This document is a Michigan Department of Treasury form for calculating penalties and interest for underpayment of estimated income tax for the 2008 tax year. It contains instructions for completing the form, which has sections to calculate the estimated tax required for the year, figure any underpayments per payment period, and determine the total interest and penalties owed. Key details include calculating the estimated tax as a percentage of the prior or current year's tax, accounting for uneven income throughout the year using annualized amounts, and applying interest rates by payment period to any underpayments.

Unveiling the Secrets How Does Generative AI Work.pdfSam H

At its core, generative artificial intelligence relies on the concept of generative models, which serve as engines that churn out entirely new data resembling their training data. It is like a sculptor who has studied so many forms found in nature and then uses this knowledge to create sculptures from his imagination that have never been seen before anywhere else. If taken to cyberspace, gans work almost the same way.

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

VAT Registration Outlined In UAE: Benefits and Requirementsuae taxgpt

Vat Registration is a legal obligation for businesses meeting the threshold requirement, helping companies avoid fines and ramifications. Contact now!

https://viralsocialtrends.com/vat-registration-outlined-in-uae/

Affordable Stationery Printing Services in Jaipur | Navpack n PrintNavpack & Print

Looking for professional printing services in Jaipur? Navpack n Print offers high-quality and affordable stationery printing for all your business needs. Stand out with custom stationery designs and fast turnaround times. Contact us today for a quote!

LA HUG - Video Testimonials with Chynna Morgan - June 2024Lital Barkan

Have you ever heard that user-generated content or video testimonials can take your brand to the next level? We will explore how you can effectively use video testimonials to leverage and boost your sales, content strategy, and increase your CRM data.🤯

We will dig deeper into:

1. How to capture video testimonials that convert from your audience 🎥

2. How to leverage your testimonials to boost your sales 💲

3. How you can capture more CRM data to understand your audience better through video testimonials. 📊

Kseniya Leshchenko: Shared development support service model as the way to ma...Lviv Startup Club

Kseniya Leshchenko: Shared development support service model as the way to make small projects with small budgets profitable for the company (UA)

Kyiv PMDay 2024 Summer

Website – www.pmday.org

Youtube – https://www.youtube.com/startuplviv

FB – https://www.facebook.com/pmdayconference

Memorandum Of Association Constitution of Company.pptseri bangash

www.seribangash.com

A Memorandum of Association (MOA) is a legal document that outlines the fundamental principles and objectives upon which a company operates. It serves as the company's charter or constitution and defines the scope of its activities. Here's a detailed note on the MOA:

Contents of Memorandum of Association:

Name Clause: This clause states the name of the company, which should end with words like "Limited" or "Ltd." for a public limited company and "Private Limited" or "Pvt. Ltd." for a private limited company.

https://seribangash.com/article-of-association-is-legal-doc-of-company/

Registered Office Clause: It specifies the location where the company's registered office is situated. This office is where all official communications and notices are sent.

Objective Clause: This clause delineates the main objectives for which the company is formed. It's important to define these objectives clearly, as the company cannot undertake activities beyond those mentioned in this clause.

www.seribangash.com

Liability Clause: It outlines the extent of liability of the company's members. In the case of companies limited by shares, the liability of members is limited to the amount unpaid on their shares. For companies limited by guarantee, members' liability is limited to the amount they undertake to contribute if the company is wound up.

https://seribangash.com/promotors-is-person-conceived-formation-company/

Capital Clause: This clause specifies the authorized capital of the company, i.e., the maximum amount of share capital the company is authorized to issue. It also mentions the division of this capital into shares and their respective nominal value.

Association Clause: It simply states that the subscribers wish to form a company and agree to become members of it, in accordance with the terms of the MOA.

Importance of Memorandum of Association:

Legal Requirement: The MOA is a legal requirement for the formation of a company. It must be filed with the Registrar of Companies during the incorporation process.

Constitutional Document: It serves as the company's constitutional document, defining its scope, powers, and limitations.

Protection of Members: It protects the interests of the company's members by clearly defining the objectives and limiting their liability.

External Communication: It provides clarity to external parties, such as investors, creditors, and regulatory authorities, regarding the company's objectives and powers.

https://seribangash.com/difference-public-and-private-company-law/

Binding Authority: The company and its members are bound by the provisions of the MOA. Any action taken beyond its scope may be considered ultra vires (beyond the powers) of the company and therefore void.

Amendment of MOA:

While the MOA lays down the company's fundamental principles, it is not entirely immutable. It can be amended, but only under specific circumstances and in compliance with legal procedures. Amendments typically require shareholder

Discover the innovative and creative projects that highlight my journey throu...dylandmeas

Discover the innovative and creative projects that highlight my journey through Full Sail University. Below, you’ll find a collection of my work showcasing my skills and expertise in digital marketing, event planning, and media production.

RMD24 | Retail media: hoe zet je dit in als je geen AH of Unilever bent? Heid...BBPMedia1

Grote partijen zijn al een tijdje onderweg met retail media. Ondertussen worden in dit domein ook de kansen zichtbaar voor andere spelers in de markt. Maar met die kansen ontstaan ook vragen: Zelf retail media worden of erop adverteren? In welke fase van de funnel past het en hoe integreer je het in een mediaplan? Wat is nu precies het verschil met marketplaces en Programmatic ads? In dit half uur beslechten we de dilemma's en krijg je antwoorden op wanneer het voor jou tijd is om de volgende stap te zetten.

Buy Verified PayPal Account | Buy Google 5 Star Reviewsusawebmarket

Buy Verified PayPal Account

Looking to buy verified PayPal accounts? Discover 7 expert tips for safely purchasing a verified PayPal account in 2024. Ensure security and reliability for your transactions.

PayPal Services Features-

🟢 Email Access

🟢 Bank Added

🟢 Card Verified

🟢 Full SSN Provided

🟢 Phone Number Access

🟢 Driving License Copy

🟢 Fasted Delivery

Client Satisfaction is Our First priority. Our services is very appropriate to buy. We assume that the first-rate way to purchase our offerings is to order on the website. If you have any worry in our cooperation usually You can order us on Skype or Telegram.

24/7 Hours Reply/Please Contact

usawebmarketEmail: support@usawebmarket.com

Skype: usawebmarket

Telegram: @usawebmarket

WhatsApp: +1(218) 203-5951

USA WEB MARKET is the Best Verified PayPal, Payoneer, Cash App, Skrill, Neteller, Stripe Account and SEO, SMM Service provider.100%Satisfection granted.100% replacement Granted.

Digital Transformation and IT Strategy Toolkit and TemplatesAurelien Domont, MBA

This Digital Transformation and IT Strategy Toolkit was created by ex-McKinsey, Deloitte and BCG Management Consultants, after more than 5,000 hours of work. It is considered the world's best & most comprehensive Digital Transformation and IT Strategy Toolkit. It includes all the Frameworks, Best Practices & Templates required to successfully undertake the Digital Transformation of your organization and define a robust IT Strategy.

Editable Toolkit to help you reuse our content: 700 Powerpoint slides | 35 Excel sheets | 84 minutes of Video training

This PowerPoint presentation is only a small preview of our Toolkits. For more details, visit www.domontconsulting.com

Premium MEAN Stack Development Solutions for Modern BusinessesSynapseIndia

Stay ahead of the curve with our premium MEAN Stack Development Solutions. Our expert developers utilize MongoDB, Express.js, AngularJS, and Node.js to create modern and responsive web applications. Trust us for cutting-edge solutions that drive your business growth and success.

Know more: https://www.synapseindia.com/technology/mean-stack-development-company.html

Enterprise Excellence is Inclusive Excellence.pdfKaiNexus

Enterprise excellence and inclusive excellence are closely linked, and real-world challenges have shown that both are essential to the success of any organization. To achieve enterprise excellence, organizations must focus on improving their operations and processes while creating an inclusive environment that engages everyone. In this interactive session, the facilitator will highlight commonly established business practices and how they limit our ability to engage everyone every day. More importantly, though, participants will likely gain increased awareness of what we can do differently to maximize enterprise excellence through deliberate inclusion.

What is Enterprise Excellence?

Enterprise Excellence is a holistic approach that's aimed at achieving world-class performance across all aspects of the organization.

What might I learn?

A way to engage all in creating Inclusive Excellence. Lessons from the US military and their parallels to the story of Harry Potter. How belt systems and CI teams can destroy inclusive practices. How leadership language invites people to the party. There are three things leaders can do to engage everyone every day: maximizing psychological safety to create environments where folks learn, contribute, and challenge the status quo.

Who might benefit? Anyone and everyone leading folks from the shop floor to top floor.

Dr. William Harvey is a seasoned Operations Leader with extensive experience in chemical processing, manufacturing, and operations management. At Michelman, he currently oversees multiple sites, leading teams in strategic planning and coaching/practicing continuous improvement. William is set to start his eighth year of teaching at the University of Cincinnati where he teaches marketing, finance, and management. William holds various certifications in change management, quality, leadership, operational excellence, team building, and DiSC, among others.

1. Reset Form

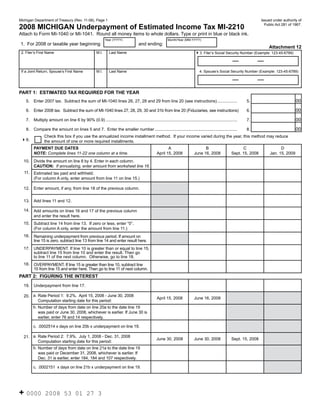

Michigan Department of Treasury (Rev. 11-08), Page 1 Issued under authority of

2008 MICHIGAN Underpayment of Estimated Income Tax MI-2210 Public Act 281 of 1967.

Attach to Form MI-1040 or MI-1041. Round all money items to whole dollars. Type or print in blue or black ink.

Year (YYYY) Month/Year (MM-YYYY)

1. For 2008 or taxable year beginning: and ending:

Attachment 12

2. Filer’s First Name M.I. Last Name 43. Filer’s Social Security Number (Example: 123-45-6789)

If a Joint Return, Spouse’s First Name M.I. Last Name 4. Spouse’s Social Security Number (Example: 123-45-6789)

PART 1: ESTIMATED TAX REQUIRED FOR THE YEAR

00

5. Enter 2007 tax. Subtract the sum of MI-1040 lines 26, 27, 28 and 29 from line 20 (see instructions) ................. 5.

00

6. Enter 2008 tax. Subtract the sum of MI-1040 lines 27, 28, 29, 30 and 31b from line 20 (Fiduciaries, see instructions) 6.

00

7. Multiply amount on line 6 by 90% (0.9) ................................................................................................................. 7.

00

8. Compare the amount on lines 5 and 7. Enter the smaller number ....................................................................... 8.

Check this box if you use the annualized income installment method. If your income varied during the year, this method may reduce

49. the amount of one or more required installments.

PAYMENT DUE DATES A B C D

April 15, 2008 June 16, 2008 Sept. 15, 2008 Jan. 15, 2009

NOTE: Complete lines 11-22 one column at a time.

10. Divide the amount on line 8 by 4. Enter in each column.

CAUTION: If annualizing, enter amount from worksheet line 16.

11. Estimated tax paid and withheld.

(For column A only, enter amount from line 11 on line 15.)

12. Enter amount, if any, from line 18 of the previous column.

13. Add lines 11 and 12.

14. Add amounts on lines 16 and 17 of the previous column

and enter the result here.

15. Subtract line 14 from line 13. If zero or less, enter “0”.

(For column A only, enter the amount from line 11.)

16. Remaining underpayment from previous period. If amount on

line 15 is zero, subtract line 13 from line 14 and enter result here.

17. UNDERPAYMENT. If line 10 is greater than or equal to line 15,

subtract line 15 from line 10 and enter the result. Then go

to line 11 of the next column. Otherwise, go to line 18.

18. OVERPAYMENT. If line 15 is greater than line 10, subtract line

10 from line 15 and enter here. Then go to line 11 of next column.

PART 2: FIGURING THE INTEREST

19. Underpayment from line 17.

20. a. Rate Period 1: 9.2%. April 15, 2008 - June 30, 2008

April 15, 2008 June 16, 2008

Computation starting date for this period:

b. Number of days from date on line 20a to the date line 19

was paid or June 30, 2008, whichever is earlier. If June 30 is

earlier, enter 76 and 14 respectively.

c. .0002514 x days on line 20b x underpayment on line 19.

21. a. Rate Period 2: 7.9%. July 1, 2008 - Dec. 31, 2008

June 30, 2008 June 30, 2008 Sept. 15, 2008

Computation starting date for this period:

b. Number of days from date on line 21a to the date line 19

was paid or December 31, 2008, whichever is earlier. If

Dec. 31 is earlier, enter 184, 184 and 107 respectively.

c. .0002151 x days on line 21b x underpayment on line 19.

+ 0000 2008 53 01 27 3

2. 2008 MI-2210, Page 2 Filer’s Social Security Number

22. a. Rate Period 3: 6.0%. Jan. 1, 2009 - June 30, 2009

Dec. 31, 2008 Dec. 31, 2008 Dec. 31, 2008 Jan. 15, 2009

Computation starting date for this period:

b. Number of days from date on line 22a to the date line 19

was paid or April 15, 2009, whichever is earlier. If April 15

is earlier, enter 105, 105, 105 and 90 respectively.

c. .0001644 x days on line 22b x underpayment on line 19.

23. Interest. Add amount on lines 20c, 21c and 22c in all columns. Enter the total interest here

00

and on the appropriate line on your MI-1040 or MI-1041 ...................................................................................... 23.

A B C D

PART 3: FIGURING THE PENALTY April 15, 2008 June 16, 2008 Sept. 15, 2008 Jan. 15, 2009

00 00 00 00

24. Underpayment (see instructions)..................................... 24.

% % % %

25. Enter 25% (0.25) or 10% (0.10) (see instructions) .......... 25.

00 00 00 00

26. Multiply amount on line 24 by line 25 .............................. 26.

27. TOTAL PENALTY. Add line 26, columns A through D. Enter total penalty here and in appropriate space

00

on the pay line of your MI-1040 or MI-1041........................................................................................................... 27.

00

28. Add lines 23 and 27. This is your total penalty and interest to be added to your tax due .................................... 28.

This form computes penalty and interest for estimate vouchers to the date of payment or April 15, 2009, whichever is earlier.

Additional penalty and interest for late filing accrues on your annual return from April 15 to the date of payment.

ANNUALIZED INCOME WORKSHEET

Complete one column at a time. Line numbers refer to this worksheet unless another form is listed.

Estates and trusts: Use the following period ending dates: 2/29/08, 4/30/08, 7/31/08 and 11/30/08.

Do not use the dates in the column headings below.

B C D

A

First 8 months 12 months

First 3 months First 5 months

1-1 to 8-31-08 1-1 to 12-31-08

1-1 to 3-31-08 1-1 to 5-31-08

1. Enter total income subject to tax (reported on 2008

MI-1040, line 14) that is attributable to each period in the

corresponding column ........................................................... 1.

4 2.4 1.5 1

2. Annualization amounts .......................................................... 2.

3. Annualized total income. Multiply line 1 by line 2 ................. 3.

4. Enter total exemption allowance (MI-1040, line 15) .............. 4.

5. Subtract line 4 from line 3 ...................................................... 5.

6. Multiply line 5 by 2008 tax rate 4.35% (0.0435) .................... 6.

7. Enter the sum of your 2008 MI-1040 credit from lines 19,

27, 28, 29, 30 and 31b in each column ................................. 7.

8. Tax after credits. Subtract line 7 from line 6 (if zero or less,

enter “0”) ................................................................................ 8.

9. Multiply line 8 by 22.5% (1st period), 45% (2nd period), (line 8 x 22.5%) (line 8 x 45%) (line 8 x 67.5%) (line 8 x 90%)

67.5% (3rd period) and 90% (4th period).

Enter the results in each column ........................................... 9.

10. Enter combined amounts from line 16 of all previous

columns ................................................................................. 10.

11. Subtract line 10 from line 9 (if zero or less, enter “0”) ........... 11.

12. Required quarterly payment. Divide the amount on MI-2210,

line 8, page 1, by four and enter the result in each column ... 12.

13. Enter the amount from line 15 of the previous column .......... 13.

14. Add lines 12 and 13 ............................................................... 14.

15. Subtract line 11 from line 14 (if zero or less, enter “0”).......... 15.

16. Required installments. Enter the smaller of lines 14 or 11

here and on MI-2210, line 10, page 1.................................... 16.

+ 0000 2008 53 02 27 1

3. Instructions for Form MI-2210

2008 MI-2210, Page 3

Underpayment of Estimated Income Tax

Complete the MI-2210 form and the annualization

General Instructions

worksheet and attach them to your Michigan annual tax

Use this form to determine if you owe penalty and interest return (individual or fiduciary).

for failing to make estimated payments or for underpaying

Completing the Worksheet

the estimated tax due. You can be charged interest (and

You must annualize for the entire year by completing all

possibly penalty) if your payment was insufficient or late in

four columns.

any quarter. This is true even if you are due a refund when

Complete one column at a time. Line 1 must be the year-

you file your tax return. The interest and penalty are figured

to-date total for each period in the appropriate column.

separately for each due date; you could still owe interest

Each column is an accumulating total and should include

and penalty even if you made up an earlier underpayment

the amount from the previous column plus any additional

with an overpayment later.

income earned to date. The last column should equal the

The estimated tax payments must be made timely, in four

amount on your MI-1040, line 14.

equal installments, and the sum of the installments must

Example: You earned $5,000 in the first three months of

equal:

the year. You earned an additional $4,000 during April and

• 90 percent of the tax shown on your 2008 tax return,

May. Enter on worksheet line 1, $5,000 in the first column

or

and $9,000 in the second column.

• 100 percent of the tax shown on your 2007 tax return,

Each entry on worksheet line 13 will be MI-2210, Part 1,

or

line 8, divided by four regardless of how the income is

• 110 percent of the tax shown on your 2007 return if

earned. If you add worksheet line 17 across the columns,

Adjusted Gross Income (AGI) was $150,000 or more

the sum should equal the total shown on MI-2210, line 8.

for joint or single filers or $75,000 or more for married

Taxpayers who annualize must also enter 25 percent of

filing separately.

tax withheld in each column of the MI-2210, line 11, or

Because this is a complicated form, you may choose to

submit documentation to substantiate uneven distribution

have Treasury compute your interest and penalty and send

of withholding.

you a bill instead of filing the form yourself. If you want

Special Rules for Farmers, Fishermen and Seafarers

Treasury to figure your interest, complete your MI-1040

Do not file this form if BOTH of these apply:

form as usual, leaving the interest line blank and do not

attach form MI-2210. Interest computed on this form and • Your gross income from farming, fishing or seafaring

penalty charged for failing to file or underpaying estimates is at least 2/3 of your annual gross income for 2007 or

will be the same regardless of whether you pay with your 2008, AND

return or if Treasury bills you.

• You filed your MI-1040 and paid the entire tax due by

You may avoid penalty and interest and should not file March 1, 2009.

this form IF:

Where to Get Forms

• You had no tax liability for 2007 (if you had to file), If you need to file estimated tax, a 2009 Michigan

or you were not required to file a 2007 return and your estimated income tax formset (MI-1040ES for individuals,

2007 federal tax return was for a full 12 months. MI-1041ES for fiduciaries) is available on the Treasury

• The total tax on your 2008 return minus the amount you Web site at www.michigan.gov/taxes or by calling

paid in withholding and all your credits is $500 or less. toll-free 1-800-827-4000 to have tax forms mailed to you.

• You made timely estimated tax payments. Line-by-Line Instructions

• No penalty is charged if estimates were not required in

Before completing Part 1, add MI-1040 lines 27, 28, 29,

the immediately preceding year, however interest may

30, 31b and 32. Subtract this sum from MI-1040, line 20.

still be due.

If the result is $500 or less, do not complete this form. For

Annualizing

MI-1041, subtract line 24 from line 23. If the result is $500

If you receive income unevenly during the year (i.e., from or less, do not complete this form.

a seasonal business, capital gain, severance pay or bonus)

FISCAL-YEAR FILERS: Change due dates and interest

you may annualize your income.

rates to correspond with your tax year.

4. 2008 MI-2210, Page 4

Example: Your tax due each period is $2,000. You

PART 1: FIGURING THE UNDERPAYMENT

have an underpayment of $1,000 for the first period (due

Line 5: Figure your 2007 tax from your 2007 return. On April 15). On June 10 you send $2,000 to pay the second

the MI-1040 form, subtract the sum of lines 26, 27, 28 and installment. But, $1,000 of this payment goes toward your

29 from line 20 and enter here. This amount must equal at $1,000 underpayment first. Interest is computed on $1,000

least 100 percent of the tax shown on your 2007 tax return, from April 15 to June 10 (56 days). The remaining $1,000

or 110 percent of the tax shown on your 2007 return if AGI is applied to your second installment payment, creating a

was $150,000 or more for joint or single filers or $75,000 second period underpayment of $1,000.

or more for married filing separately. Fiduciaries, enter the

Interest will continue to accrue on this $1,000 until another

amount from MI-1041, line 22.

payment is received.

Line 6: Figure your 2008 tax. On the MI-1040 form,

Interest rates are set by Treasury twice each year for six-

subtract the total of lines 27, 28, 29, 30 and 31b from

month periods starting January 1 and July 1. The rate is

line 20 and enter here. Fiduciaries, enter the amount from

1 percent above the prime rate in Michigan. For example,

MI-1041, line 23.

if the Michigan prime rate is 10.2 percent, your interest

Line 10: If you did not receive your income evenly rate for completing the MI-2210 is 11.2 percent for that

throughout the year, you may annualize your income. See six-month period. For current interest rates, visit our Web

the instructions and worksheet on this form. site at www.michigan.gov/taxes for a copy of Revenue

Administrative Bulletin 2008-5.

Line 11: Enter the estimated tax payments you made plus

any withholding. Note the following:

PART 3: FIGURING THE PENALTY

• One-fourth of your total withholding is considered paid

Penalty is 25 percent of the tax due (minimum $25), for

on each due date unless you can document the dates the

failing to file estimated payments or 10 percent (minimum

tax was withheld.

$10) for failing to pay enough with your estimates or paying

• An overpayment from 2007 that has been credited

late.

forward to 2008 will be applied to the first installment.

Line 24: The underpayment for the penalty charge is

• Do not enter extension payments on this form.

figured the same way as the underpayment for interest.

In column A, enter the estimated tax payments made

Exceptions:

by April 15, 2008, that were for the 2008 tax year. In

• Payments are applied in the quarter they are received.

column B, enter payments made after April 15 and through

June 16, 2008. In column C, enter payments made after • If an overpayment occurs in any quarter, the overpayment

June 16 and through September 15, 2008. In column D, amount is carried forward to the next quarter and applied

enter payments made after September 15, 2008, and through as a timely payment.

January 15, 2009. Extension payments or other payments • Payments are not carried back to offset underpayments

received after January 15 are not considered estimated tax in previous quarters.

payments for tax year 2008.

The amount on line 24 cannot be less than zero (0).

PART 2: FIGURING THE INTEREST Line 25: Enter 25 percent if estimated tax payments

were not made for 2008. Enter 10 percent if estimated tax

The MI-2210 computes interest to April 15, 2009, or the

payments were made for 2008.

date of payment, whichever is earlier. This part of the form

breaks down underpayments to the payment period they Example: In the example in Part 2, the $2,000 payment

are due, then gives the interest rate for that period. Interest received on June 10 is applied to the $2,000 required

is figured for the number of days the installment remained payment in the second quarter. The penalty in the first

unpaid. All payments are applied to any underpayment first, quarter is $100 (10 percent of the $1,000 underpayment in

regardless of when the payment is received. The balance (if the first quarter). The penalty in the second quarter would

any) is applied to the next period. be zero (0).

Note: Complete lines 11 through 23 for column A before

going to column B, etc. You need only complete each

column to the date the payment was made. If the total

underpayment for any payment period was not paid off

with one payment, you may need to do several calculations

in each column.