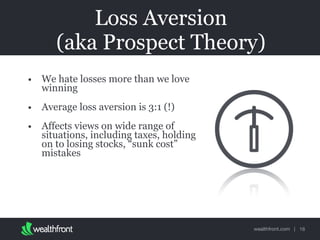

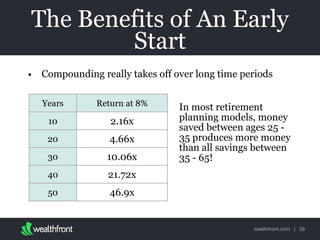

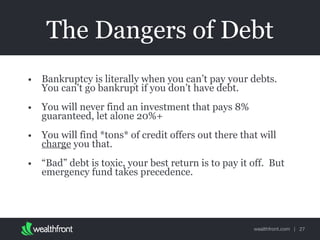

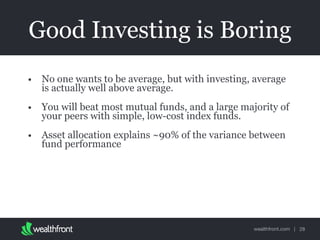

The document discusses fundamental concepts in personal finance, emphasizing the importance of self-awareness regarding irrational behaviors influencing financial decisions. Key topics include liquidity, cash flow management, the benefits of compounding interest, and the dangers of debt, alongside behavioral biases that affect investment choices. It advocates for a long-term, boring approach to investing, focusing on low-cost index funds and proper asset allocation.