Download as PDF, PPTX

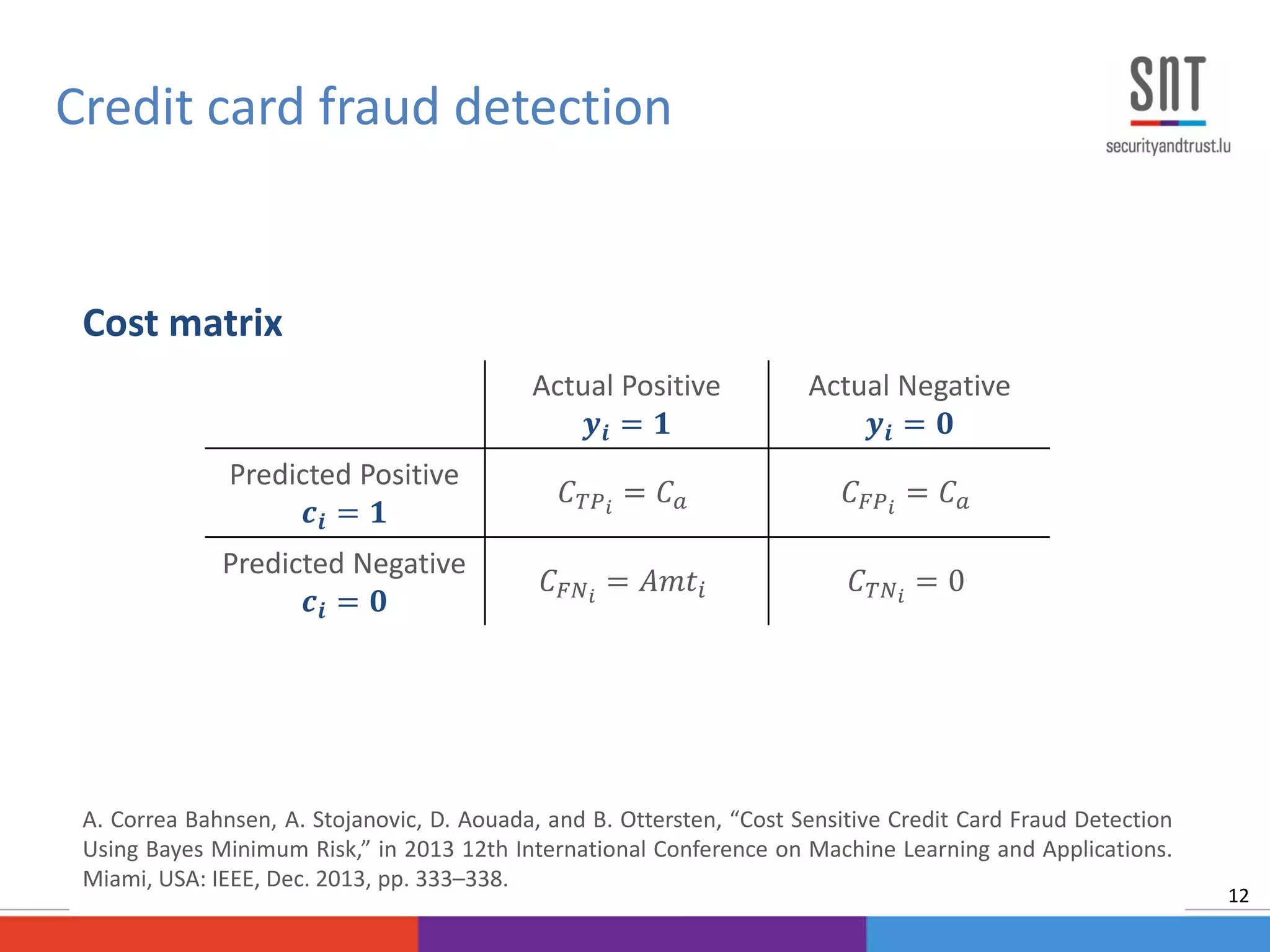

![We define a cost measure based on the cost matrix [Elkan 2001]

From which we calculate the 𝑪𝒐𝒔𝒕 of applying a classifier to a given set

𝐶𝑜𝑠𝑡 𝑓 𝑆 =

𝑖=1

𝑁

𝑦𝑖 𝑐𝑖 𝐶 𝑇𝑃 𝑖

+ 1 − 𝑐𝑖 𝐶 𝐹𝑁 𝑖

+ 1 − 𝑦𝑖 𝑐𝑖 𝐶 𝐹𝑃 𝑖

+ 1 − 𝑐𝑖 𝐶 𝑇𝑁 𝑖

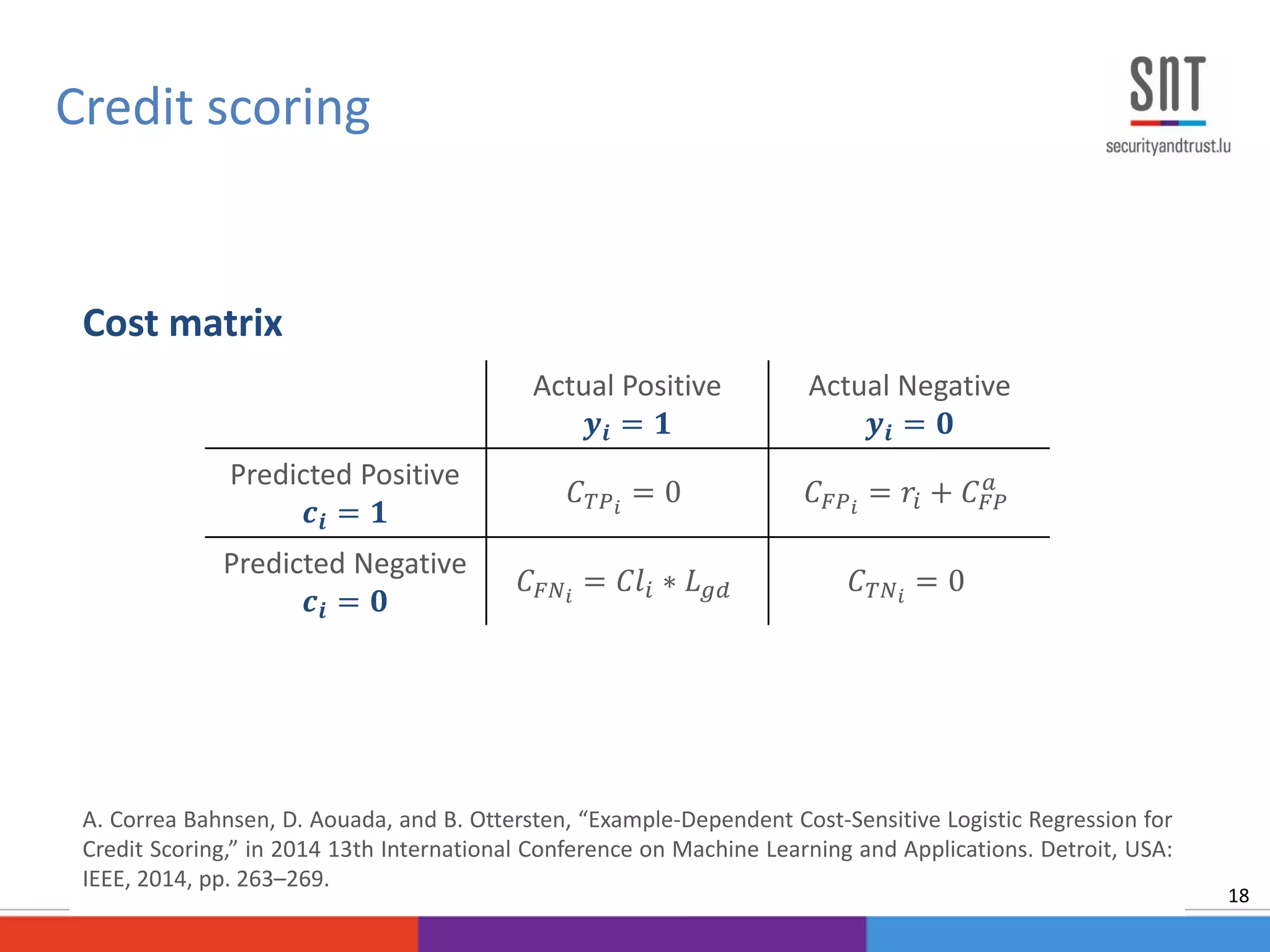

Background - Cost-sensitive evaluation

6

Actual Positive

𝒚𝒊 = 𝟏

Actual Negative

𝒚𝒊 = 𝟎

Predicted Positive

𝒄𝒊 = 𝟏

𝐶 𝑇𝑃 𝑖

𝐶 𝐹𝑃 𝑖

Predicted Negative

𝒄𝒊 = 𝟎

𝐶 𝐹𝑁 𝑖

𝐶 𝑇𝑁 𝑖](https://image.slidesharecdn.com/thesisexampledependentcostsensitiveclassificationslides-150923041551-lva1-app6892/75/PhD-Defense-Example-Dependent-Cost-Sensitive-Classification-6-2048.jpg)

![Research in example-dependent cost-sensitive classification has been

narrow, mostly because of the lack of publicly available datasets [Aodha

and Brostow 2013].

Standard approaches consist in re-weighting the training examples based

on their costs:

• Cost-proportionate rejection sampling [Zadrozny et al. 2003]

• Cost-proportionate oversampling [Elkan 2001]

Background - State-of-the-art methods

8](https://image.slidesharecdn.com/thesisexampledependentcostsensitiveclassificationslides-150923041551-lva1-app6892/75/PhD-Defense-Example-Dependent-Cost-Sensitive-Classification-8-2048.jpg)

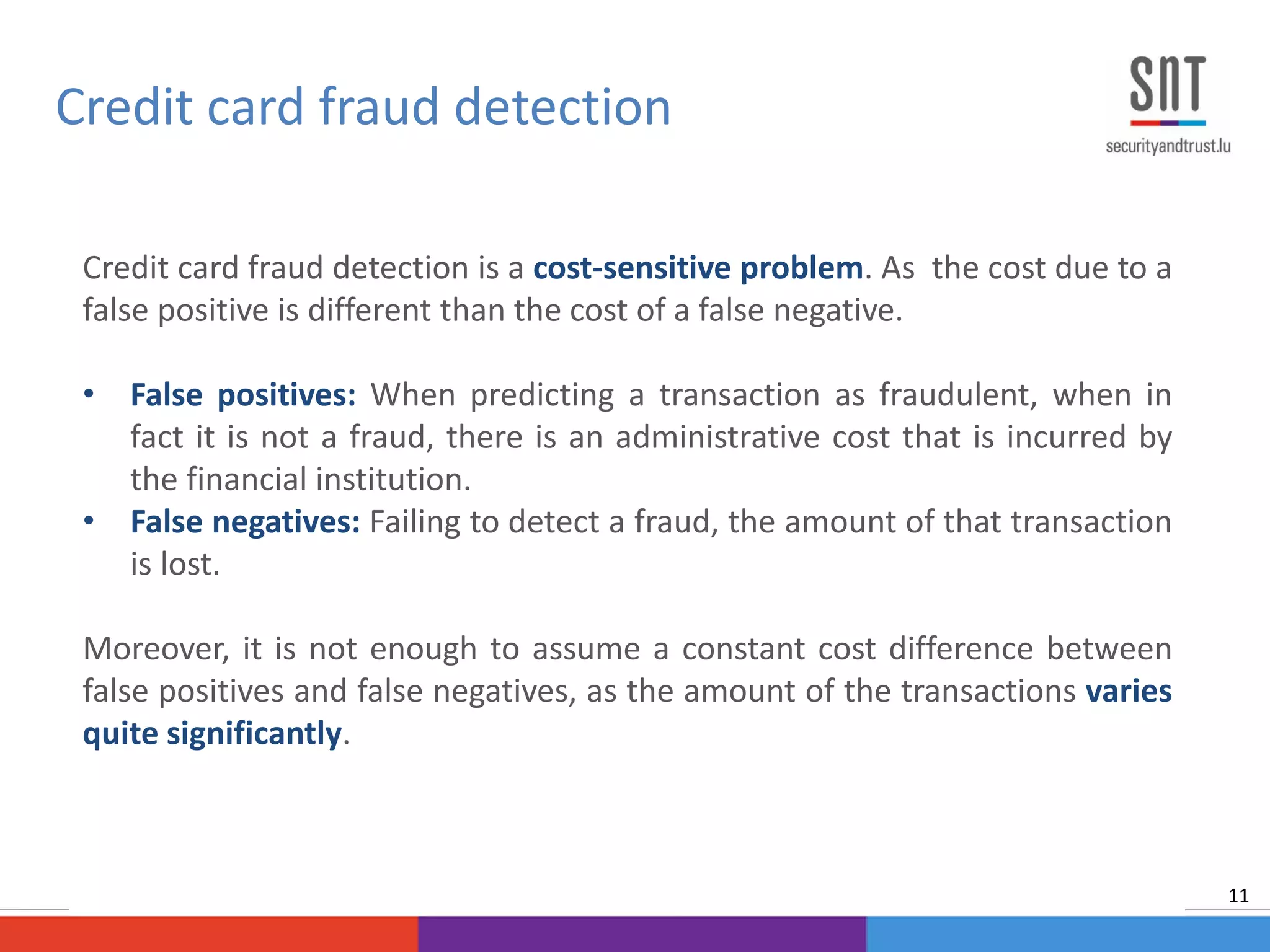

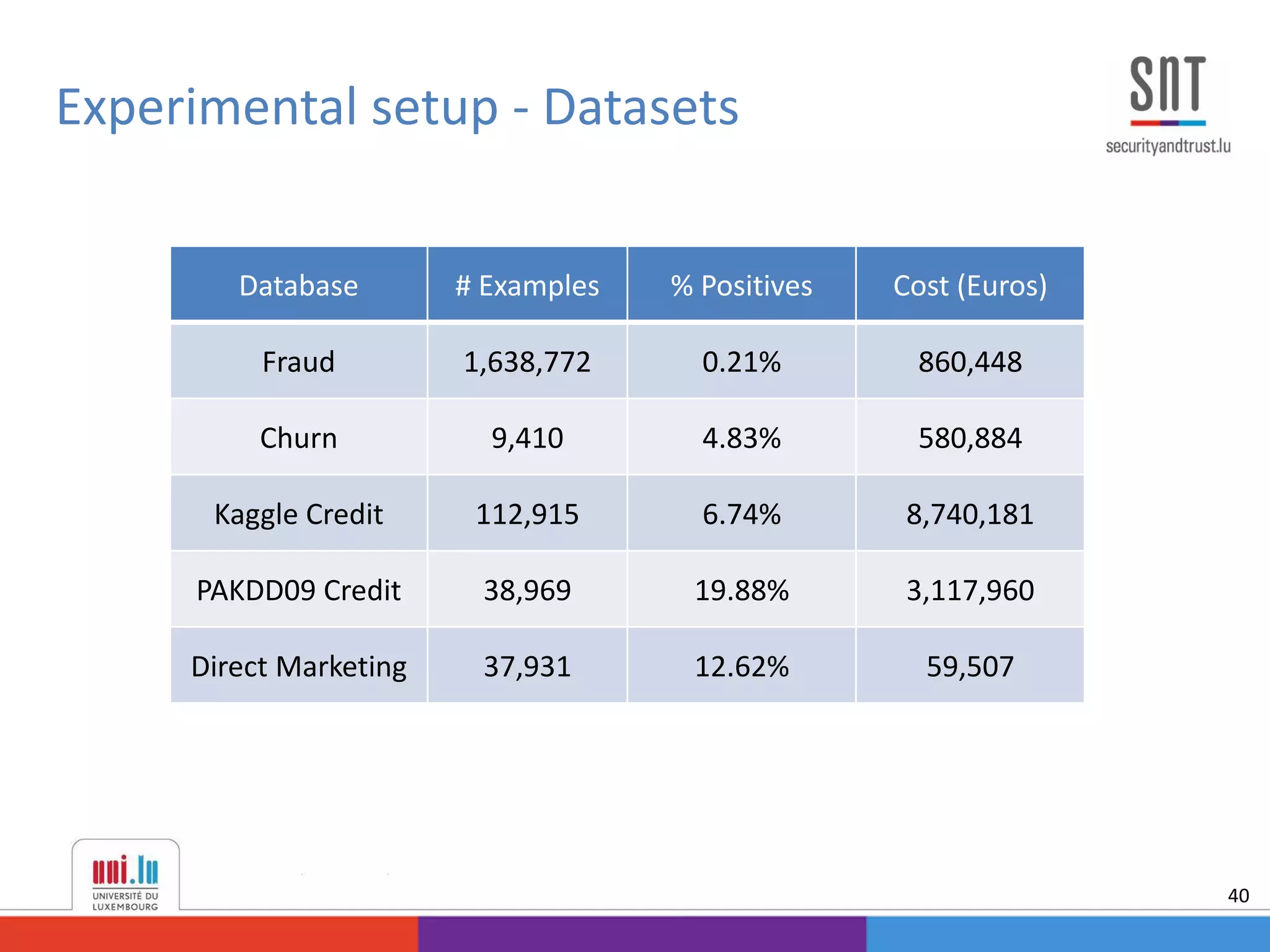

![Estimate the probability of a transaction being fraud based on analyzing

customer patterns and recent fraudulent behavior

Issues when constructing a fraud detection system [Bolton et al., 2002]:

• Skewness of the data

• Cost-sensitivity

• Short time response of the system

• Dimensionality of the search space

• Feature preprocessing

Credit card fraud detection

10](https://image.slidesharecdn.com/thesisexampledependentcostsensitiveclassificationslides-150923041551-lva1-app6892/75/PhD-Defense-Example-Dependent-Cost-Sensitive-Classification-10-2048.jpg)

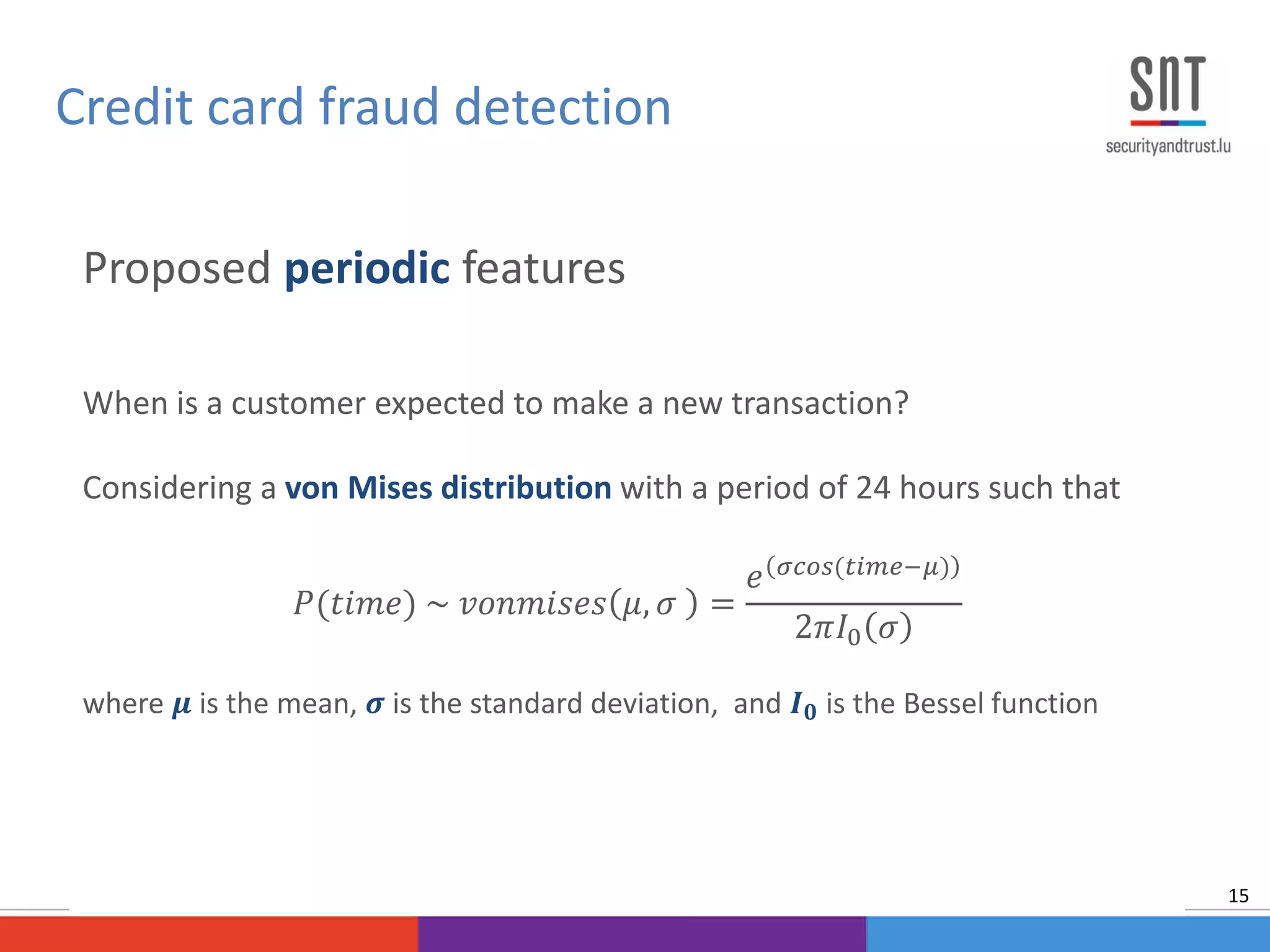

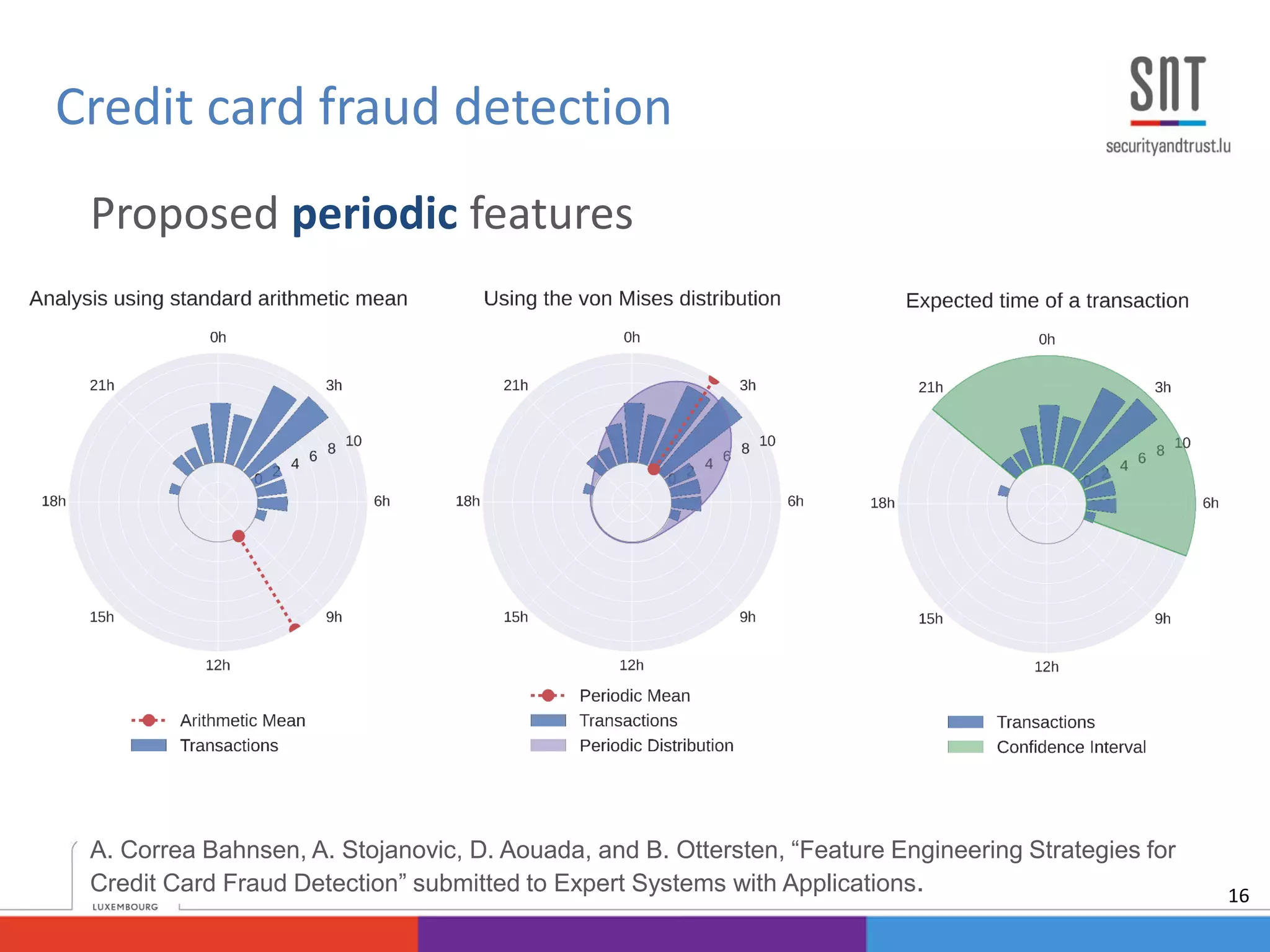

![Transaction aggregation strategy [Whitrow, 2008]

Credit card fraud detection

14

Raw Features

TrxId Time Type Country Amt

1 1/1 18:20 POS Lux 250

2 1/1 20:35 POS Lux 400

3 1/1 22:30 ATM Lux 250

4 2/1 00:50 POS Ger 50

5 2/1 19:18 POS Ger 100

6 2/1 23:45 POS Ger 150

7 3/1 06:00 POS Lux 10

Aggregated Features

No Trx

last 24h

Amt last

24h

No Trx

last 24h

same

type and

country

Amt last

24h same

type and

country

0 0 0 0

1 250 1 250

2 650 0 0

3 900 0 0

3 700 1 50

2 150 2 150

3 400 0 0](https://image.slidesharecdn.com/thesisexampledependentcostsensitiveclassificationslides-150923041551-lva1-app6892/75/PhD-Defense-Example-Dependent-Cost-Sensitive-Classification-14-2048.jpg)

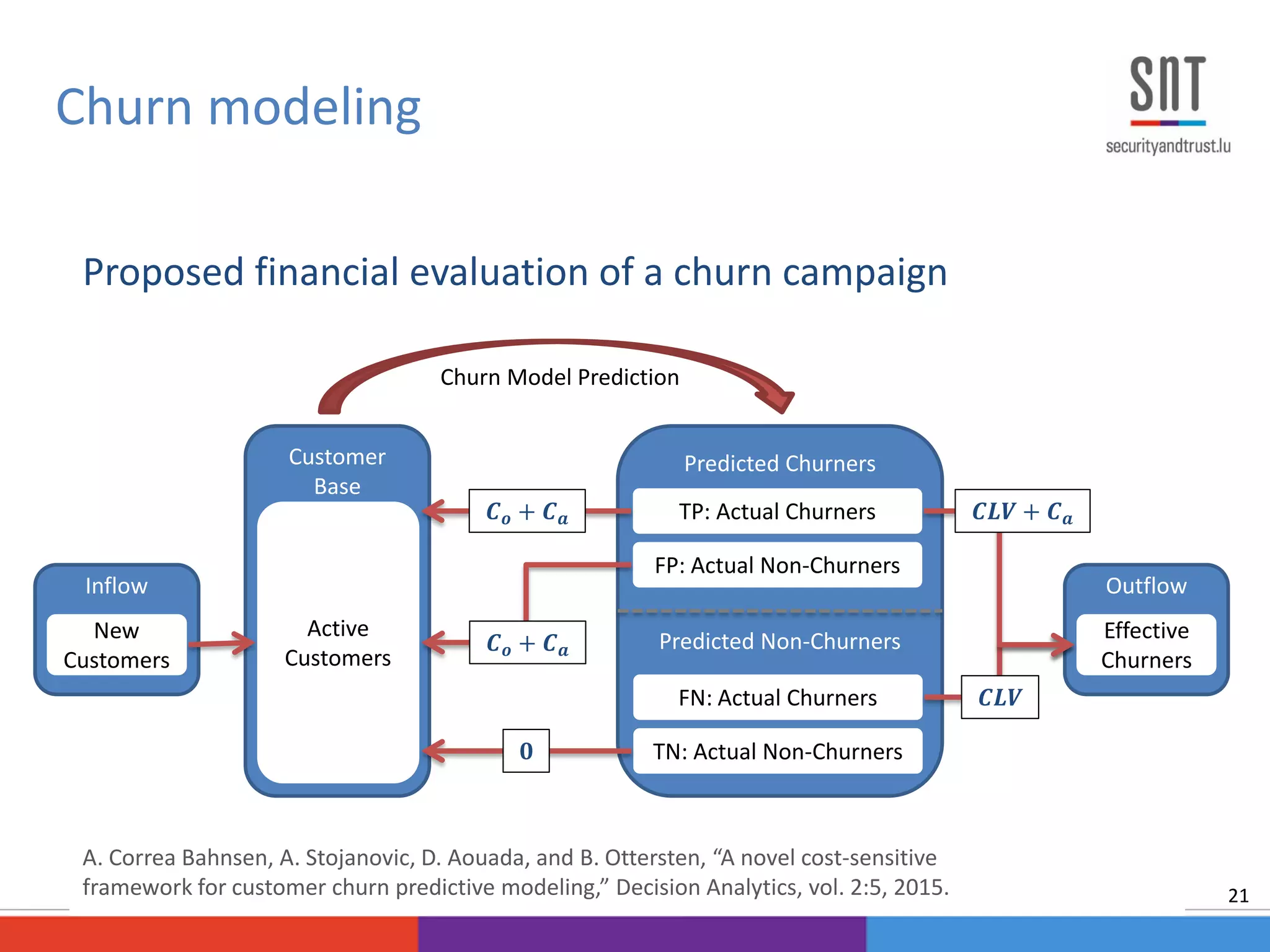

![Churn management campaign [Verbraken, 2013]

Churn modeling

20

Inflow

New

Customers

Customer

Base

Active

Customers

Predicted Churners

Predicted Non-Churners

TP: Actual Churners

FP: Actual Non-Churners

FN: Actual Churners

TN: Actual Non-Churners

Outflow

Effective

Churners

Churn Model Prediction

1

1

𝟏 − 𝜸𝜸

1](https://image.slidesharecdn.com/thesisexampledependentcostsensitiveclassificationslides-150923041551-lva1-app6892/75/PhD-Defense-Example-Dependent-Cost-Sensitive-Classification-20-2048.jpg)

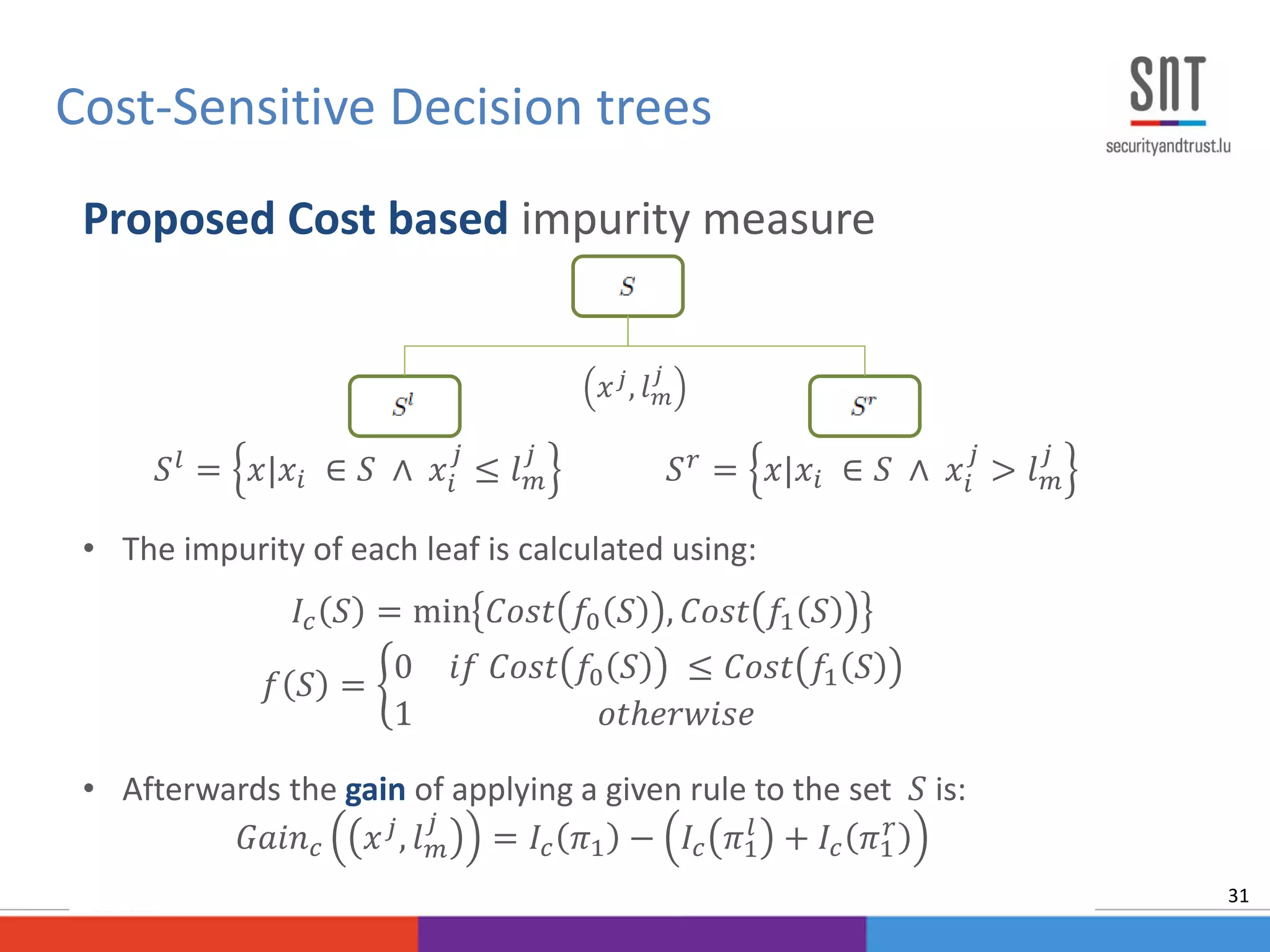

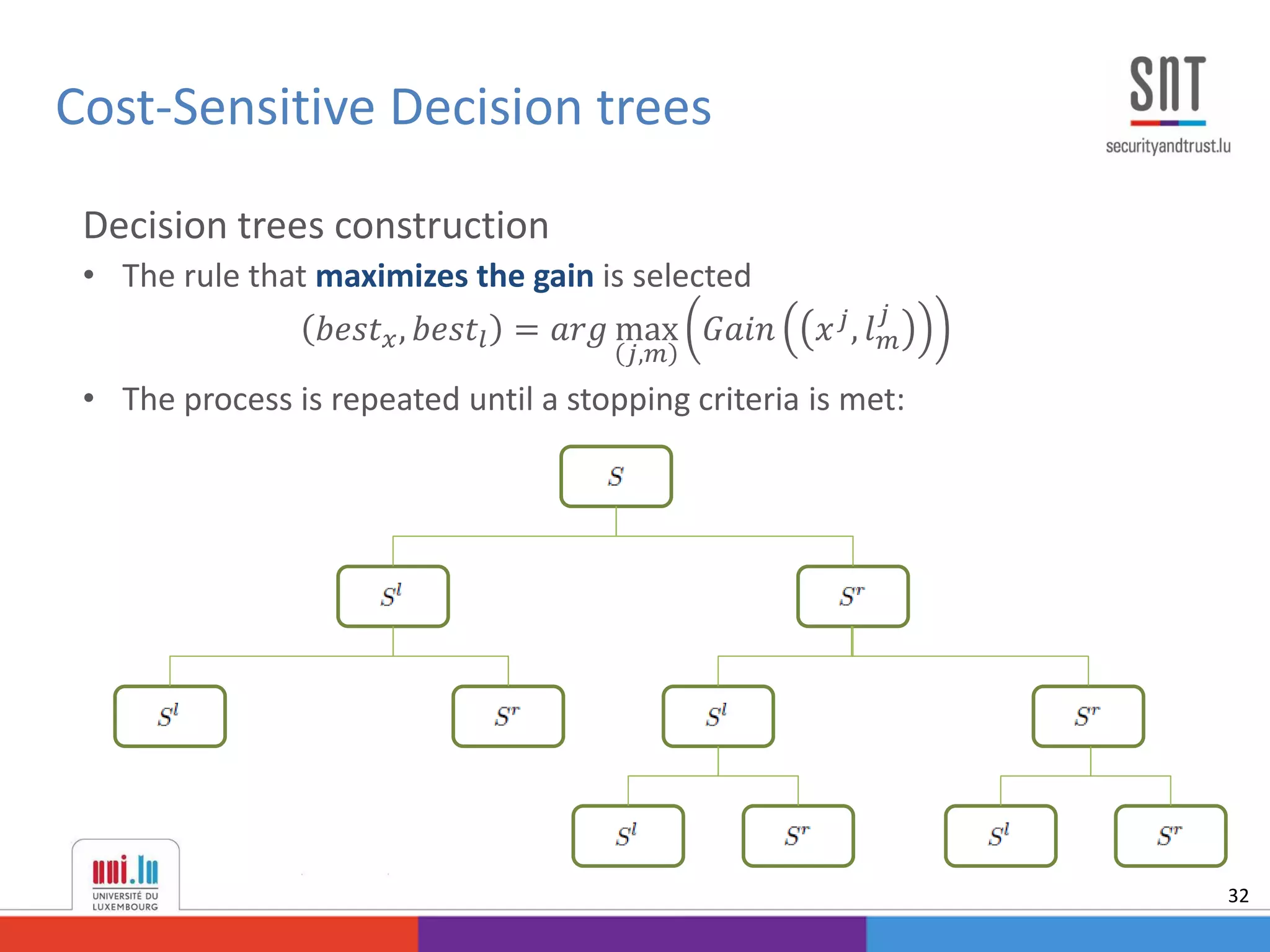

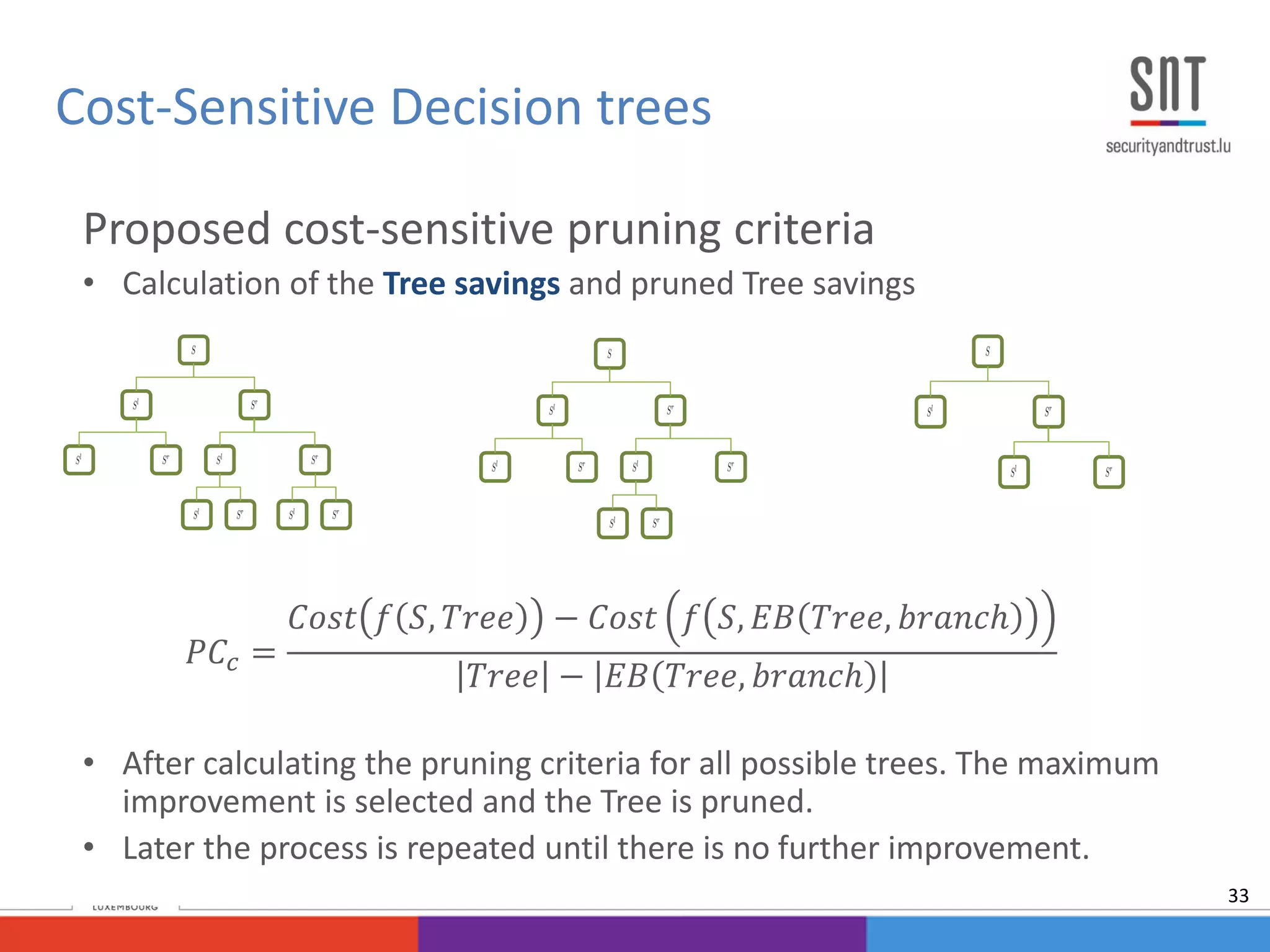

![• A decision tree is a classification model that iteratively creates binary

decision rules 𝑥 𝑗, 𝑙 𝑚

𝑗

that maximize certain criteria (gain, entropy, …).

Where 𝑥 𝑗, 𝑙 𝑚

𝑗

refers to making a rule using feature j on value m

• Maximize the accuracy is different than maximizing the cost.

• To solve this, some studies had been proposed method that aim to

introduce the cost-sensitivity into the algorithms [Lomax 2013].

However, research have been focused on class-dependent methods

• We proposed:

• Example-dependent cost based impurity measure

• Example-dependent cost based pruning criteria

Cost-Sensitive Decision trees

30](https://image.slidesharecdn.com/thesisexampledependentcostsensitiveclassificationslides-150923041551-lva1-app6892/75/PhD-Defense-Example-Dependent-Cost-Sensitive-Classification-30-2048.jpg)

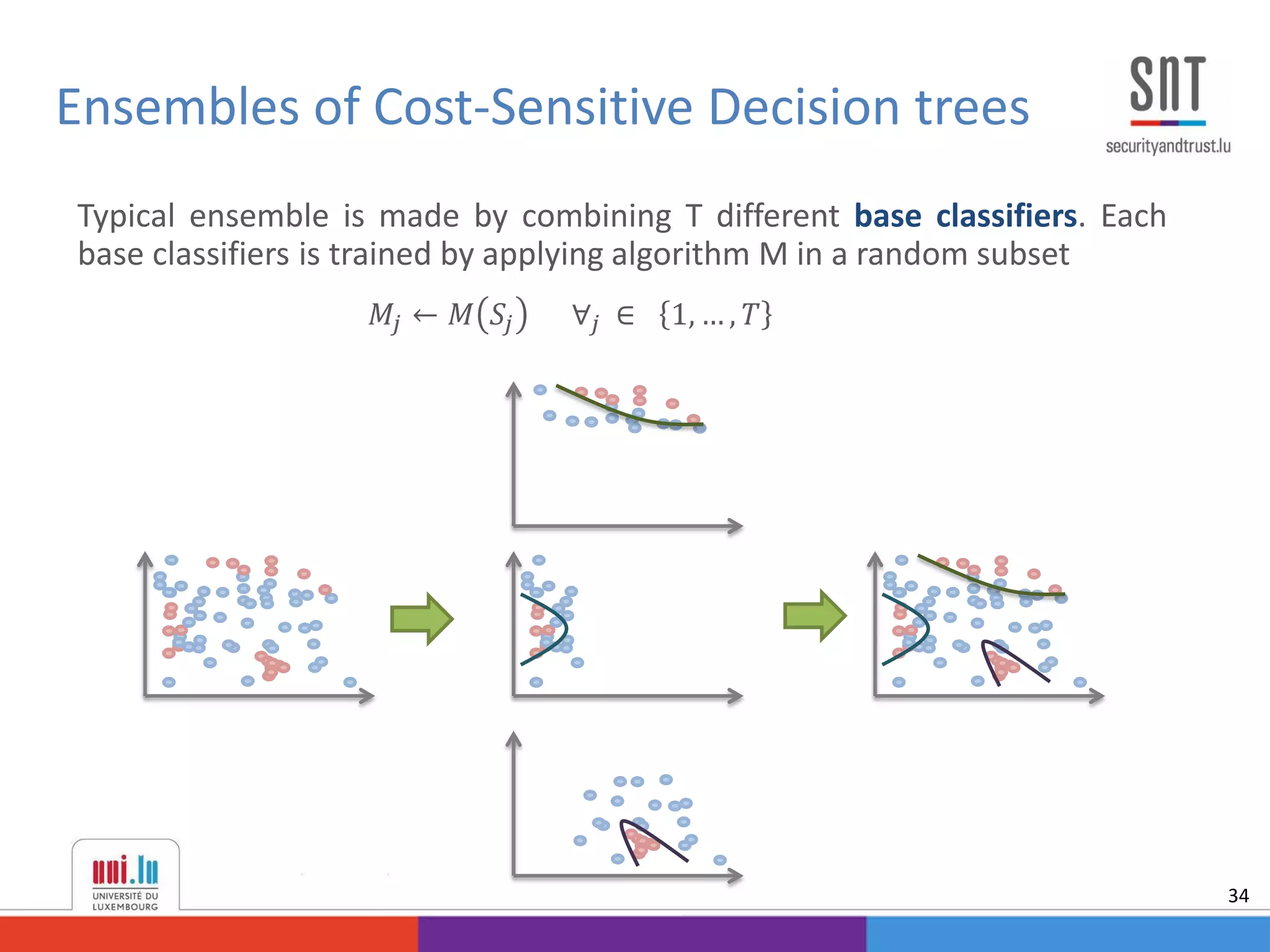

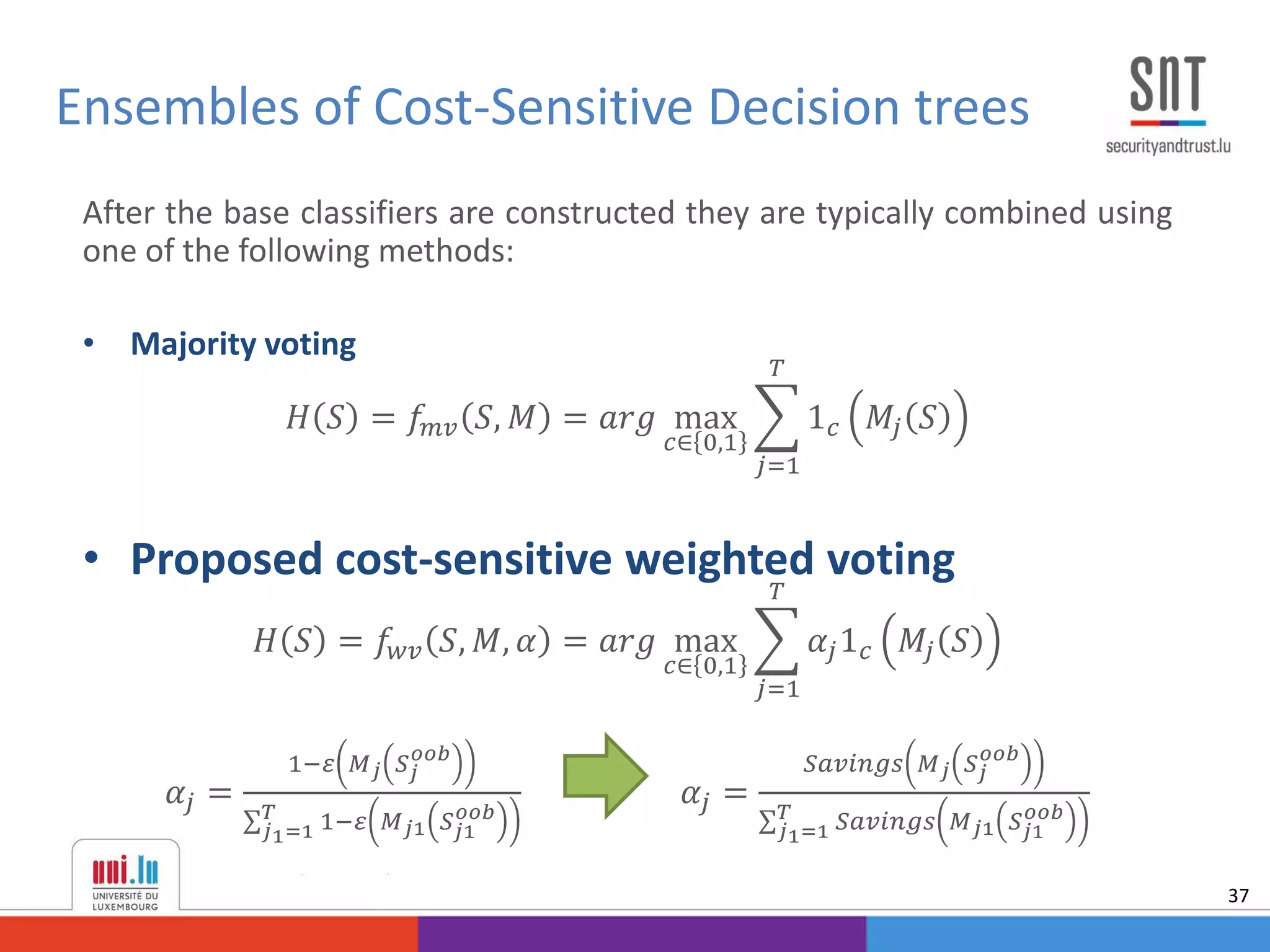

![• Proposed cost-sensitive stacking

𝐻 𝑆 = 𝑓𝑠 𝑆, 𝑀, 𝛽 =

1

1 + 𝑒

− 𝑗=1

𝑇

𝛽 𝑗 𝑀 𝑗 𝑆

Using the cost-sensitive logistic regression [Correa et. al, 2014] model:

𝐽 𝑆, 𝑀, 𝛽 =

𝑖=1

𝑁

𝑦𝑖 𝑓𝑠 𝑆, 𝑀, 𝛽 𝐶 𝑇𝑃 𝑖

− 𝐶 𝐹𝑁𝑖

+ 𝐶 𝐹𝑁 𝑖

+

1 − 𝑦𝑖 𝑓𝑠 𝑆, 𝑀, 𝛽 𝐶 𝐹𝑃 𝑖

− 𝐶 𝑇𝑁 𝑖

+ 𝐶 𝑇𝑁 𝑖

Then the weights are estimated using

𝛽 = 𝑎𝑟𝑔 min

𝛽

𝐽 𝑆, 𝑀, 𝛽

Ensembles of Cost-Sensitive Decision trees

38](https://image.slidesharecdn.com/thesisexampledependentcostsensitiveclassificationslides-150923041551-lva1-app6892/75/PhD-Defense-Example-Dependent-Cost-Sensitive-Classification-38-2048.jpg)

This document discusses example-dependent cost-sensitive classification techniques in financial risk modeling and marketing analytics, emphasizing their importance in real-world applications such as credit card fraud detection, churn modeling, credit scoring, and direct marketing. It outlines traditional classification methods' limitations concerning misclassification costs and proposes cost-sensitive algorithms, including Bayes minimum risk and cost-sensitive decision trees. The document also highlights the implications of these methodologies through experimental setups and results.

![[DSC Europe 25] Branko Urosevic -Rethinking Financial Talent: Integrating Cod...](https://cdn.slidesharecdn.com/ss_thumbnails/8jjrus8ttko6qj64f58f-3-251212103250-642c6374-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Hans Kleinsman - The Compliance Gearbox: How Tax Tech Mediate...](https://cdn.slidesharecdn.com/ss_thumbnails/dxdytie1toel0hr90bjs-2-251212103250-174fdbe7-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Debmalya Biswas - Agentification: the art of transforming man...](https://cdn.slidesharecdn.com/ss_thumbnails/r5azlggvtqiaiiusrqdr-4-251212103249-5a12c89b-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Jovan Bogicevic - Legacy to AI-Driven Defense: Transforming D...](https://cdn.slidesharecdn.com/ss_thumbnails/rsarluadt563hntyfc8q-3-251211083849-3e7bc4c0-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dusan Nesic - Securing Tomorrow’s Infrastructure: Why Cyber-P...](https://cdn.slidesharecdn.com/ss_thumbnails/qikbszfftyowjm2q6duw-1-251211083848-8f2ead6b-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Bassam Maharmeh - Artificial Intelligence: Opportunities and ...](https://cdn.slidesharecdn.com/ss_thumbnails/thhfmr2fqpawzj7hsjpg-5-251211083048-2c23204f-thumbnail.jpg?width=640&height=640&fit=bounds)