from the region will become

easier.

The Brighton mainline needs updating

and the London & South Coast Study,

ordered by the Chancellor George

Osborne in 2015, promised to include

BML2 and is due to be published in

Autumn 2016. ¹

Providing a better rail link to the

underused Stansted airport would

enable Gatwick and Stansted to work

together like a hub airport to increase

international visitors. It will also enable

better cross-London connections

for those living in Kent and Sussex.

Liberal Democrat East Sussex County

Council Councillor Rosalyn St Pierre,

who opposes BML2, acknowledged

that “People in Sussex are forced to

live with one of the worst performing

railway networks in the country”.2

In Cambridgeshire, the small town

of Wisbech hasn’t seen a railway line

in many years, but it has become a

thriving town in recent times. The

process of re-opening railway lines can

take years of consultation and this line,

like the Uckfield to Lewes line in East

Sussex, is no different. The problem is

that Britain has seen a third of its line

capacity, roughly 17,000 miles, shut

down and the process of re-opening

is something Whitehall is reluctant to

consider, not least because it may be

cheaper to add rail capacity through

pharaonic projects such as HS2.

In Scotland, the Edinburgh Glasgow

Improvement Plan (EGIP) is underway.

Scottish Transport Minister Derek

Mackay argued that the Edinburgh

Gateway station will offer “new

journey opportunities to the airport,

places of work and the surrounding

business development area”. A total

of £742 million out of a proposed

£5bn for rail improvement in Scotland

has already been put forward by the

Scottish government. The funding

is being ploughed into an array of

projects, from Edinburgh's Gateway

station and Glasgow’s Queen Street

station, to the line improvements

between Stirling and Dunblane. The

plan is for 150 km of electrified line

in Scotland and a 30% increase in

capacity by 2020, providing faster,

more reliable trains. The programme

faced criticism early on in the process,

with the original estimate being sliced

by £300m and a capacity reduction cut

by 20%. Nevertheless, the programme

is on schedule and will deliver real

change to the aged Scottish network.³

The effect of this regional

infrastructure improvement will

rebalance the scales, shifting the

economic hub away from London

and allow the UK to compete as a

whole on the world stage. Many

historic London-centric businesses,

such as accountancy and law firms,

now have offices in Leeds, Bristol and

Manchester. Cheaper rental space

has taken them there, and the lower

cost to their customers has kept them

there. Employees not living in London

benefit from the lower cost of living.

London cannot be entirely ignored.

It is constantly growing, with the

population expected to reach 10

million by the early 2030s and nearly

11.5 million by 2050.4, 5

Transport

infrastructure in London is already

the most advanced in the country; it

boasts the underground, regular buses,

trains from a multitude of stations, as

well as air travel. All of these modes

of transport are fundamental to daily

life, and the demands placed on them

are vast and varied; from personal

travel to the transportation of goods:

the international to the local. Due to

Newcastle is one of the key

government regional growth areas

and the vision is to have "a transport

system that is an engine for economic

growth”.6

In 2013 the Gateshead and

Newcastle Delivery Plan stretched

to 2030 and aimed to promote and

improve sustainable travel and ensure

effective maintenance of the existing

works. Of key importance is expansion

of the A1, a vital link to Edinburgh

and the South, which faces continual

congestion.7

The National Infrastructure Delivery

plan 2016 - 2021 released in March

2016 contains a £1billion package of

improvement and maintenance works.

Specifically it features the completion

of projects to create a motorway link

from the North East to the rest of

England and start of construction on

both the dualling of the section north

of Newcastle between Morpeth and

Ellingham, and a widening scheme on

the A1 Newcastle-Gateshead Western

Bypass.8

The Port of Tyne has also received

the go ahead for development at a

cost of £350 million which will aim to

provide full time employment to 300

people. The project is located on a 54

hectare brownfield site of which 38.8

hectares is a designated enterprise

zone. Conveniently located only 5

minutes from the metro station with

connectivity to Newcastle airport and

London, the project offers the port

huge support to continue the region's

strong tradition in heavy engineering.9

Newcastle

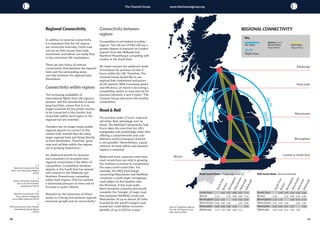

5 KEY REGION IN FOCUS

£350m

Investment in

development of the

Port of Tyne.

£1 billion

Value of

improvement

and maintenance

works outlined

in the National

Infrastructure

Delivery Plan 2016.

the sheer volume of people using the

transport systems in London, they are

often under pressure or operating in

excess of maximum capacity at peak

times. In order to improve, there must

be modernisation and new lines built.

London Bridge station is undergoing a

multi-billion pound overhaul like Kings-

Cross-St Pancras before it. London

Underground is investing millions of

pounds upgrading its network and

purchasing new rolling stock. See 'The

job isn't done in London' overleaf for a

detailed analysis.

“[Poor road and rail infrastructure]

is estimated at costing the Sussex

economy around £2 billion a year.

I am supporting the Brighton Mainline

2 (BML2) campaign which will see the

reopening of the Lewes to Uckfield Rail

line.”

Maria Caulfield, Member of Parliament for Lewes

Speaking to The Channel Group

1

HM Government, Terms of

Reference – London and South

Coast Rail Corridor Study, (2016)

2

Sussex Express, Tories and Lib

Dems clash overprogresstowards

reinstating Lewes-Uckfield

services, (2016)

3

Network Rail, Edinburgh

Glasgow Improvement

Programme, (2016)

4

Mayor of London, London

Infrastructure Plan 2050, (2013)

5

HM Government, National

Infrastructure Delivery Plan

2016–2021, (2016)

6, 7

Gateshead Council, Gateshead

and Newcastle Infrastructure

Delivery Plan, (2013)

8

HM Government Infrastructure

and Projects Authority,

National Infrastructure Delivery

Plan 2016–2021, (2016)

9

HM Government Regeneration

Investment Organisation,

Regeneration Project: Port of

Tyne – Newcastle / Tyne and

Wear, (2015)](https://image.slidesharecdn.com/654ea8a7-0daa-4886-8b73-96c0f915b7a8-160524182234/85/Powering-Up-The-Engines-15-320.jpg)