Q3FY15: Buy PTC India for upside 22%, target price 109

•

1 like•321 views

PTC India reported lower than estimated quarterly revenues and profits. Revenues were INR28.2 billion, lower than the estimate of INR33 billion due to lower trading volumes and realization. Reported profit was INR66 million versus the estimate of INR364 million. However, adjusted profit of INR391 million was boosted by rebate and surcharge income. Trading margins of Ps4.7/unit were better than estimated but tolling margins and volumes were lower. Grid constraints impacted overall volumes. The company maintains a buy rating with a target price of INR109 per share based on a sum-of-the-parts valuation.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Q3FY15: Buy PTC India for upside 22%, target price 109

Similar to Q3FY15: Buy PTC India for upside 22%, target price 109 (20)

More from IndiaNotes.com

More from IndiaNotes.com (20)

Recently uploaded

Recently uploaded (20)

Q3FY15: Buy PTC India for upside 22%, target price 109

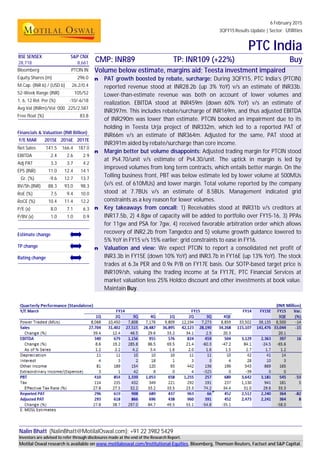

- 1. 6 February 2015 3QFY15 Results Update | Sector: Utilities PTC India Nalin Bhatt (NalinBhatt@MotilalOswal.com); +91 22 3982 5429 BSE SENSEX S&P CNX CMP: INR89 TP: INR109 (+22%) Buy28,718 8,661 Bloomberg PTCIN IN Equity Shares (m) 296.0 M.Cap. (INR b) / (USD b) 26.2/0.4 52-Week Range (INR) 105/52 1, 6, 12 Rel. Per (%) -10/-6/18 Avg Val (INRm)/Vol ‘000 225/2,587 Free float (%) 83.8 Financials & Valuation (INR Billion) Y/E MAR 2015E 2016E 2017E Net Sales 141.5 166.4 187.0 EBITDA 2.4 2.6 2.9 Adj PAT 3.3 3.7 4.2 EPS (INR) 11.0 12.4 14.1 Gr. (%) -9.6 12.7 13.7 BV/Sh.(INR) 88.3 93.0 98.3 RoE (%) 7.5 9.4 10.0 RoCE (%) 10.4 11.4 12.2 P/E (x) 8.0 7.1 6.3 P/BV (x) 1.0 1.0 0.9 Estimate change TP change Rating change Volume below estimate, margins aid; Teesta investment impaired n PAT growth boosted by rebate, surcharge: During 3QFY15, PTC India’s (PTCIN) reported revenue stood at INR28.2b (up 3% YoY) v/s an estimate of INR33b. Lower-than-estimate revenue was both on account of lower volumes and realization. EBITDA stood at INR459m (down 60% YoY) v/s an estimate of INR397m. This includes rebate/surcharge of INR169m, and thus adjusted EBITDA of INR290m was lower than estimate. PTCIN booked an impairment due to its holding in Teesta Urja project of INR332m, which led to a reported PAT of INR66m v/s an estimate of INR364m. Adjusted for the same, PAT stood at INR391m aided by rebate/surcharge than core income. n Margin better but volume disappoints: Adjusted trading margin for PTCIN stood at Ps4.70/unit v/s estimate of Ps4.30/unit. The uptick in margin is led by improved volumes from long term contracts, which entails better margin. On the Tolling business front, PBT was below estimate led by lower volume at 500MUs (v/s est. of 610MUs) and lower margin. Total volume reported by the company stood at 7.7BUs v/s an estimate of 8.5BUs. Management indicated grid constraints as a key reason for lower volumes. n Key takeaways from concall: 1) Receivables stood at INR31b v/s creditors at INR17.5b, 2) 4.8gw of capacity will be added to portfolio over FY15-16, 3) PPAs for 11gw and PSA for 7gw, 4) received favorable arbitration order which allows recovery of INR2.2b from Tangedco and 5) volume growth guidance lowered to 5% YoY in FY15 v/s 15% earlier; grid constraints to ease in FY16. n Valuation and view: We expect PTCIN to report a consolidated net profit of INR3.3b in FY15E (down 10% YoY) and INR3.7b in FY16E (up 13% YoY). The stock trades at 6.3x PER and 0.9x P/B on FY17E basis. Our SOTP-based target price is INR109/sh, valuing the trading income at 5x FY17E, PTC Financial Services at market valuation less 25% Holdco discount and other investments at book value. Maintain Buy. Investors are advised to refer through disclosures made at the end of the Research Report. Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

- 2. 6 February 2015 2 PTC India 3QFY15 reported performance boosted by rebate/surcharge income n PTC India reported revenues of INR28.2b, lower than our estimate of INR33b. This was led by lower trading volumes at 7.7BUs vs our volume estimate of 8.5BUs. Also, the average realization for the quarter stood better at INR3.88/unit in 3QFY15, vs INR3.35/unit YoY. Tolling volumes stood at 500MUs, vs our estimate of 610MUs. n We note that volume growth de-grew (down 7% YoY) for the first time since 1QFY13. Management indicated that ST and OTC volumes were lower on the wake of DISCOM issues. Moreover, the volume growth was impacted due to transmission bottleneck. Despite higher volumes contracted by PTC, ~61% of contracted power could not flow owing to grid constraint. Exhibit 1: Volume growth decline owing to grid constraints 37% 21% 31% 62% 17% 12% -21%-16% -2% 9% 29% 54% 28% 15% 40% 14% 21% 18% -6% 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12 2QFY12 3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 2QFY15 3QFY15 Units Traded(MUs) YoY Growth(%) Source: Company n Reported revenue includes INR42.7m of gain owing to surcharge and rebate income of INR126m. EBIDTA thus, stood at INR459m on reported basis and INR290m, after taking off surcharge and rebate income. n This was lower than our estimate of INR397m. Lower volume growth was partly offset by higher margins in trading business. n PBT for the company stood at INR257m, as PTC booked an impairment of its investment in Teesta Urja hydro power project. PTC is set to divest part of its investment in project in favour of Government of Sikkim to enable holding of 51% by State government. Such transfer was valued at below face value and thus there will be a loss of INR65m on transfer. n While PTC created provision for such loss, it also impaired its balance holding in project on conservative basis and made further provision of INR266.9m. However, this would be evaluated closer to project CoD (March 2016) and would be treated accordingly. n Reported PAT thus stood at mere INR66m vs estimate of INR364m. Adjusted for impairment, the PAT stood at INR391m, though aided by rebate and surcharge. Adjusted for rebate/surcharge income, PAT stood at INR279m, lower than estimate. Margin for trading better, tolling margin impacted n For the 3QFY15, the tolling volumes stood at 500MUs, lower than our estimate of 610MUs. Tolling PBT, in our view, stood at INR82m, vs estimate of INR162m. Management indicated that lower coal prices and fixed plus margin structure of offtake has impacted margins in tolling business.

- 3. 6 February 2015 3 PTC India n Trading margin stood at Paisa4.7/unit post adjustments for rebate and net surcharge. This was higher than our estimate of margins at Paisa 4.3/unit. Exhibit 2: Margins remain range bound (Ps/unit) 5.0 4.6 4.3 5.3 4.9 4.2 3.8 4.7 4.0 3.1 3.7 3.7 6.3 4.1 4.2 3.1 4.4 5.2 4.7 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12 2QFY12 3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 2QFY15 3QFY15 Source: Company Exhibit 3: Surcharge income boosts contribution (INR m) 239 144 109 176 25 43 27 129 91 230 810 606 109 189 169 1QFY12 2QFY12 3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 2QFY15 3QFY15 Source: Company Net receivable position remains elevated n As at FY14, the gross trade receivable for PTC on standalone basis stood at INR20.9b, vs INR21.4b as at March 2013. Last year, the company had outstanding receivable dues from TN and UP, which has been cleared in FY14. Despite this, the sustained level of receivable could be owing to higher volumes necessitating higher working capital requirement. n We thus look at the net open position. So, trade payable for PTC stood at INR17.5, and net receivable stood at INR31b. n Utilization of cash and cash equivalent of INR5b remain key to watch out for. Key takeaways from concall n 4.8GW of capacity will be added to portfolio over FY15-16E, n PPAs signed for 11GW, while PSA are in place for ~7GW. Large part of upcoming capacity tied-up back to back and thus does not pose any major challenge. n Also, tariff framework is manageable and even assuming open capacity in the interim. n Commencement of supply of power, 200 MW each, to Haryana and Uttar Pradesh and 104MW to Rajasthan from Jaypee Karcham Wangtoo on LT basis. n Favourable outcome in arbitration allows recovery of INR2.2b from TANGEDCO. n FY15E Volume growth likely at 5%, vs earlier anticipation of 15% due to grid constrains, expect it to ease out in FY16E. Valuations and view n We expect PTC to report consolidated net profit of INR3.3b in FY15E (down 10% YoY) and INR3.7b in FY16E (up 13% YoY). PTC trades at 6.3x PER and 0.9x P/B on FY17E basis. n Our SOTP based TP is INR109/sh, valuing trading income at 5x FY17E, PTC Financial services at market valuation less 25% HOLDCO discount and other investment at book value. Buy.

- 4. 6 February 2015 4 PTC India Financials and valuations Income Statement (INR Million) Y/E March 2011 2012 2013 2014 2015E 2016E 2017E Total Revenues 90,632 76,502 88,569 123,084 141,476 166,390 186,974 Total Expenses 89,232 75,049 86,869 119,507 139,113 163,766 184,117 EBITDA 1,400 1,453 1,700 3,577 2,363 2,624 2,857 % of Total Revenues 1.5 1.9 1.9 2.9 1.7 1.6 1.5 Depreciation 50 45 42 42 41 42 43 Interest 11 260 9 28 10 10 10 Other Income 628 505 119 543 869 1,043 1,252 Extra Ordinary -2 -3 -17.16 0 321.8 0 0 PBT 1,969 1,656 1,785 4,051 3,503 3,616 4,055 Tax 576 452 497 1,130 941 1,085 1,217 Rate (%) 29.3 27.3 27.9 27.9 26.9 30.0 30.0 Reported PAT 1,393 1,204 1,287 2,921 2,562 2,531 2,839 Change (%) 86.7 -13.6 7.0 126.9 -12.3 -1.2 12.2 Adjusted PAT 1,351 1,201 1,270 2,473 2,241 2,531 2,839 Change (%) 43.6 -11.1 5.8 94.7 -9.4 13.0 12.2 Consolidated PAT 1,660 2,041 1,983 3,608 3,263 3,676 4,180 Change (%) 50.3 22.9 -2.9 82.0 -9.6 12.7 13.7 Balance Sheet (INR Million) Y/E March 2011 2012 2013 2014 2015E 2016E 2017E Share Capital 2,950 2,950 2,960 2,960 2,960 2,960 2,960 Reserves 18,852 19,551 20,297 22,124 23,179 24,571 26,133 Net Worth 21,802 22,501 23,257 25,084 26,139 27,531 29,093 Loans 0 0 0 0 0 0 0 Deferred Tax Liability 75 63 0 0 0 0 0 Minority Interest 0 0 0 0 0 0 0 Capital Employed 21,876 22,564 23,257 25,084 26,139 27,531 29,093 Gross Fixed Assets 621 626 643 670 689 711 726 Less: Depreciation 240 285 327 369 410 452 495 Net Fixed Assets 380 341 327 301 279 260 232 Investments 10,527 8,235 9,245 9,598 9,367 9,367 9,367 Curr. Assets 16,980 27,543 25,599 27,186 27,495 27,965 28,723 Debtors 9,779 25,810 21,421 20,857 17,728 15,956 14,360 Cash & Bank Balance 6,877 458 3,535 5,447 9,238 11,429 13,724 Loans & Advances 223 856 457 826 528 581 639 Other Current Assets 101 4 3 57 0 0 0 Current Liab. & Prov. 6,011 13,556 11,914 12,001 11,002 10,060 9,229 Other Liabilities 5,463 12,943 11,381 11,343 10,209 9,188 8,269 Provisions 547 613 576 721 793 872 960 Net Current Assets 10,969 13,987 13,685 15,185 16,493 17,905 19,494 Application of Funds 21,877 22,564 23,257 25,084 26,139 27,531 29,093 E: MOSL Estimates

- 5. 6 February 2015 5 PTC India Financials and valuations Ratios Y/E March 2011 2012 2013 2014 2015E 2016E 2017E Basic (INR) EPS 4.6 4.1 4.3 9.9 7.6 8.6 9.6 Consol EPS 5.6 6.9 6.7 12.2 11.0 12.4 14.1 CEPS (INR) 4.9 4.2 4.5 10.0 6.6 8.7 9.7 Book Value 73.9 76.3 78.6 84.7 88.3 93.0 98.3 DPS 2.1 1.8 2.0 2.3 2.9 3.8 4.3 Payout (incl. Div. Tax.) 45.0 45.0 45.0 23.5 45.0 45.0 45.0 Valuation (x) P/E (Standalone) 19.3 21.8 20.6 9.0 11.7 10.4 9.2 P/E (Consolidated) 15.7 12.8 13.2 7.3 8.0 7.1 6.3 EV/EBITDA 12.7 17.7 13.3 5.8 7.2 5.6 4.4 EV/Sales 0.2 0.3 0.3 0.2 0.1 0.1 0.1 Price/Book Value 1.2 1.2 1.1 1.0 1.0 1.0 0.9 Dividend Yield (%) 2.4 2.1 2.2 2.6 3.3 4.3 4.9 Profitability Ratios (%) RoE 6.5 5.4 5.6 12.1 7.5 9.4 10.0 RoCE 9.2 8.6 3.8 15.0 10.4 11.4 12.2 Turnover Ratios Debtors (Days) 40 124 94 68 49 38 30 Asset Turnover (x) 0.1 0.1 0.1 0.1 0.1 0.1 0.1 Leverage Ratio Debt/Equity (x) -0.3 0.0 -0.2 -0.2 -0.4 -0.4 -0.5 Cash Flow Statement (INR Million) 2011 2012 2013 2014 2015E 2016E 2017E PBT before EO Items 1,967 1,653 1,767 4,051 3,182 3,616 4,055 Add : Depreciation 50 45 42 42 41 42 43 Interest 11 260 9 28 10 10 10 Less:DirectTaxesPaid 576 452 497 1,130 941 1,085 1,217 (Inc)/Dec in WC -2,169 -9,437 3,378 412 2,484 778 706 CF from Oper.incl EOI -717 -7,932 4,700 3,403 4,775 3,361 3,598 (Inc)/dec in FA -5 -5 -28 -16 -19 -22 -15 (Pur)/Sale of Investments -1,767 2,292 -1,009 -353 230 0 0 CF from Investments -1,772 2,286 -1,038 -369 212 -22 -15 (Inc)/Dec in Net Worth 58 26 -15 -407 0 0 0 Less : Interest Paid 11 260 9 28 10 10 10 Dividend Paid 627 542 579 687 863 1,139 1,277 Others -2 -18 0 0 0 0 CF from Fin. Activity -579 -774 -586 -1,122 -873 -1,149 -1,287 Inc/Dec of Cash -3,068 -6,419 3,076 1,912 4,114 2,190 2,295 Add: Beginning Balance 9,944 6,877 458 3,535 5,447 9,238 11,429 Closing Balance 6,877 458 3,535 5,447 9,560 11,429 13,724 E: MOSL Estimates

- 6. 6 February 2015 6 PTC India Corporate profile: PTC India Exhibit 5: Shareholding pattern (%) Dec-14 Sep-14 Dec-13 Promoter 16.2 16.2 16.2 DII 36.6 37.7 44.9 FII 25.6 24.5 18.0 Others 21.5 21.6 20.8 Note: FII Includes depository receipts Exhibit 6: Top holders Holder Name % Holding Life Insurance Corporation Of India 12.3 IDFC Premier Equity Fund 5.1 HDFC Standard Life Insurance Company Limited 4.4 Reliance Capital Trustee Co. Ltd A/C Reliance 4.0 Government Pension Fund Global 3.8 Exhibit 7: Top management Name Designation Deepak Amitabh Chairman & Managing Director Exhibit 8: Directors Name Name Deepak Amitabh M K Goel Anil Razdan* I J Kapoor Ved Kumar Jain* Jyoti Arora S Balachandran* Ravi P Singh Dipak Chatterjee* Dinesh Prasad Bhargava Dhirendra Swarup* Hemant Bhargava Harbans Lal Bajaj* *Independent Exhibit 9: Auditors Name Type K G Somani & Co Statutory Ravi Rajan & Co Internal Exhibit 10: MOSL forecast v/s consensus EPS (INR) MOSL forecast Consensus forecast Variation (%) FY15 11.0 11.3 -2.3 FY16 12.4 13.4 -7.6 FY17 14.1 16.0 -11.7 Company description PTC India Ltd. is the pioneer in power trading in India, and over the years has become a Power Solutions company. It was set up in April 1999 with a mandate to catalyze the development of large power projects by acting as a single buyer for PPAs with independent power producers on one hand and by entering multi-partite PPAs with users and SEBs under long-term arrangements on the other. The GoI has identified PTC as its nodal agency for trading power with neighboring countries. Exhibit 4: Sensex rebased

- 7. 6 February 2015 7 PTC India N O T E S

- 8. 6 February 2015 8 PTC IndiaDisclosures This document has been prepared by Motilal Oswal Securities Limited (hereinafter referred to as Most) to provide information about the company(ies) and/sector(s), if any, covered in the report and may be distributed by it and/or its affiliated company(ies). This report is for personal information of the selected recipient/s and does not construe to be any investment, legal or taxation advice to you. This research report does not constitute an offer, invitation or inducement to invest in securities or other investments and Motilal Oswal Securities Limited (hereinafter referred as MOSt) is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your general information and should not be reproduced or redistributed to any other person in any form. This report does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any advice or recommendation in this material, investors should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The price and value of the investments referred to in this material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur. MOSt and its affiliates are a full-service, integrated investment banking, investment management, brokerage and financing group. We and our affiliates have investment banking and other business relationships with a some companies covered by our Research Department. Our research professionals may provide input into our investment banking and other business selection processes. Investors should assume that MOSt and/or its affiliates are seeking or will seek investment banking or other business from the company or companies that are the subject of this material and that the research professionals who were involved in preparing this material may educate investors on investments in such business. The research professionals responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting information. Our research professionals are paid on the profitability of MOSt which may include earnings from investment banking and other business. MOSt generally prohibits its analysts, persons reporting to analysts, and members of their households from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. Additionally, MOSt generally prohibits its analysts and persons reporting to analysts from serving as an officer, director, or advisory board member of any companies that the analysts cover. Our salespeople, traders, and other professionals or affiliates may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing among other things, may give rise to real or potential conflicts of interest. MOSt and its affiliated company(ies), their directors and employees and their relatives may; (a) from time to time, have a long or short position in, act as principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein. (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions.; however the same shall have no bearing whatsoever on the specific recommendations made by the analyst(s), as the recommendations made by the analyst(s) are completely independent of the views of the affiliates of MOSt even though there might exist an inherent conflict of interest in some of the stocks mentioned in the research report Reports based on technical and derivative analysis center on studying charts company's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamental analysis. In addition MOST has different business segments / Divisions with independent research separated by Chinese walls catering to different set of customers having various objectives, risk profiles, investment horizon, etc, and therefore may at times have different contrary views on stocks sectors and markets. Unauthorized disclosure, use, dissemination or copying (either whole or partial) of this information, is prohibited. The person accessing this information specifically agrees to exempt MOSt or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold MOSt or any of its affiliates or employees responsible for any such misuse and further agrees to hold MOSt or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays. The information contained herein is based on publicly available data or other sources believed to be reliable. Any statements contained in this report attributed to a third party represent MOSt’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. This Report is not intended to be a complete statement or summary of the securities, markets or developments referred to in the document. While we would endeavor to update the information herein on reasonable basis, MOSt and/or its affiliates are under no obligation to update the information. Also there may be regulatory, compliance, or other reasons that may prevent MOSt and/or its affiliates from doing so. MOSt or any of its affiliates or employees shall not be in any way responsible and liable for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. MOSt or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations. This report is intended for distribution to institutional investors. Recipients who are not institutional investors should seek advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. Most and it’s associates may have managed or co-managed public offering of securities, may have received compensation for investment banking or merchant banking or brokerage services, may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months. Most and it’s associates have not received any compensation or other benefits from the subject company or third party in connection with the research report. Subject Company may have been a client of Most or its associates during twelve months preceding the date of distribution of the research report MOSt and/or its affiliates and/or employees may have interests/positions, financial or otherwise of over 1 % at the end of the month immediately preceding the date of publication of the research in the securities mentioned in this report. To enhance transparency, MOSt has incorporated a Disclosure of Interest Statement in this document. This should, however, not be treated as endorsement of the views expressed in the report. Motilal Oswal Securities Limited is under the process of seeking registration under SEBI (Research Analyst) Regulations, 2014. There are no material disciplinary action that been taken by any regulatory authority impacting equity research analysis activities Analyst Certification The views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject securities or issues, and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly related to the specific recommendations and views expressed by research analyst(s) in this report. The research analysts, strategists, or research associates principally responsible for preparation of MOSt research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues Disclosure of Interest Statement PTC INDIA § Analyst ownership of the stock No § Served as an officer, director or employee No Regional Disclosures (outside India) This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject MOSt & its group companies to registration or licensing requirements within such jurisdictions. For U.S. Motilal Oswal Securities Limited (MOSL) is not a registered broker - dealer under the U.S. Securities Exchange Act of 1934, as amended (the"1934 act") and under applicable state laws in the United States. In addition MOSL is not a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended (the "Advisers Act" and together with the 1934 Act, the "Acts), and under applicable state laws in the United States. Accordingly, in the absence of specific exemption under the Acts, any brokerage and investment services provided by MOSL, including the products and services described herein are not available to or intended for U.S. persons. This report is intended for distribution only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the Exchange Act and interpretations thereof by SEC (henceforth referred to as "major institutional investors"). This document must not be acted on or relied on by persons who are not major institutional investors. Any investment or investment activity to which this document relates is only available to major institutional investors and will be engaged in only with major institutional investors. In reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the "Exchange Act") and interpretations thereof by the U.S. Securities and Exchange Commission ("SEC") in order to conduct business with Institutional Investors based in the U.S., MOSL has entered into a chaperoning agreement with a U.S. registered broker-dealer, Motilal Oswal Securities International Private Limited. ("MOSIPL"). Any business interaction pursuant to this report will have to be executed within the provisions of this chaperoning agreement. The Research Analysts contributing to the report may not be registered /qualified as research analyst with FINRA. Such research analyst may not be associated persons of the U.S. registered broker-dealer, MOSIPL, and therefore, may not be subject to NASD rule 2711 and NYSE Rule 472 restrictions on communication with a subject company, public appearances and trading securities held by a research analyst account. For Singapore Motilal Oswal Capital Markets Singapore Pte Limited is acting as an exempt financial advisor under section 23(1)(f) of the Financial Advisers Act(FAA) read with regulation 17(1)(d) of the Financial Advisors Regulations and is a subsidiary of Motilal Oswal Securities Limited in India. This research is distributed in Singapore by Motilal Oswal Capital Markets Singapore Pte Limited and it is only directed in Singapore to accredited investors, as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. In respect of any matter arising from or in connection with the research you could contact the following representatives of Motilal Oswal Capital Markets Singapore Pte Limited: Anosh Koppikar Kadambari Balachandran Email : anosh.Koppikar@motilaloswal.com Email : kadambari.balachandran@motilaloswal.com Contact : (+65)68189232 Contact : (+65) 68189233 / 65249115 Office Address : 21 (Suite 31),16 Collyer Quay,Singapore 04931 Motilal Oswal Securities Ltd Motilal Oswal Tower, Level 9, Sayani Road, Prabhadevi, Mumbai 400 025 Phone: +91 22 3982 5500 E-mail: reports@motilaloswal.com