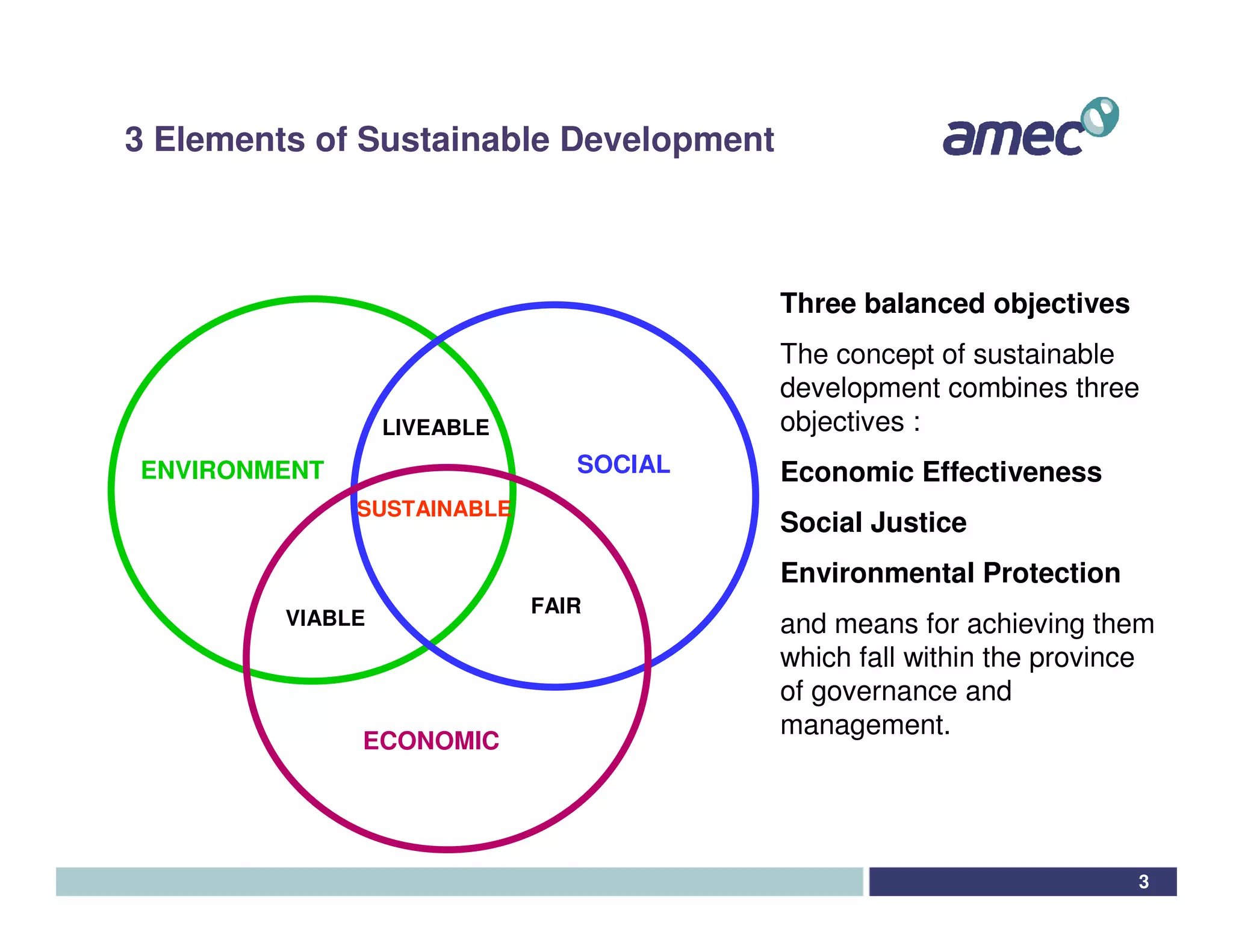

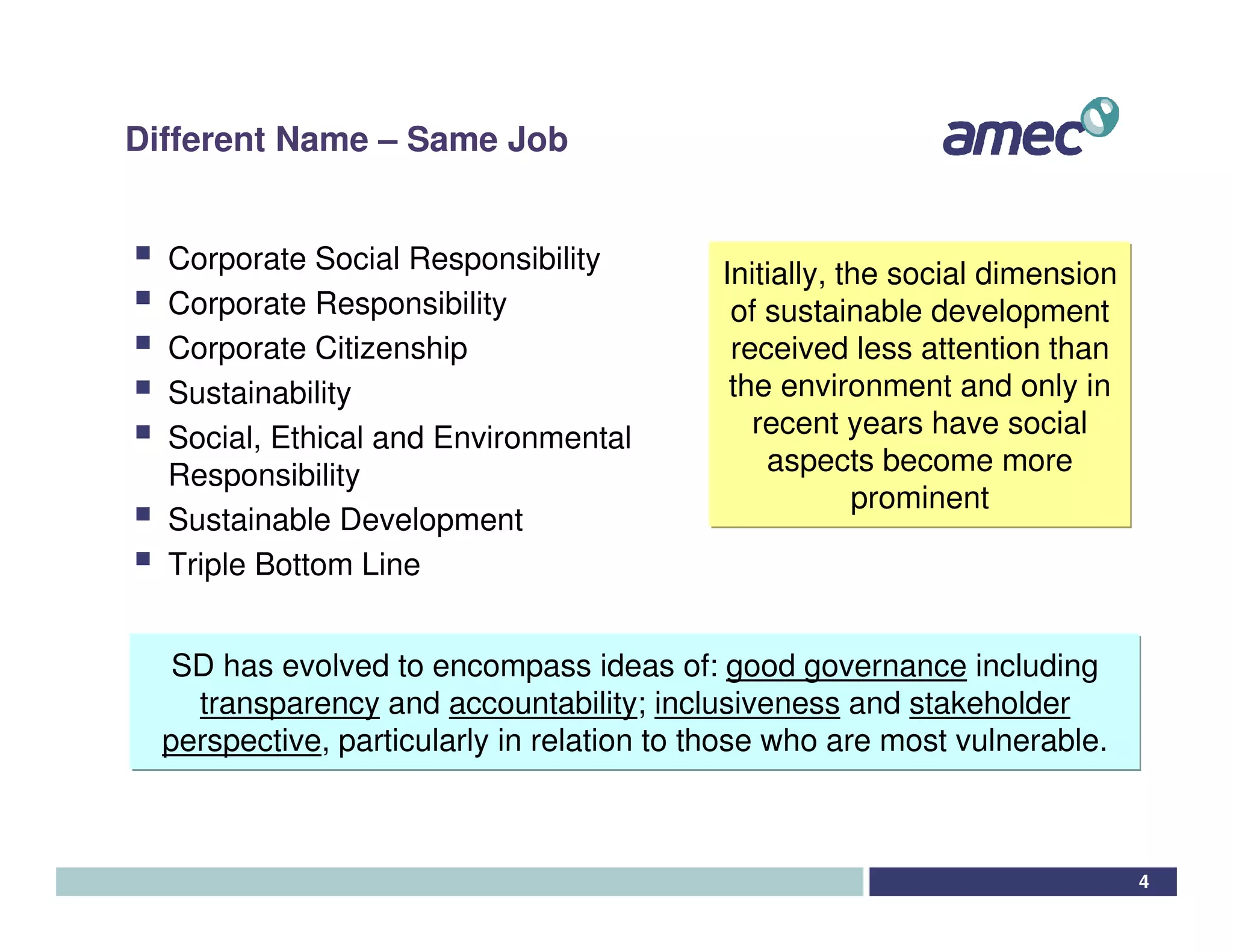

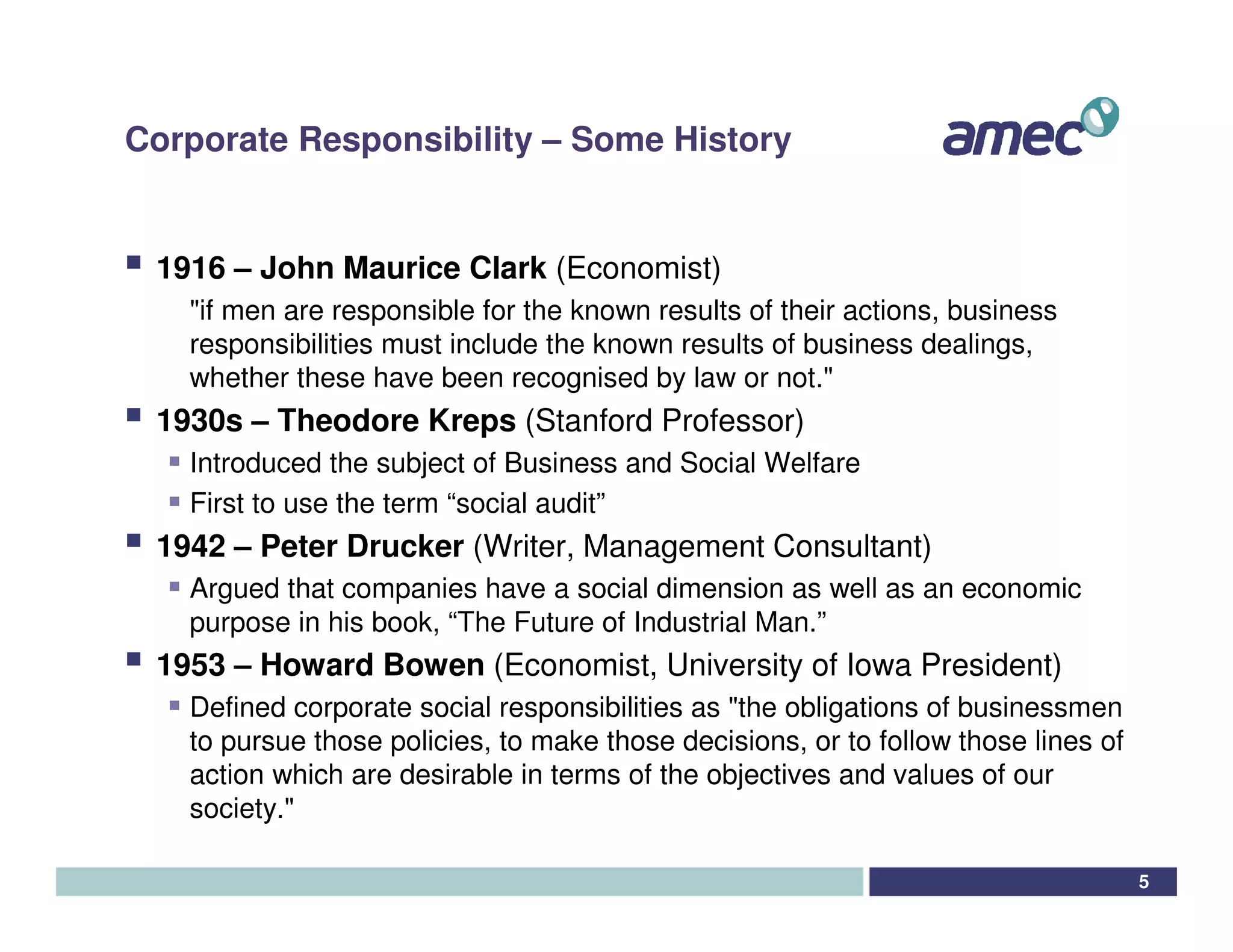

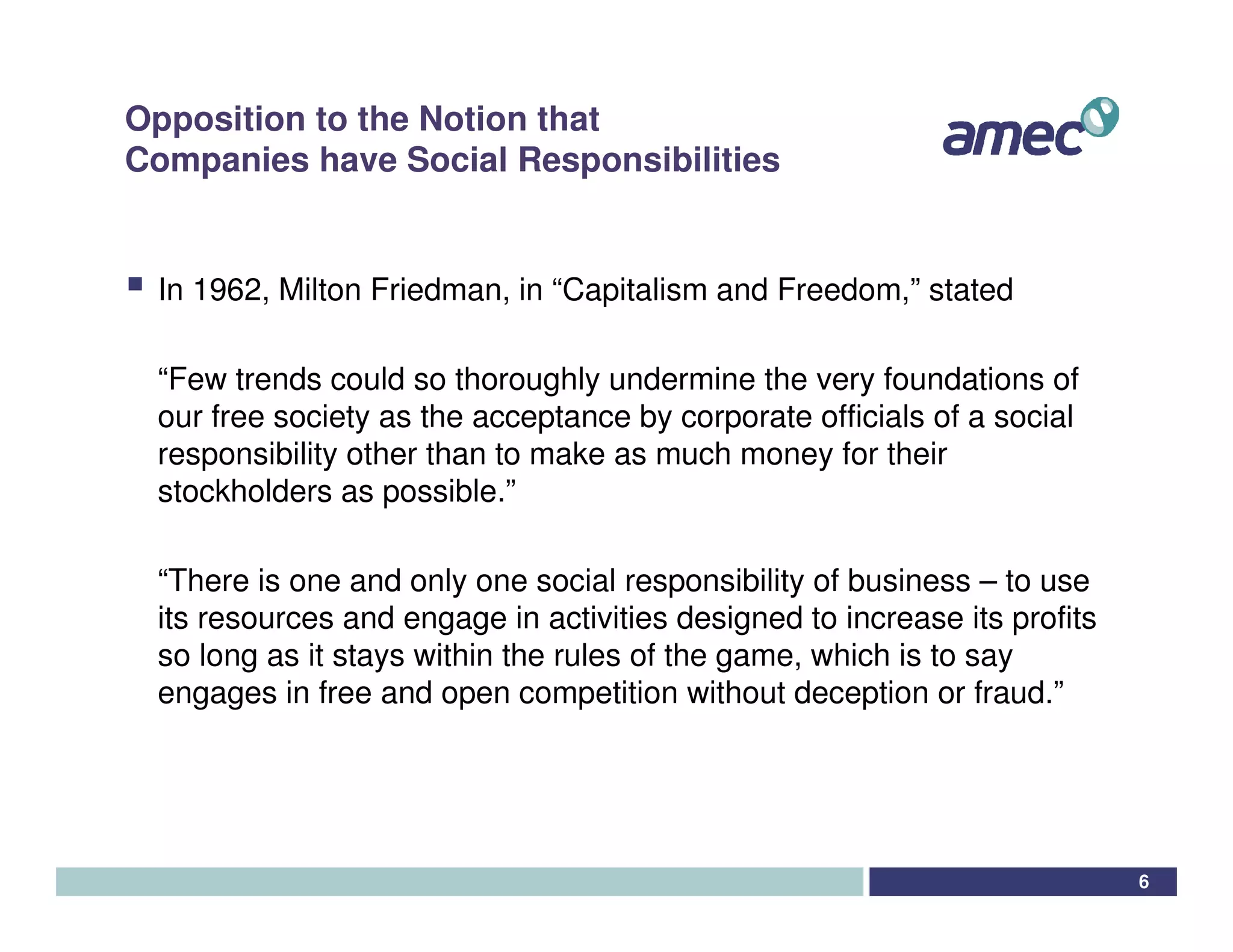

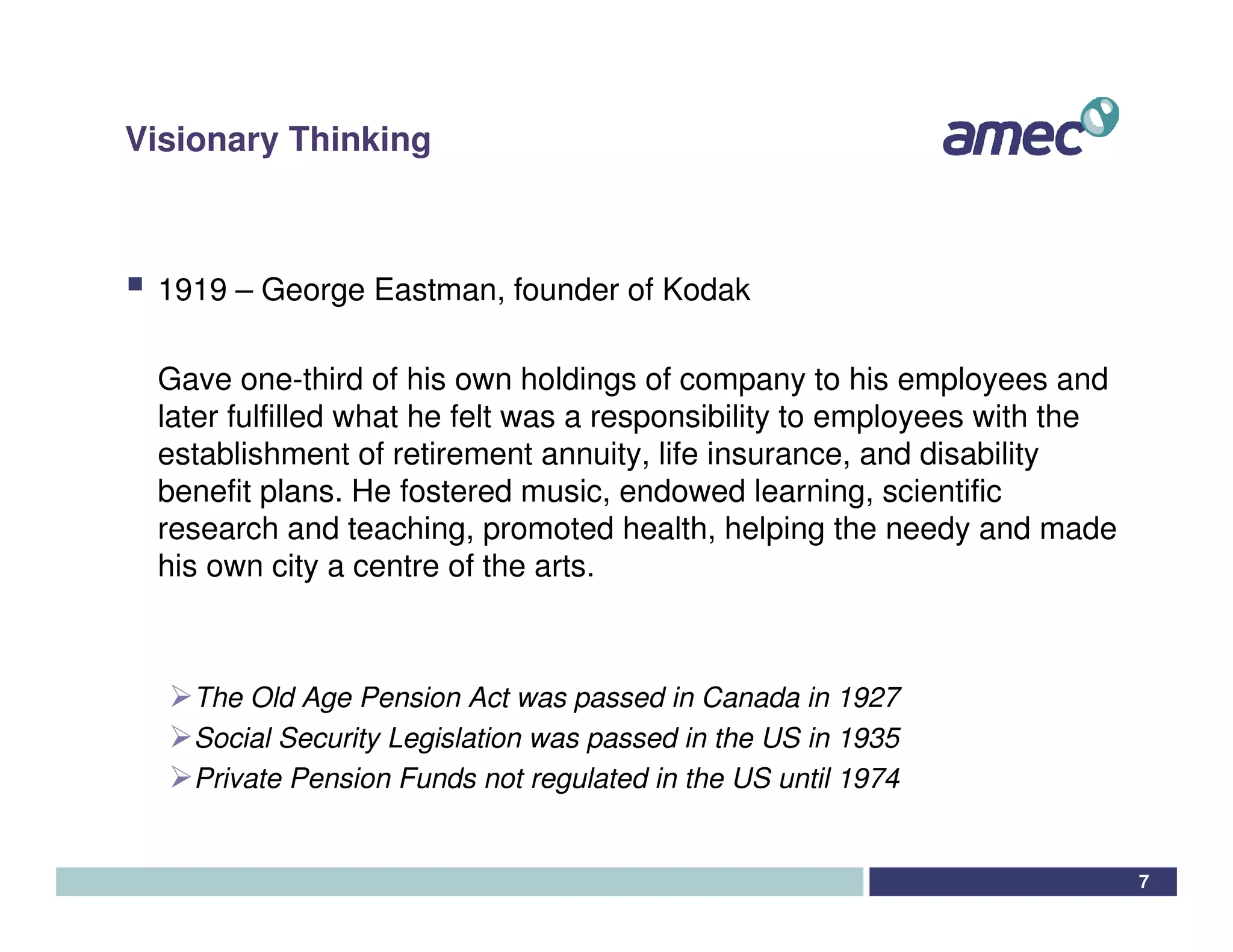

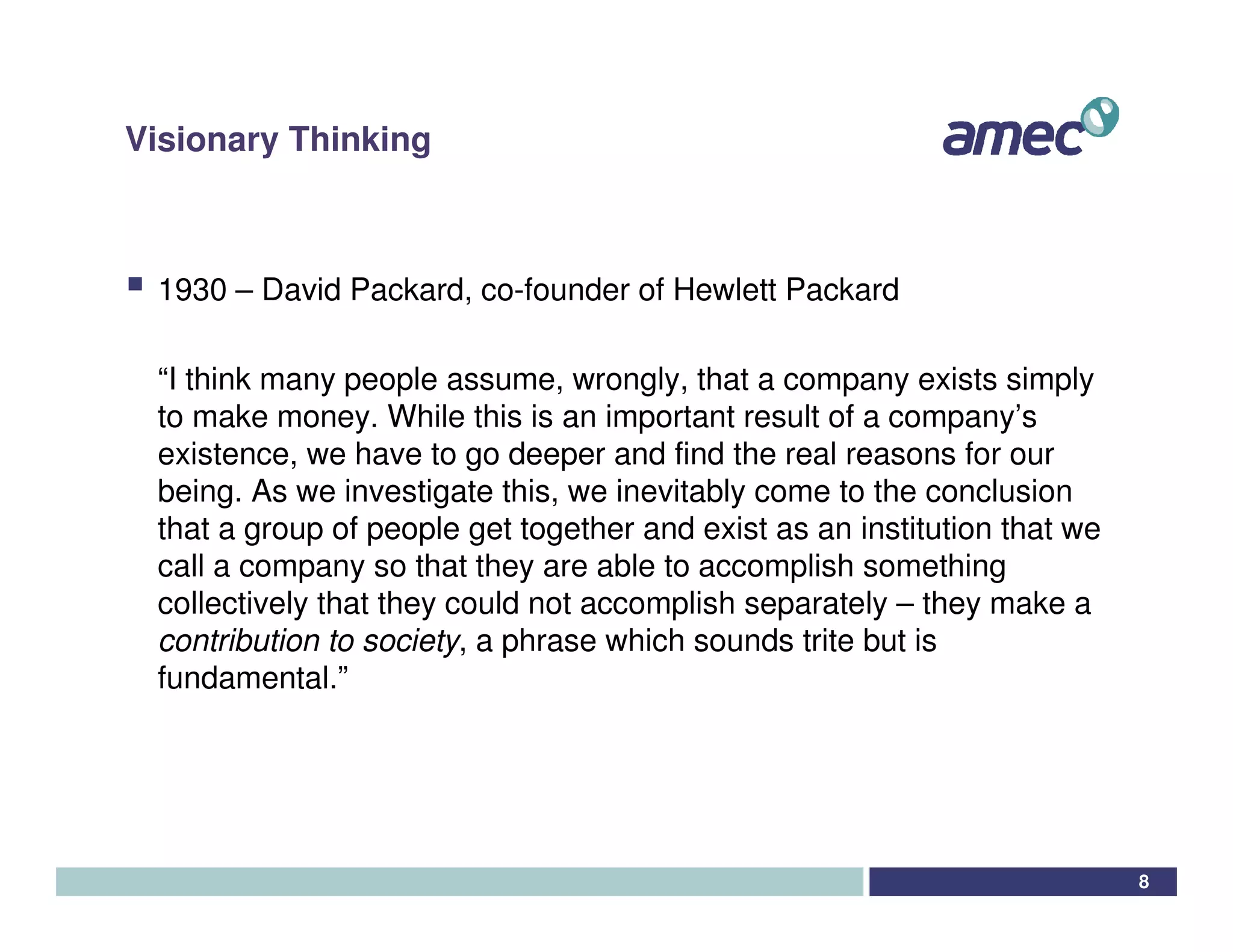

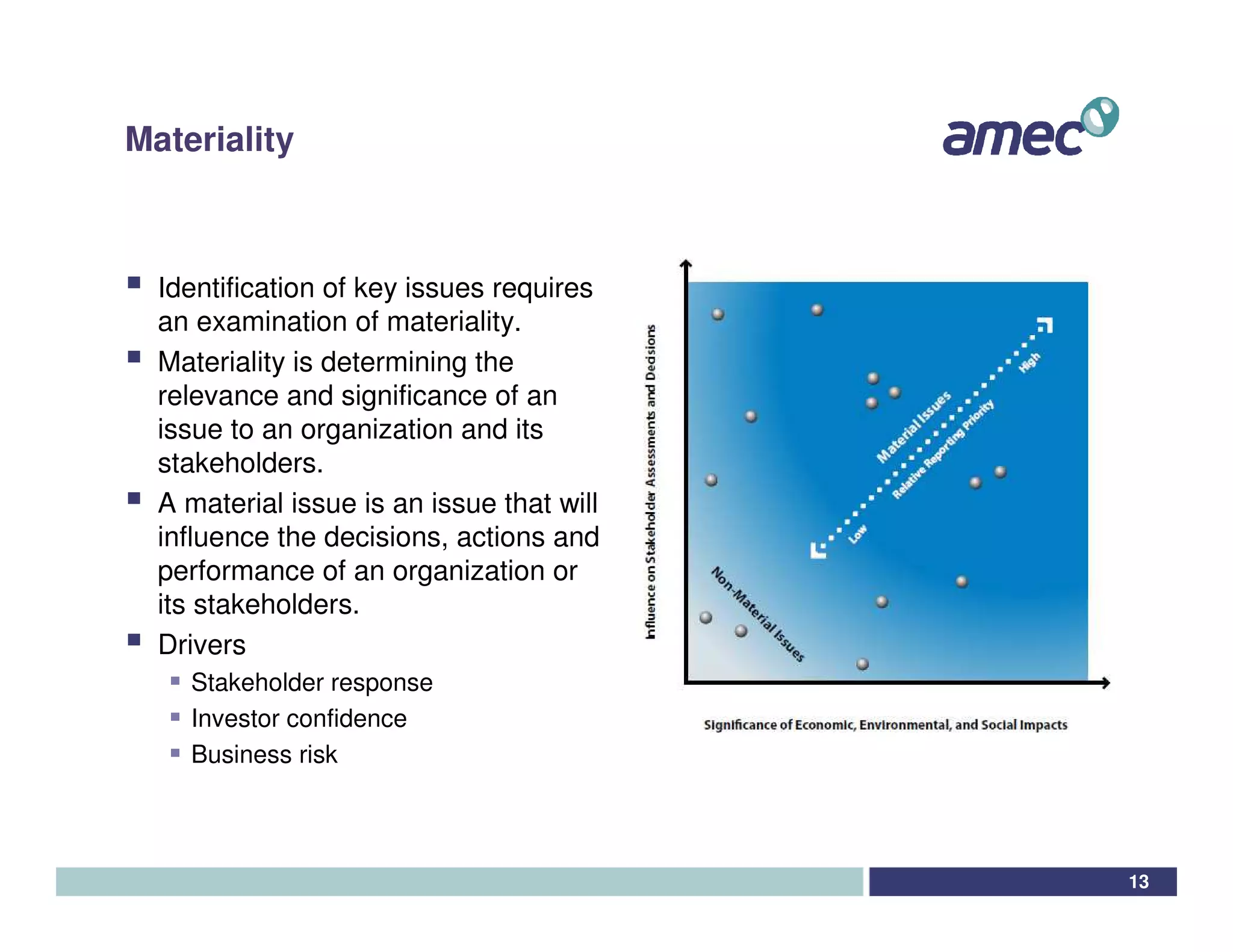

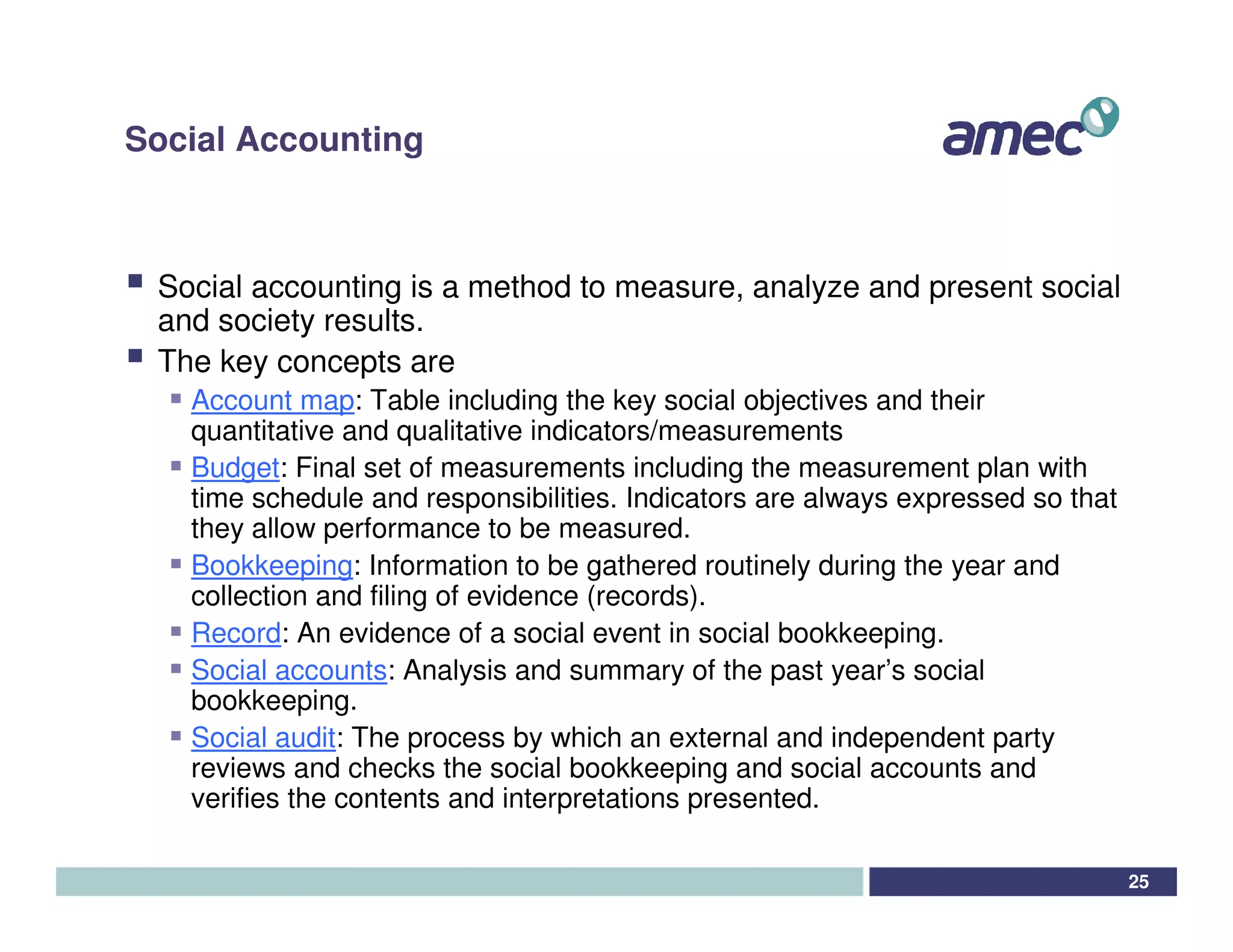

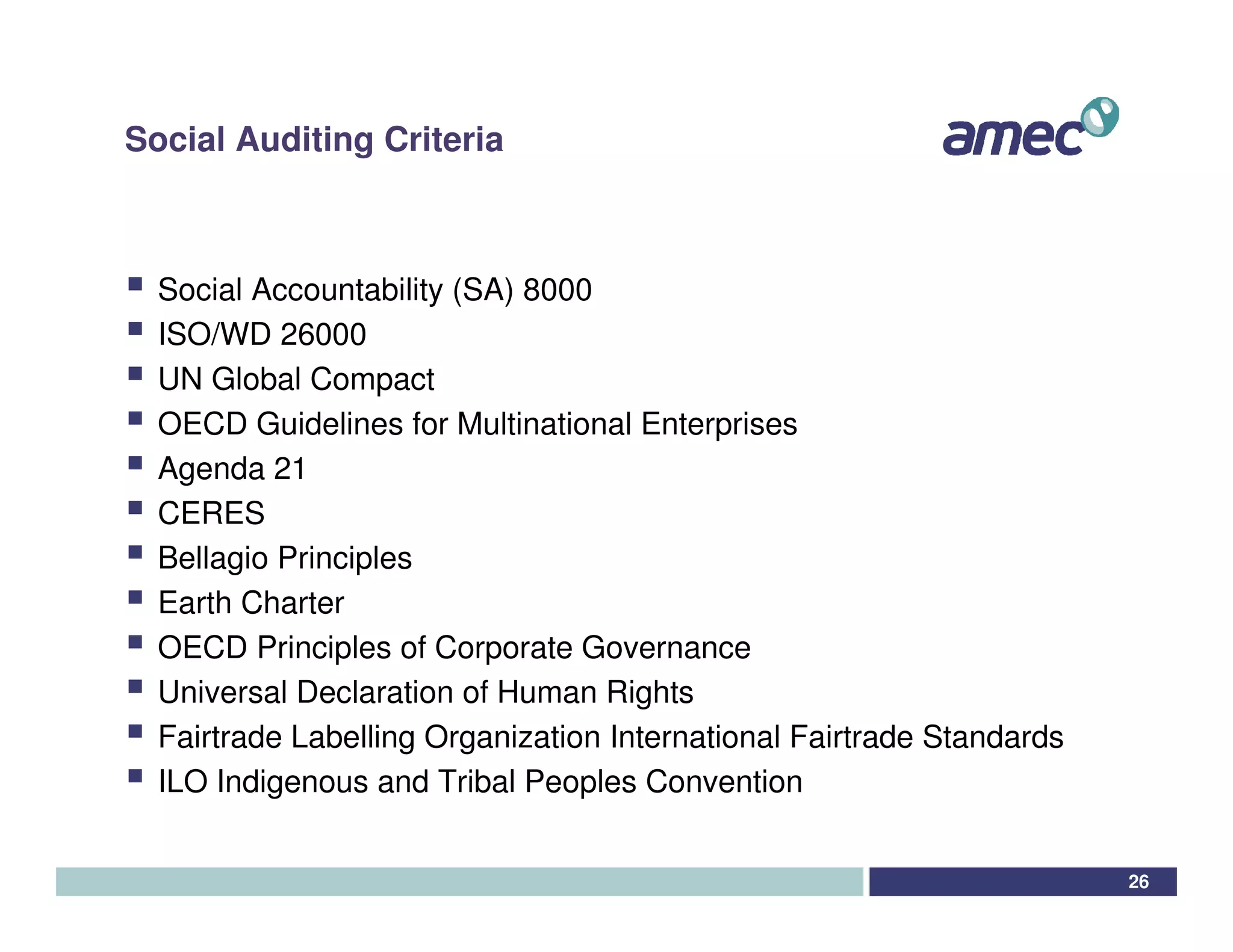

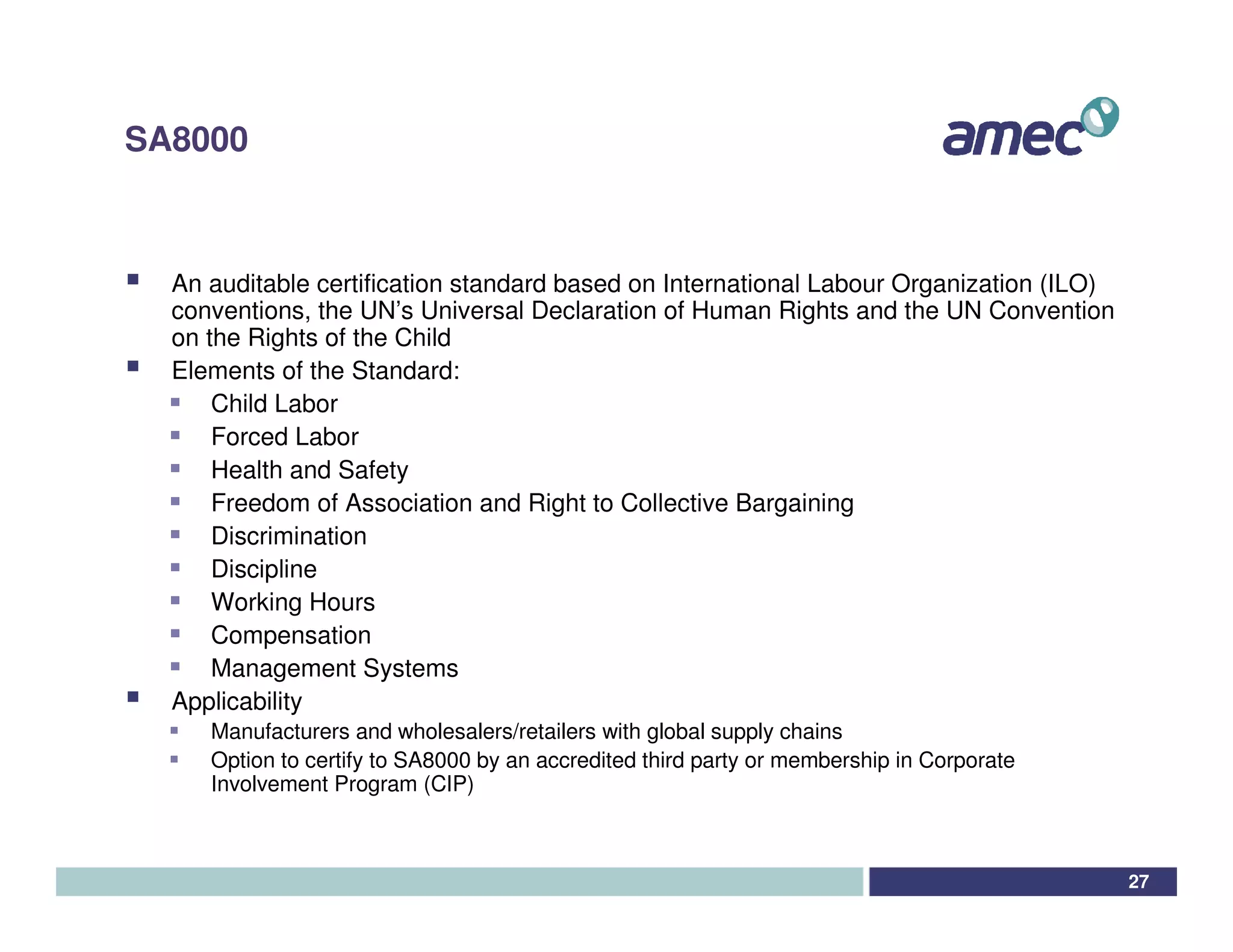

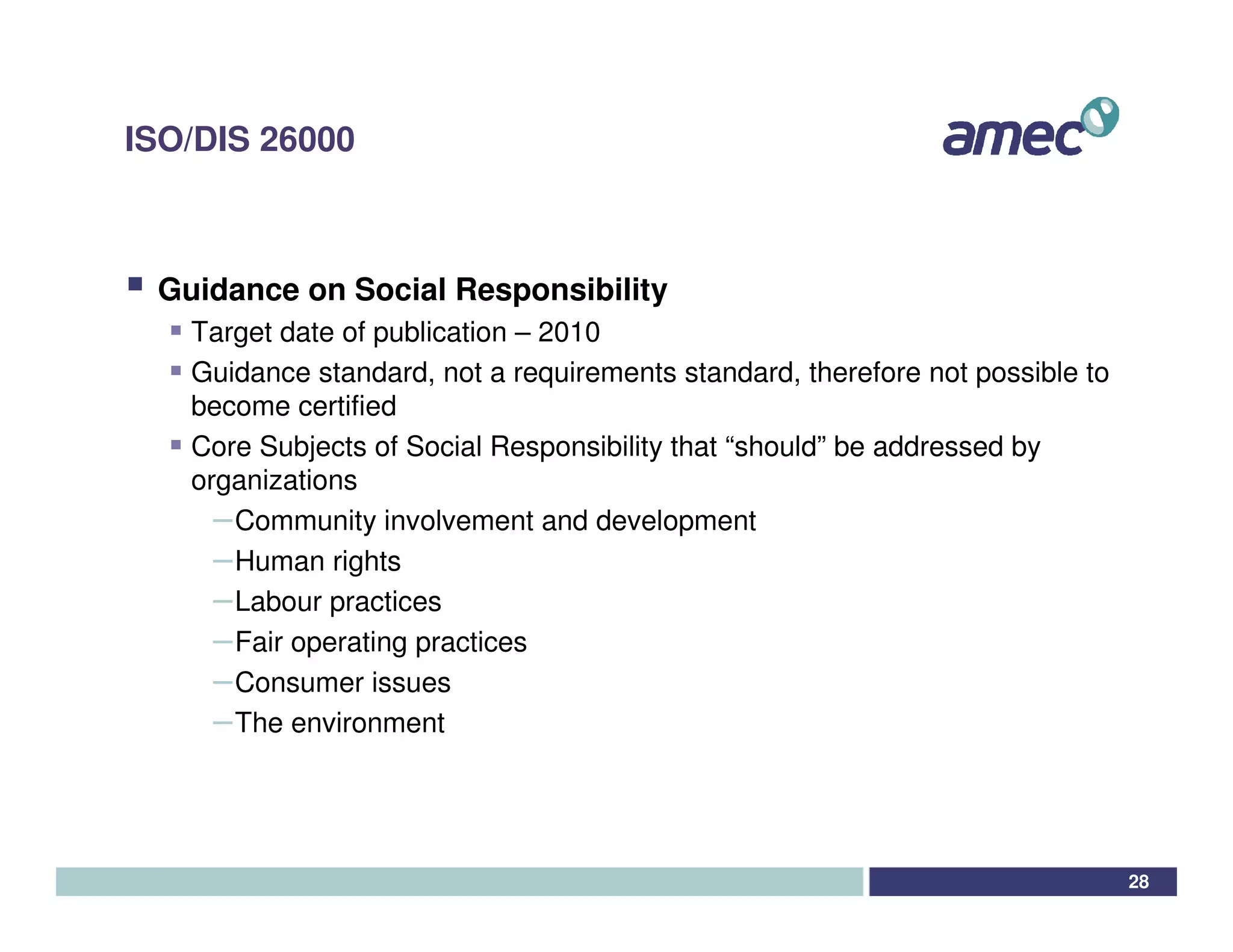

This document provides an overview of social auditing and corporate responsibility. It discusses the brief history of corporate responsibility programs and how they have developed over time. It then explains the key principles, criteria, and process involved in social auditing for corporations. The document emphasizes that determining material issues and prioritizing them is an important part of social auditing.