Download as PDF, PPTX

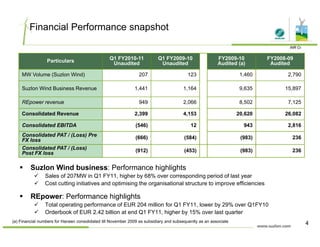

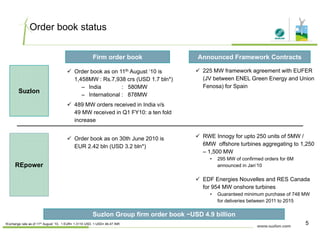

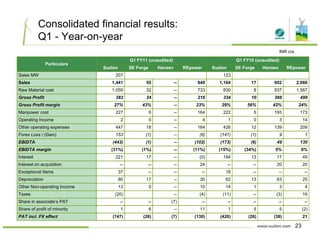

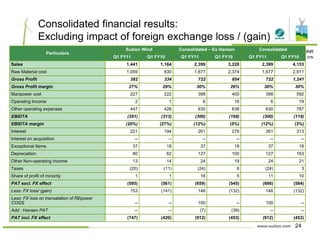

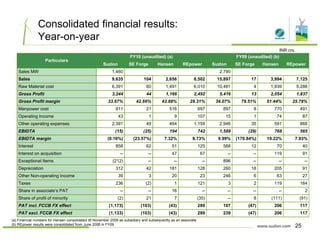

The document is Suzlon Energy Limited's presentation of its Q1 FY2011 results. Some key highlights include growth in Suzlon's wind turbine volume compared to Q1 FY2010, a significant increase in order flows in India, and the successful completion of a rights issue. The outlook suggests the wind industry will continue robust long-term growth, with the growing Indian market benefiting Suzlon. Suzlon is also working closely with REpower to strengthen their future platform.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)