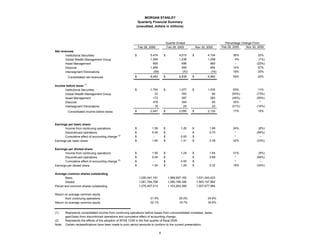

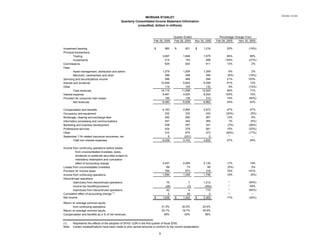

Morgan Stanley reported record first quarter results for 2006, with net revenues of $8.5 billion, up 24% from the previous year. Net income was $1.6 billion, a 17% increase, while diluted earnings per share were $1.54. All of Morgan Stanley's major business segments achieved record or near-record results, including Institutional Securities which saw a 36% rise in net revenues. The company directed additional resources to areas seeing major growth like emerging markets and leveraged finance. Morgan Stanley also continued international expansion and reorganized some business divisions to drive better performance.