According to AdamSmith, “Every tax should be

designed to take as little money as possible out

of people’s pockets while yet contributing to

the public treasury of the state.”

6.

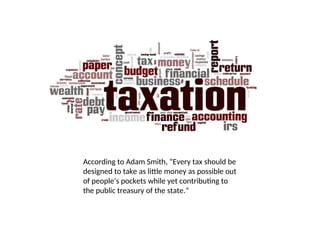

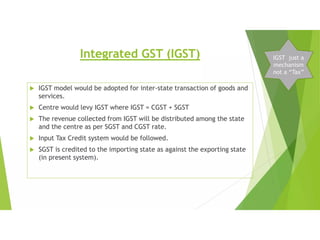

How to knowwhen SGST, CGST or IGST is applicable?

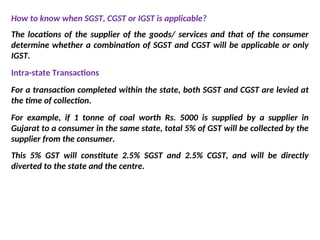

The locations of the supplier of the goods/ services and that of the consumer

determine whether a combination of SGST and CGST will be applicable or only

IGST.

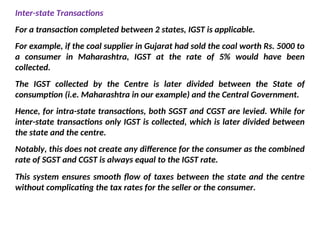

Intra-state Transactions

For a transaction completed within the state, both SGST and CGST are levied at

the time of collection.

For example, if 1 tonne of coal worth Rs. 5000 is supplied by a supplier in

Gujarat to a consumer in the same state, total 5% of GST will be collected by the

supplier from the consumer.

This 5% GST will constitute 2.5% SGST and 2.5% CGST, and will be directly

diverted to the state and the centre.

7.

Inter-state Transactions

For atransaction completed between 2 states, IGST is applicable.

For example, if the coal supplier in Gujarat had sold the coal worth Rs. 5000 to

a consumer in Maharashtra, IGST at the rate of 5% would have been

collected.

The IGST collected by the Centre is later divided between the State of

consumption (i.e. Maharashtra in our example) and the Central Government.

Hence, for intra-state transactions, both SGST and CGST are levied. While for

inter-state transactions only IGST is collected, which is later divided between

the state and the centre.

Notably, this does not create any difference for the consumer as the combined

rate of SGST and CGST is always equal to the IGST rate.

This system ensures smooth flow of taxes between the state and the centre

without complicating the tax rates for the seller or the consumer.

8.

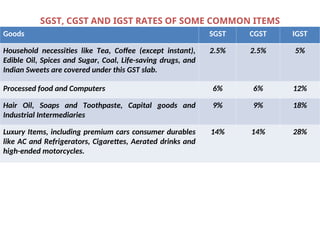

Goods SGST CGSTIGST

Household necessities like Tea, Coffee (except instant),

Edible Oil, Spices and Sugar, Coal, Life-saving drugs, and

Indian Sweets are covered under this GST slab.

2.5% 2.5% 5%

Processed food and Computers 6% 6% 12%

Hair Oil, Soaps and Toothpaste, Capital goods and

Industrial Intermediaries

9% 9% 18%

Luxury Items, including premium cars consumer durables

like AC and Refrigerators, Cigarettes, Aerated drinks and

high-ended motorcycles.

14% 14% 28%

SGST, CGST AND IGST RATES OF SOME COMMON ITEMS

9.

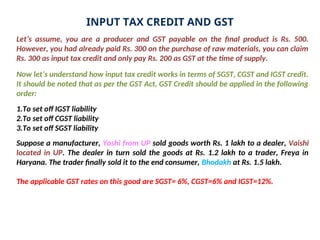

INPUT TAX CREDITAND GST

Let’s assume, you are a producer and GST payable on the final product is Rs. 500.

However, you had already paid Rs. 300 on the purchase of raw materials, you can claim

Rs. 300 as input tax credit and only pay Rs. 200 as GST at the time of supply.

Now let’s understand how input tax credit works in terms of SGST, CGST and IGST credit.

It should be noted that as per the GST Act, GST Credit should be applied in the following

order:

1.To set off IGST liability

2.To set off CGST liability

3.To set off SGST liability

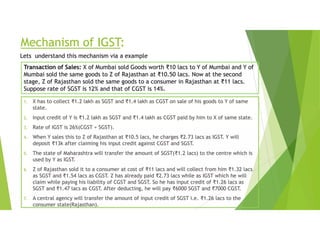

Suppose a manufacturer, Yoshi from UP sold goods worth Rs. 1 lakh to a dealer, Vaishi

located in UP. The dealer in turn sold the goods at Rs. 1.2 lakh to a trader, Freya in

Haryana. The trader finally sold it to the end consumer, Bhodakh at Rs. 1.5 lakh.

The applicable GST rates on this good are SGST= 6%, CGST=6% and IGST=12%.

10.

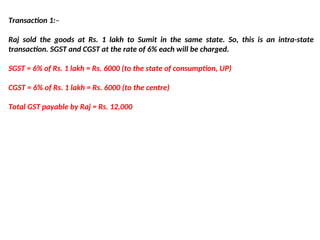

Transaction 1:–

Raj soldthe goods at Rs. 1 lakh to Sumit in the same state. So, this is an intra-state

transaction. SGST and CGST at the rate of 6% each will be charged.

SGST = 6% of Rs. 1 lakh = Rs. 6000 (to the state of consumption, UP)

CGST = 6% of Rs. 1 lakh = Rs. 6000 (to the centre)

Total GST payable by Raj = Rs. 12,000

11.

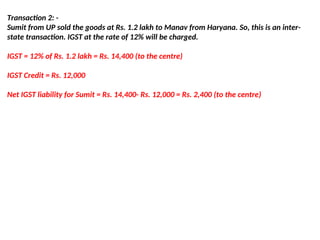

Transaction 2: -

Sumitfrom UP sold the goods at Rs. 1.2 lakh to Manav from Haryana. So, this is an inter-

state transaction. IGST at the rate of 12% will be charged.

IGST = 12% of Rs. 1.2 lakh = Rs. 14,400 (to the centre)

IGST Credit = Rs. 12,000

Net IGST liability for Sumit = Rs. 14,400- Rs. 12,000 = Rs. 2,400 (to the centre)

12.

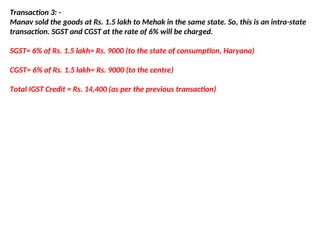

Transaction 3: -

Manavsold the goods at Rs. 1.5 lakh to Mehak in the same state. So, this is an intra-state

transaction. SGST and CGST at the rate of 6% will be charged.

SGST= 6% of Rs. 1.5 lakh= Rs. 9000 (to the state of consumption, Haryana)

CGST= 6% of Rs. 1.5 lakh= Rs. 9000 (to the centre)

Total IGST Credit = Rs. 14,400 (as per the previous transaction)

13.

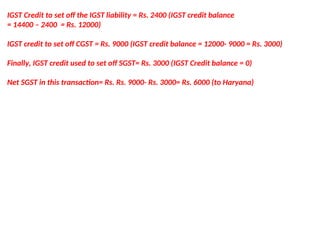

IGST Credit toset off the IGST liability = Rs. 2400 (IGST credit balance

= 14400 – 2400 = Rs. 12000)

IGST credit to set off CGST = Rs. 9000 (IGST credit balance = 12000- 9000 = Rs. 3000)

Finally, IGST credit used to set off SGST= Rs. 3000 (IGST Credit balance = 0)

Net SGST in this transaction= Rs. Rs. 9000- Rs. 3000= Rs. 6000 (to Haryana)

14.

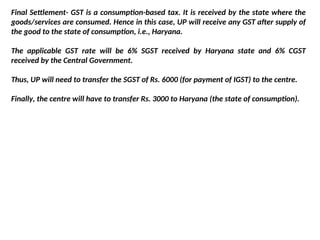

Final Settlement- GSTis a consumption-based tax. It is received by the state where the

goods/services are consumed. Hence in this case, UP will receive any GST after supply of

the good to the state of consumption, i.e., Haryana.

The applicable GST rate will be 6% SGST received by Haryana state and 6% CGST

received by the Central Government.

Thus, UP will need to transfer the SGST of Rs. 6000 (for payment of IGST) to the centre.

Finally, the centre will have to transfer Rs. 3000 to Haryana (the state of consumption).

15.

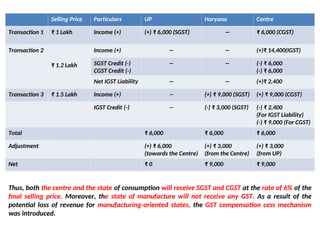

Selling Price ParticularsUP Haryana Centre

Transaction 1 ₹ 1 Lakh Income (+) (+) ₹ 6,000 (SGST) -- ₹ 6,000 (CGST)

Transaction 2

₹ 1.2 Lakh

Income (+) -- -- (+)₹ 14,400(IGST)

SGST Credit (-)

CGST Credit (-)

-- -- (-) ₹ 6,000

(-) ₹ 6,000

Net IGST Liability -- -- (+)₹ 2,400

Transaction 3 ₹ 1.5 Lakh Income (+) -- (+) ₹ 9,000 (SGST) (+) ₹ 9,000 (CGST)

IGST Credit (-) -- (-) ₹ 3,000 (SGST) (-) ₹ 2,400

(For IGST Liability)

(-) ₹ 9,000 (For CGST)

Total ₹ 6,000 ₹ 6,000 ₹ 6,000

Adjustment (+) ₹ 6,000

(towards the Centre)

(+) ₹ 3,000

(from the Centre)

(+) ₹ 3,000

(from UP)

Net ₹ 0 ₹ 9,000 ₹ 9,000

Thus, both the centre and the state of consumption will receive SGST and CGST at the rate of 6% of the

final selling price. Moreover, the state of manufacture will not receive any GST. As a result of the

potential loss of revenue for manufacturing-oriented states, the GST compensation cess mechanism

was introduced.

18.

CAPEX:

Capital expenditure isthe money spent on acquiring fixed assets like new

equipment, machinery, land, plant etc. and intangible assets such as patents or

licenses, upgrading an existing asset, repairing an asset or repayment of loan.

Deregulation:

It is the elimination or removal of government controls over a particular industry or

sector. Deregulation opens up the industry to more players and makes it more

competitive.

Four ways that your organization can diversify its supply chain:

1.Invest In Domestic Sourcing. Forming local partnerships is more important today

than ever before.

2.Expand Your Supplier Base. Resilient supply chains are flexible supply chains.

3.Hedge Commodities.

4.Streamline Operational Measures.

The Insolvency and Bankruptcy Code (IBC) 2015:

It is a law in India that governs insolvency and bankruptcy proceedings for

companies, partnership firms, and individuals. The IBC was first introduced in Lok

Sabha in December 2015 and passed in May 2016.

19.

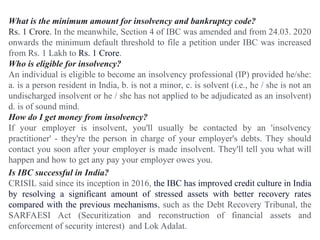

What is theminimum amount for insolvency and bankruptcy code?

Rs. 1 Crore. In the meanwhile, Section 4 of IBC was amended and from 24.03. 2020

onwards the minimum default threshold to file a petition under IBC was increased

from Rs. 1 Lakh to Rs. 1 Crore.

Who is eligible for insolvency?

An individual is eligible to become an insolvency professional (IP) provided he/she:

a. is a person resident in India, b. is not a minor, c. is solvent (i.e., he / she is not an

undischarged insolvent or he / she has not applied to be adjudicated as an insolvent)

d. is of sound mind.

How do I get money from insolvency?

If your employer is insolvent, you'll usually be contacted by an 'insolvency

practitioner' - they're the person in charge of your employer's debts. They should

contact you soon after your employer is made insolvent. They'll tell you what will

happen and how to get any pay your employer owes you.

Is IBC successful in India?

CRISIL said since its inception in 2016, the IBC has improved credit culture in India

by resolving a significant amount of stressed assets with better recovery rates

compared with the previous mechanisms, such as the Debt Recovery Tribunal, the

SARFAESI Act (Securitization and reconstruction of financial assets and

enforcement of security interest) and Lok Adalat.

30.

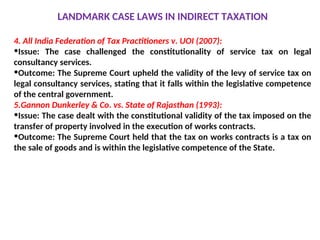

LANDMARK CASE LAWSIN INDIRECT TAXATION

1. M/s BSNL vs. UOI (2006):

•Issue: The case revolved around the service tax liability on the receipts of the

BSNL (Bharat Sanchar Nigam Limited) for providing telecom services.

•Outcome: The Supreme Court held that the receipts of BSNL are not subject to

service tax, as the activities performed by it do not fall within the definition of

"commercial or industrial construction service."

2. Union of India v. Bombay Tyre International Ltd. (1984):

•Issue: The case dealt with the question of whether a sale was completed within

the territory of a single state or involved inter-state sales.

•Outcome: The Supreme Court clarified the principles governing inter-state sales

and the concept of the "sale of goods" under the Central Sales Tax Act, 1956.

3. J.K. Synthetics Ltd. v. Commercial Taxes Officer (1994):

•Issue: The case discussed the scope of the term "manufacture" under the Central

Excise Act, 1944.

•Outcome: The Supreme Court held that the mere cutting of raw materials into

suitable sizes for being used in the manufacture of final products does not amount

to manufacture under the Act.

31.

LANDMARK CASE LAWSIN INDIRECT TAXATION

4. All India Federation of Tax Practitioners v. UOI (2007):

•Issue: The case challenged the constitutionality of service tax on legal

consultancy services.

•Outcome: The Supreme Court upheld the validity of the levy of service tax on

legal consultancy services, stating that it falls within the legislative competence

of the central government.

5.Gannon Dunkerley & Co. vs. State of Rajasthan (1993):

•Issue: The case dealt with the constitutional validity of the tax imposed on the

transfer of property involved in the execution of works contracts.

•Outcome: The Supreme Court held that the tax on works contracts is a tax on

the sale of goods and is within the legislative competence of the State.

32.

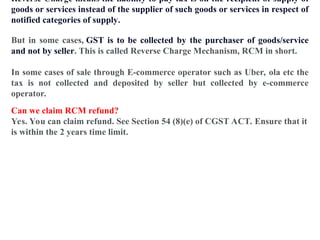

Reverse Charge meansthe liability to pay tax is on the recipient of supply of

goods or services instead of the supplier of such goods or services in respect of

notified categories of supply.

But in some cases, GST is to be collected by the purchaser of goods/service

and not by seller. This is called Reverse Charge Mechanism, RCM in short.

In some cases of sale through E-commerce operator such as Uber, ola etc the

tax is not collected and deposited by seller but collected by e-commerce

operator.

Can we claim RCM refund?

Yes. You can claim refund. See Section 54 (8)(e) of CGST ACT. Ensure that it

is within the 2 years time limit.