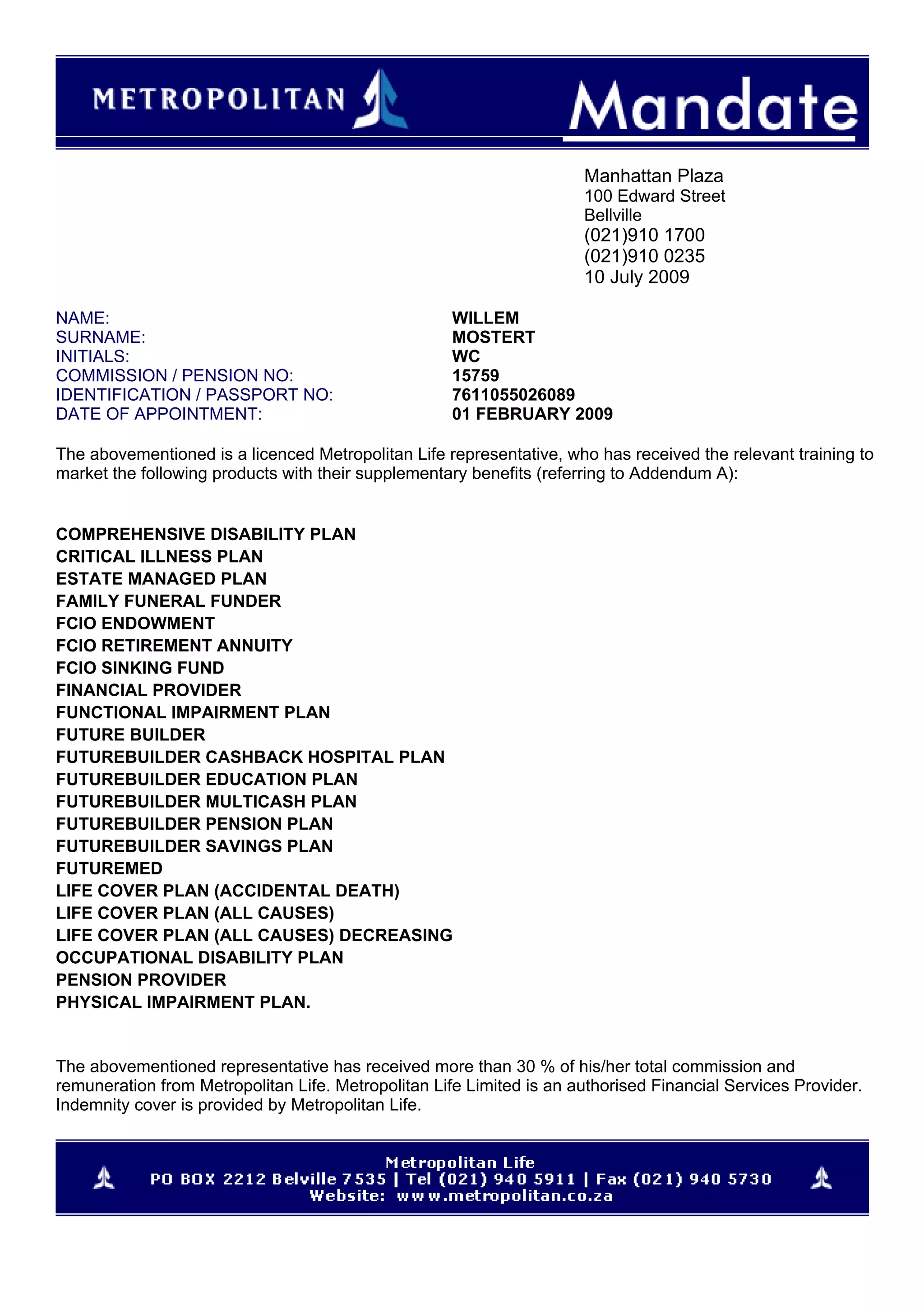

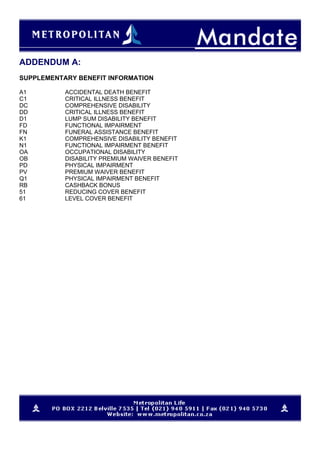

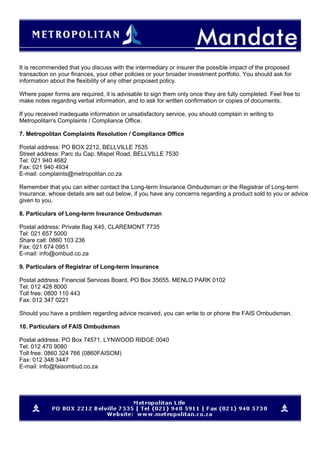

Willem Mostert is a licensed representative of Metropolitan Life who is authorized to market various insurance products, including disability, critical illness, retirement, and life insurance plans. He has received over 30% of his commission from Metropolitan Life. The document includes details on supplementary benefits that can be added to certain plans, as well as a statutory notice outlining policyholders' rights regarding disclosure, replacement policies, cancellation, and complaints procedures.