Download to read offline

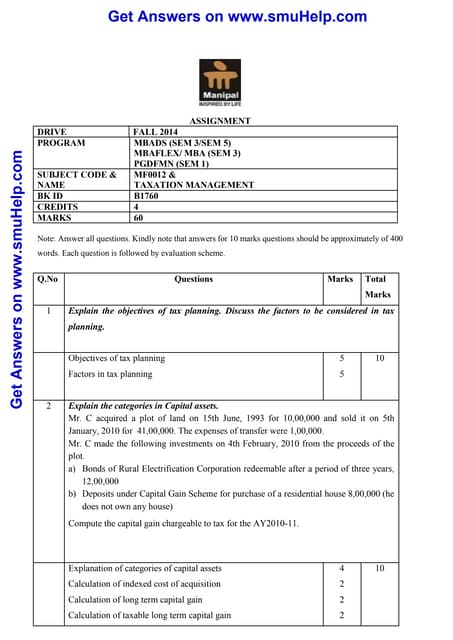

The document provides details of an MBA semester 3 assignment on Taxation Management consisting of 6 questions requiring answers between 300 to 400 words each. The assignment covers topics such as objectives of tax planning, categories of capital assets, capital structure planning, dividend policy, service tax law, exemptions and rebates in service tax, and customs duty calculations. Students are instructed to answer all 6 questions within 6-8 pages and submit their assignment by the given contact details.