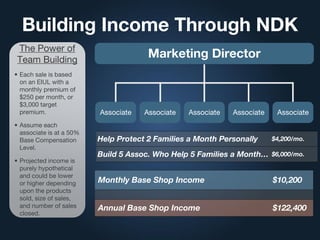

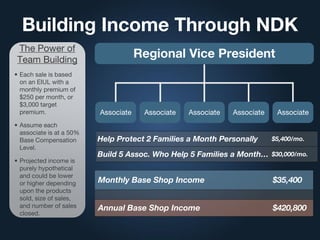

This document provides information about NDK Insurance Agents, including what they do, their mission, vision, and the companies they represent. They specialize in various types of retirement planning, insurance, and asset protection for individuals, families, and businesses. Their goal is to actualize clients' dreams through cutting-edge financial solutions and become the premier financial solutions provider across the nation. The document also discusses various financial planning strategies and concepts around investing, taxes, and building wealth over time through compound interest.