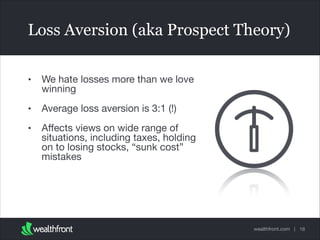

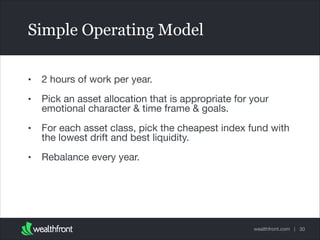

This document provides an overview of personal finance basics for engineers. It discusses how behavioral finance concepts like anchoring, mental accounting, and loss aversion affect financial decision making. It emphasizes the importance of cash flow, emergency funds, spending less than you earn, and the power of compound returns over long periods. The document recommends keeping investing simple through low-cost index funds and rebalancing annually.