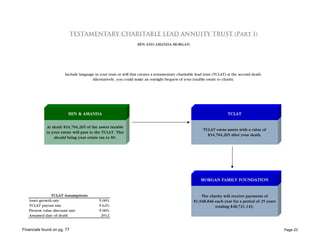

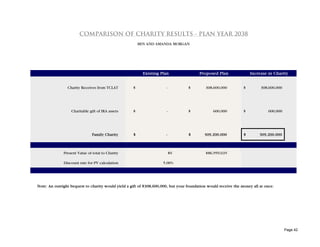

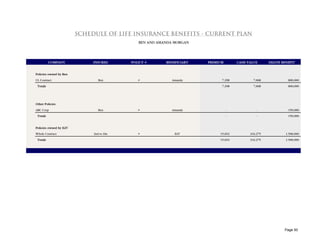

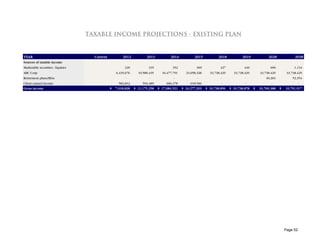

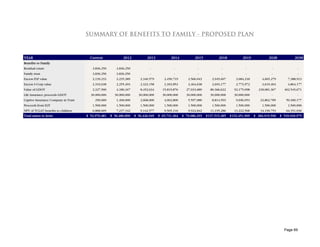

The document outlines an estate and financial planning strategy for clients Ben and Amanda Morgan, which includes maintaining their lifestyle, securing financial stability for their spouse, establishing a business succession plan, and providing significant charitable contributions. It presents various wealth management tools and strategies, such as family limited partnerships and grantor deemed owner trusts, aimed at minimizing estate taxes, ensuring asset protection, and planning for inheritance. The plan emphasizes structured cash flow, efficient wealth transfer, and tax reduction while accommodating Ben and Amanda's philanthropic objectives.