Download to read offline

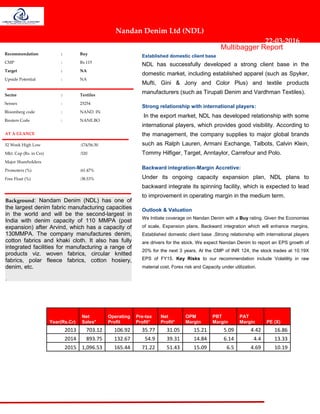

NDL is one of the largest denim fabric manufacturers in the world. It has an established client base in India and supplies international brands. It plans to expand capacity which will drive revenue growth. Backward integration of spinning will improve margins. The stock currently trades at a reasonable valuation and further expansion positions the company for strong performance. Key risks include volatility in raw materials and underutilization of new capacity.