Download as PDF, PPTX

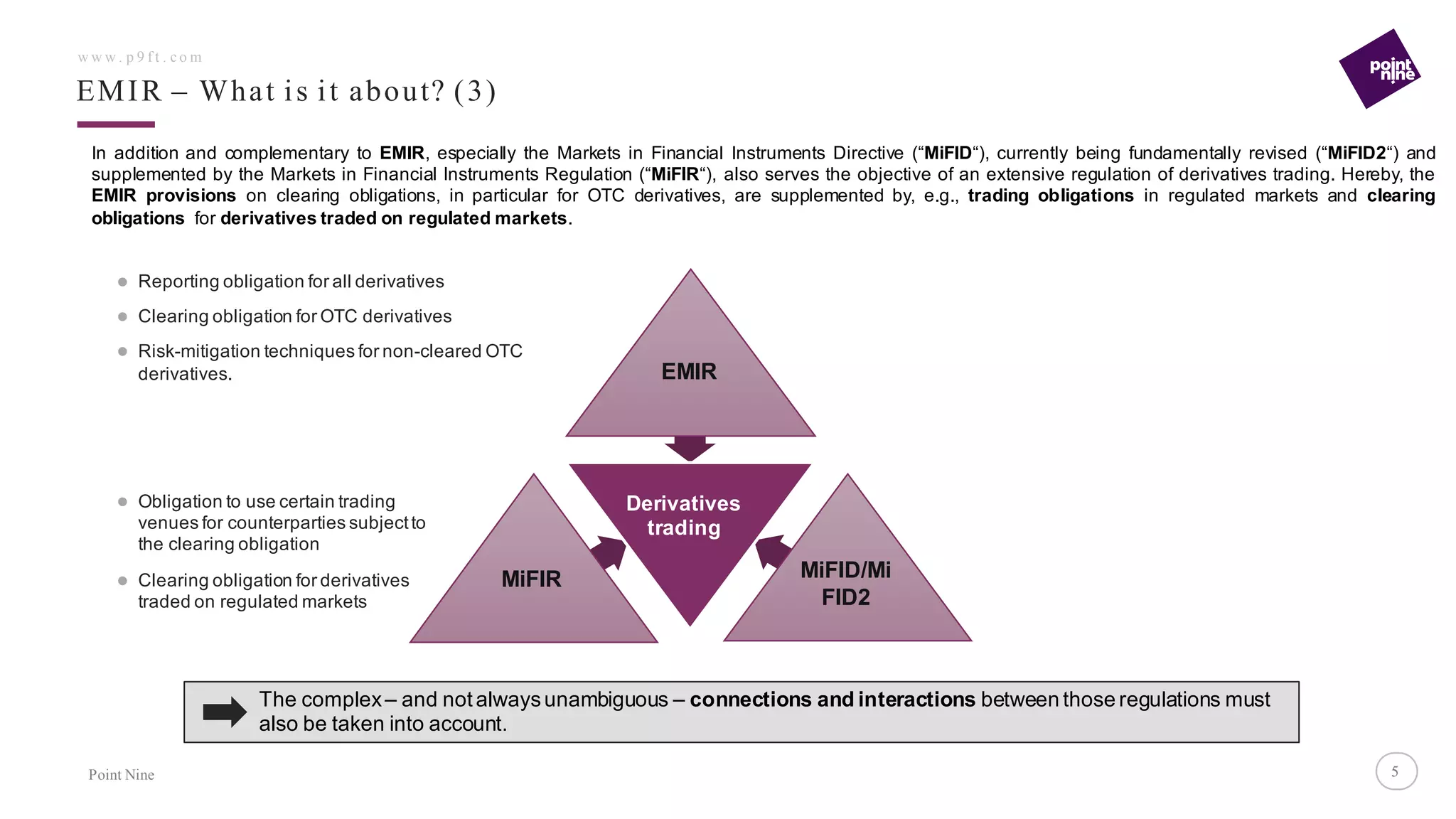

The document discusses the European Market Infrastructure Regulation (EMIR) which aims to reduce risks in over-the-counter (OTC) derivatives markets through increased transparency, security and regulation. EMIR requires reporting of all derivatives contracts to trade repositories, clearing of standardized OTC contracts through central counterparties, and risk mitigation processes for non-cleared OTC derivatives. It affects financial and non-financial counterparties engaged in derivatives trading and imposes requirements for reporting, clearing thresholds, and compliance audits.