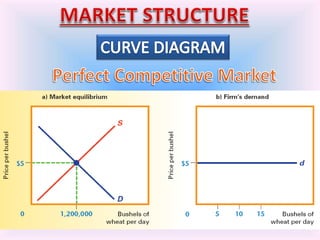

The document outlines the characteristics of a market, emphasizing that it encompasses the interactions of buyers and sellers, rather than being confined to a physical location. It describes different market structures such as perfect competition, monopolistic competition, oligopoly, and monopoly, detailing their attributes like the number of firms and barriers to entry. Key concepts include the determination of price through competition, the need for transparency of information, and the presence of buyers and sellers for market functionality.