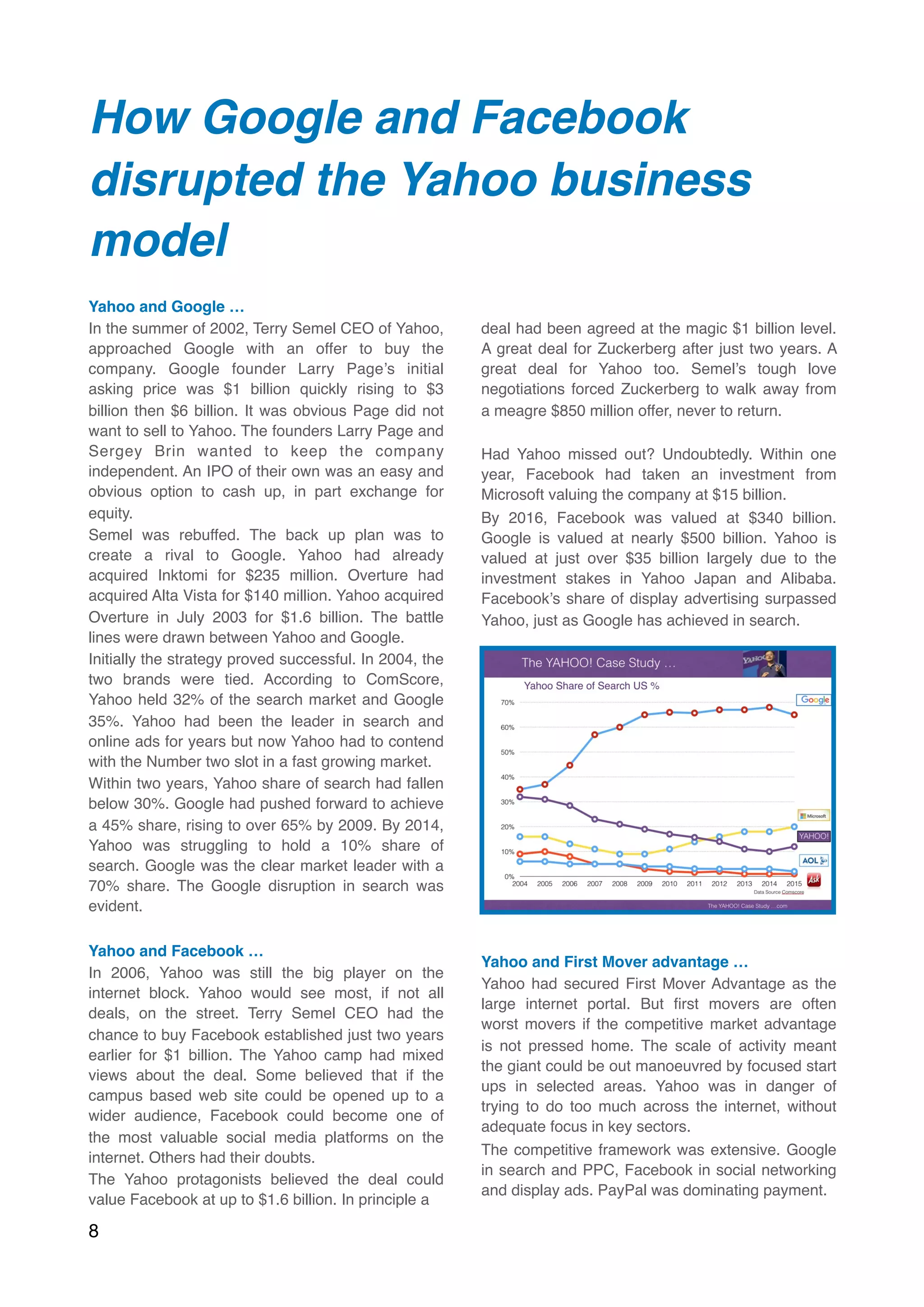

Download to read offline

![Digital Disruption and the

Challenge to the UK Banking

System

Digital Disruption and the Challenge to the

Banking System …

In 2016 the Competition Market Authority [CMA]

released the final report on the UK Banking

System. Despite fears about digital disruption and

the potential “uberization” of the bank network,

change is slow to take effect.

The report concludes the smaller, newer,

“challenger” banks find it difficult to grow. Older,

larger, legacy banks do not have to compete “hard

enough” for customers’ business.

Switching, the process by which customers change

bank accounts from one bank to another is still

extremely low. Switching accounts for between 3%

and 4% of total current account business.

The CMA would like to see the dominance of the

Big Four, HSBC, Barclays, Lloyds and RBS

diminished. In 2014 it is estimated the big four, plus

Santander, had a combined UK current accounts

market share of 85%. Add in TSB, Nationwide and

the Co-operative Bank and the total increases to

97%.

For the new challenger banks like OakNorth,

Aldermore, Mondo and Atom the challenge is

particularly difficult. Despite a strong Fintech mobile

platform, Mondo, Atom and Tandem will struggle to

recreate, in banking, the success of AirBnB and

Uber in hotels and transportation.

Scaleability is a difficult growth challenge when

confronted with customer inertia. In banking, far

more is at risk than calling a cab or booking a

room. The commitment Life Time Value [LTV] has

much more at stake as clients put their savings,

houses and transactions on the line.

Customer inertia, with a switching rate sub 4% will

inhibit the growth of challengers whether digital or

not. The marketing spend and capital requirements

to achieve critical mass, are significant

impediments to rapid growth.

So what can the CMA achieve …?

The CMA would like to develop an “Open Banking”

network. A world in which customers are able to

move accounts more easily and more regularly.

Price and performance comparisons should feature

as part of the banks’ marketing profiles.

APIs would be linked to all major banking systems.

Clients would receive reliable, personalised,

financial advice, precisely tailored to individual

circumstances delivers securely and confidentially.

Big data and predictive analytics would enable

cash forecasting to warn of impending

overspending. The standards set by the Empires of

the Cloud, Google, Apple, Facebook and Amazon

are becoming the norm for the banking network.

“People who bought this also bought this, but you

can’t afford it - so don’t look at that site again!”

With Open Banking, apps could use transaction

information to find the current account deals which

suit best. Running a small business, apps could

find the best options for business accounts and

loans. Apps could even help avoid overdraft

charges by moving cash into accounts when they

dip into the red.

17](https://image.slidesharecdn.com/digitaldisruption-181203130913/75/Our-Guide-to-Digital-disruption-Update-2019-17-2048.jpg)

This document discusses digital disruption and its causes. It identifies six global forces shaping digital disruption: 1) increasing connectivity through mobile phones and other devices, 2) the growing number of connected devices and emergence of the internet of things, 3) exponential growth in data creation and need for data storage, 4) lower barriers to market participation. These forces are accelerating changes in business models and challenging traditional companies through new entrants like Uber and Airbnb.