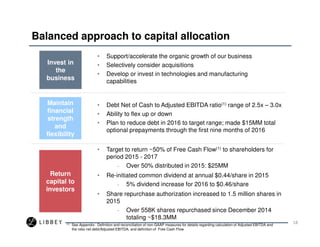

The document summarizes a presentation given by Libbey Inc. to investors. It highlights that Libbey is a global leader in glass tableware, especially in foodservice, with opportunities to grow organically and through acquisitions. Libbey has a strategic focus on innovation, customer focus, and business simplification to improve margins and returns. Financially, Libbey aims to balance investing in the business, maintaining financial strength, and returning capital to shareholders.

![Piper slides 11 11 16 final [read only]](https://cdn.slidesharecdn.com/ss_thumbnails/piperslides111116finalread-only-161114212607-thumbnail.jpg?width=640&height=640&fit=bounds)