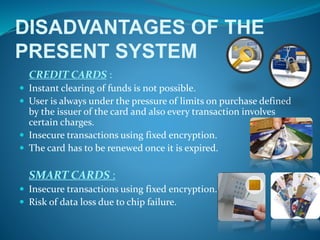

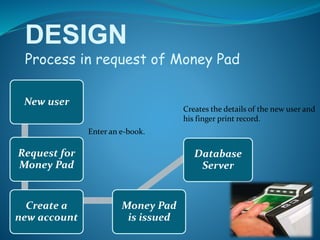

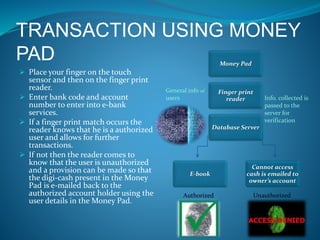

The document introduces the 'money pad,' a biometric system designed to securely carry digital cash as a replacement for traditional payment methods like credit cards and smart cards. It details the advantages and disadvantages of the money pad, including its high security and potential for e-banking transactions, while also noting issues such as the requirement for additional sensors and the risk of injury affecting fingerprint recognition. The conclusion emphasizes the need for features like instant fund clearing and secure transactions to ensure widespread acceptance of digital currency systems.