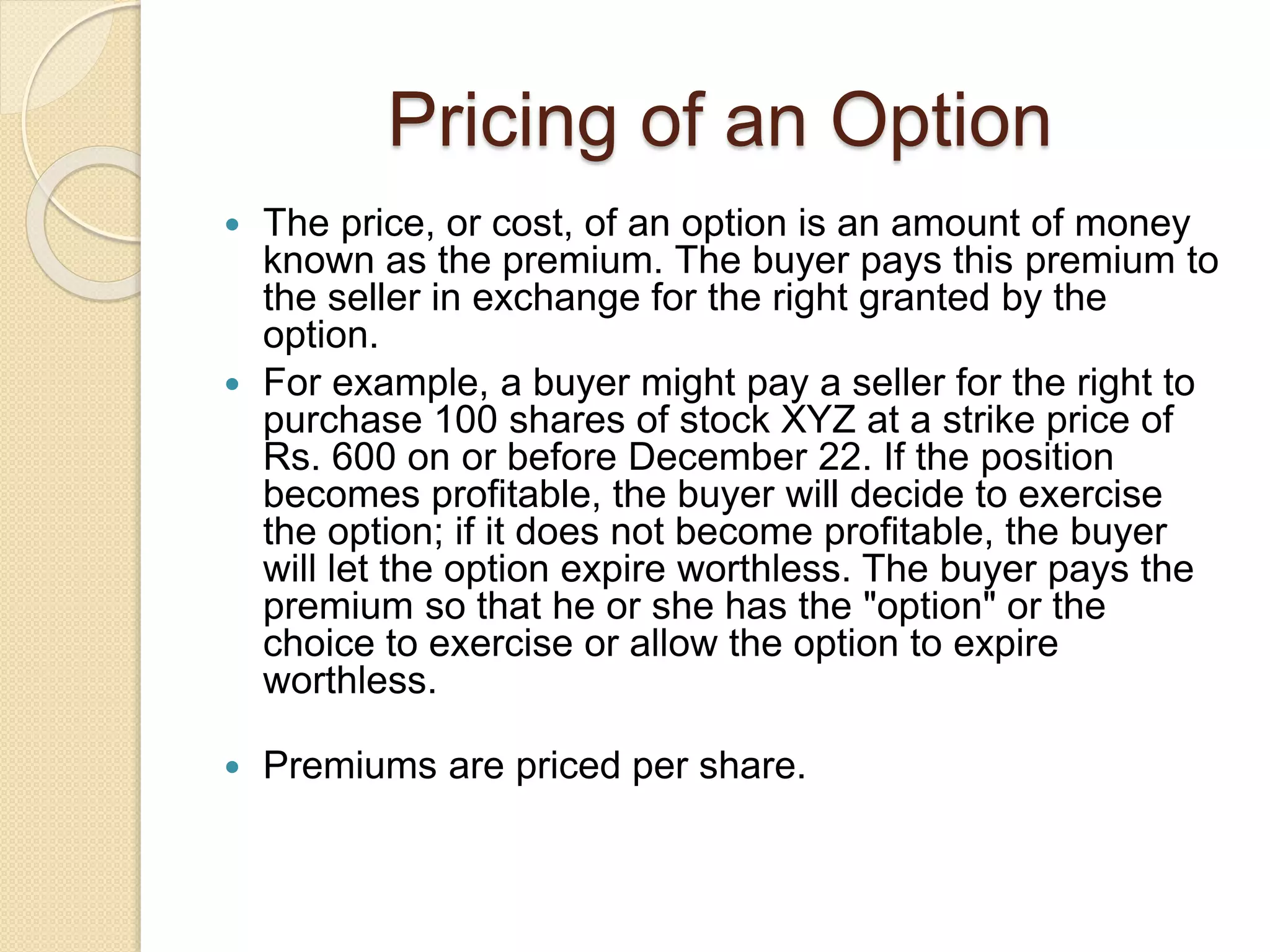

The document discusses pricing of options. It defines what an option is, the two main types of options - calls and puts, and some key terminology used related to options. It then discusses the major factors that affect the pricing of an option, including the spot price of the underlying asset, time until expiration, volatility, distance between the strike price and spot price, and risk-free rate of return. The document also discusses intrinsic and time value that make up an option's premium price. It concludes by covering the Black-Scholes model for pricing options theoretically based on these factors.

![ict_presentation_final_final_final[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/ictpresentationfinalfinalfinal1-251230145259-2b4839bd-thumbnail.jpg?width=640&height=640&fit=bounds)