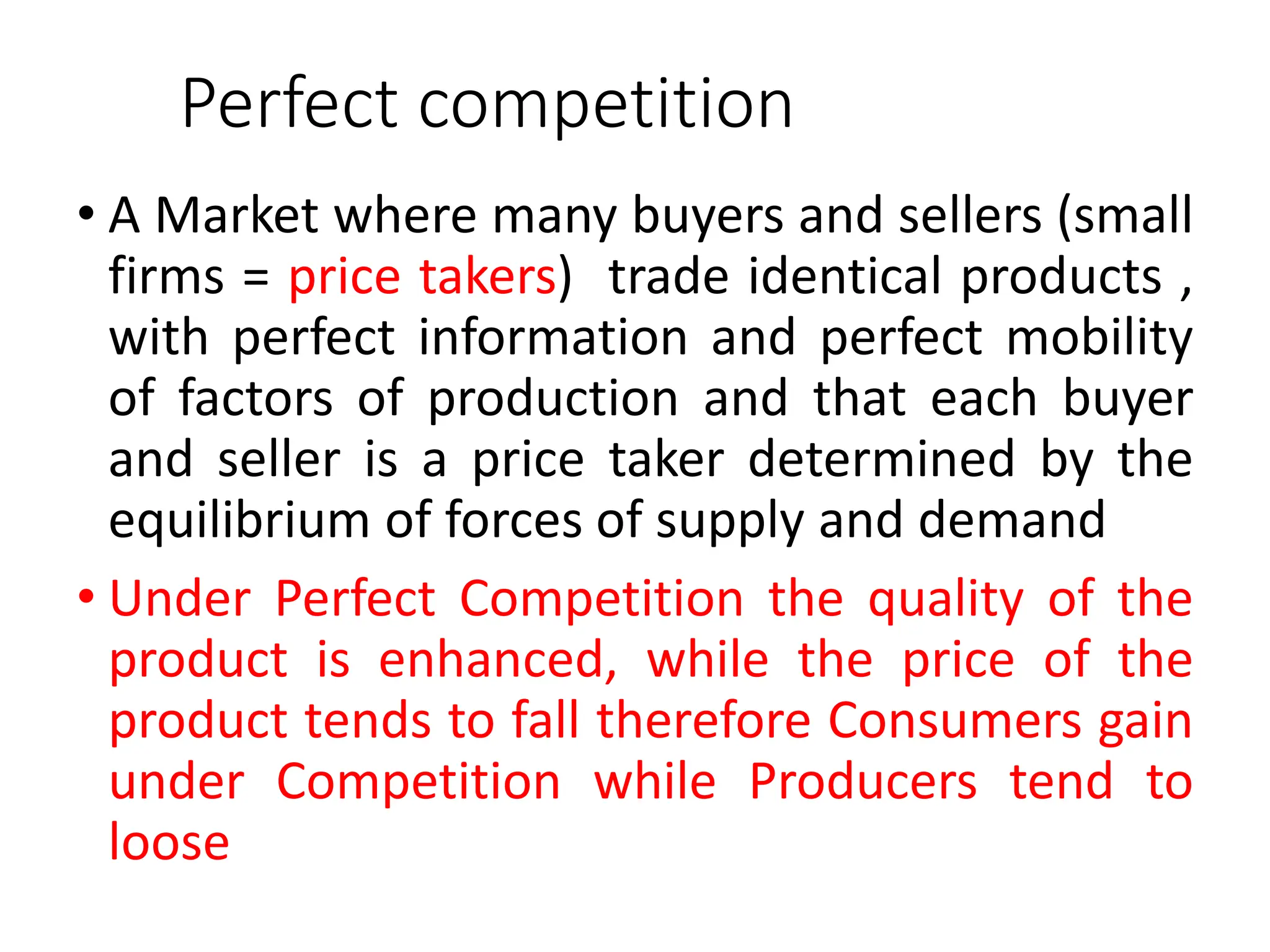

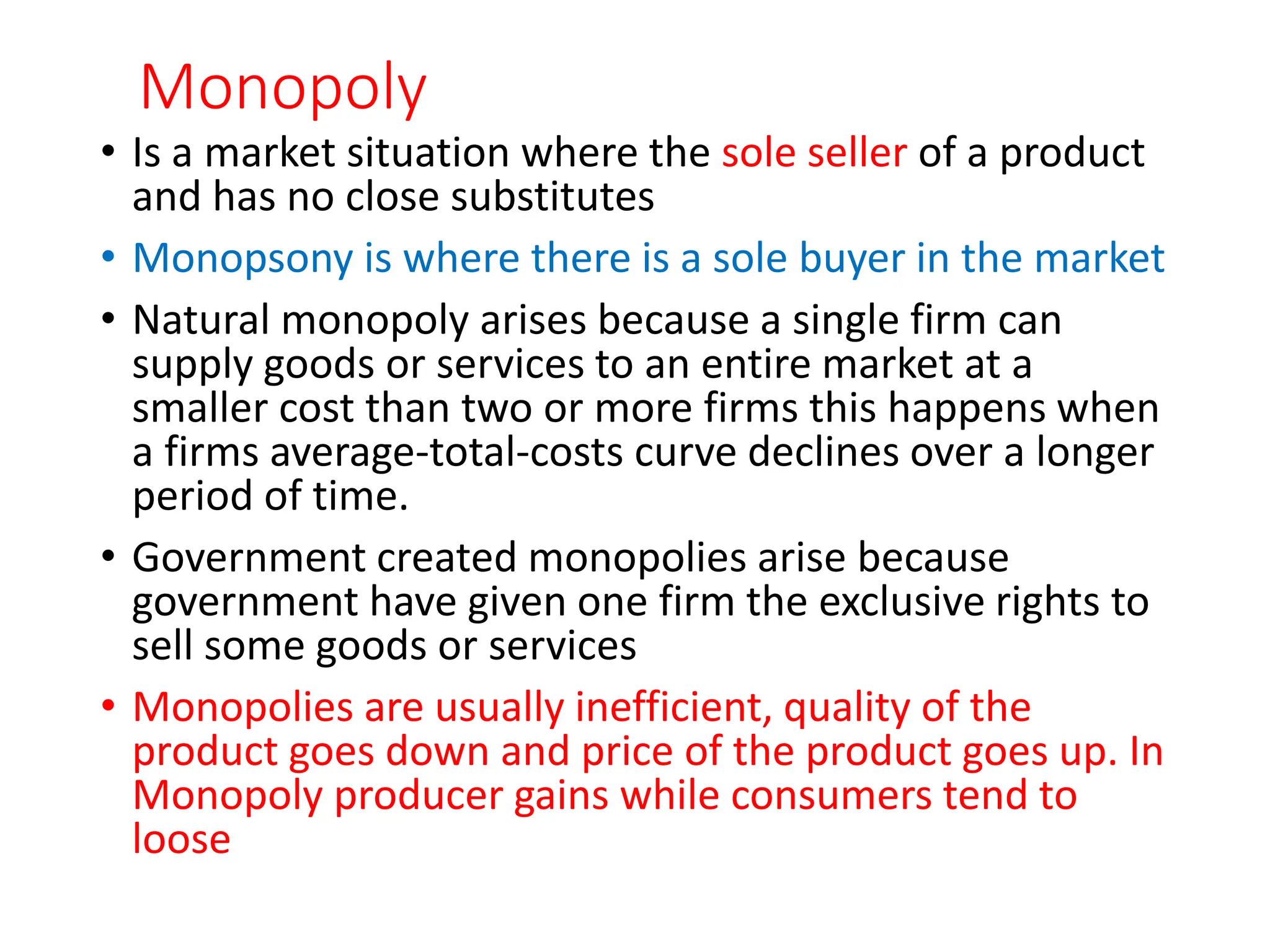

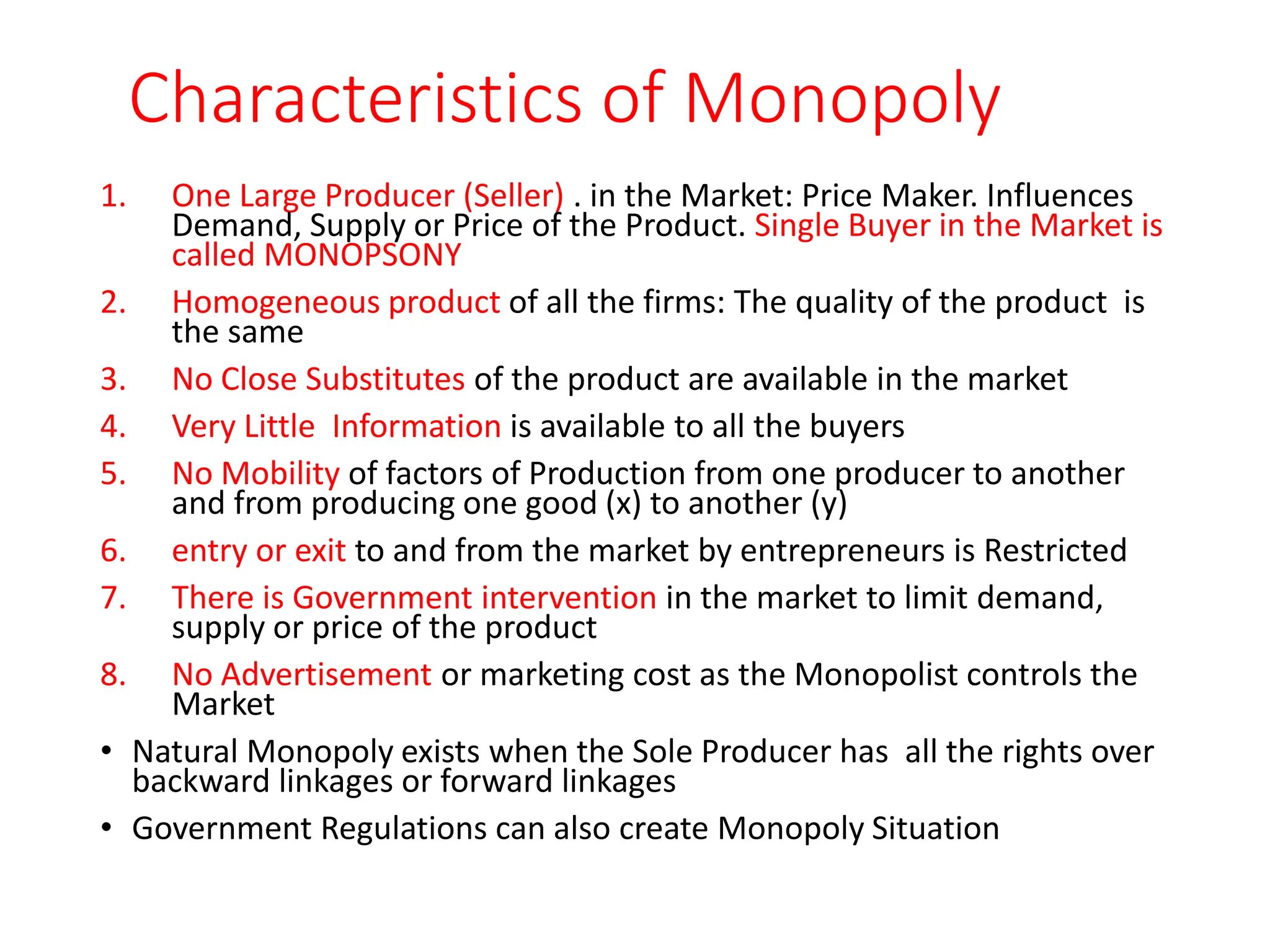

This document discusses different market structures: perfect competition, monopoly, monopolistic competition, and oligopoly. It provides characteristics and examples of each. Perfect competition is defined as having many small firms, homogeneous products, perfect information and mobility. Monopoly is defined as having a single seller and no close substitutes. Monopolistic competition involves differentiated products and some product substitutes. Oligopoly involves a small number of firms producing similar or identical products. The document also discusses concepts like welfare costs of monopolies, price discrimination, and kinked demand curves.

![Lesson 10--mkt-structures[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-10-mkt-structures1-130409195936-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)